When you work remotely from a different state than your employer, you may owe taxes to both your home state and your employer’s state. Most states offer a tax credit to prevent true double taxation—but it doesn’t always fully offset the liability. The “Convenience of Employer” rule (used by New York and a few others) can mean taxes follow your employer’s state regardless of where you physically work. Update your payroll immediately after any move, and file both a resident and non-resident return wherever required.

Remote work tax implications hit hardest when you least expect them—usually around April, when you realize you owe money in a state you haven’t set foot in for months. I’ve spent two decades advising on compensation strategy and total rewards, and I’ll tell you: multi-state tax exposure is one of the most consistently misunderstood financial risks facing remote professionals right now.

You moved to a lower-cost state. You kept your job. You assumed taxes would simply follow. Then your W-2 shows withholding for a state you no longer live in, your home state wants its cut too, and suddenly you’re staring at two tax returns, potential penalties, and a refund that may never come.

This guide is what I wish every remote employee would read before they move—or even before they accept a remote role. No jargon, no hedging. Just the mechanics of how state taxes actually work when your employer’s ZIP code and yours don’t match.

How Remote Work Changes Your State Tax Picture

Before remote work became mainstream, state taxes were simple: you lived and worked in the same state, filed one state return, and moved on. The system wasn’t designed for a reality where your laptop lives in Austin but your employer’s headquarters is in Manhattan.

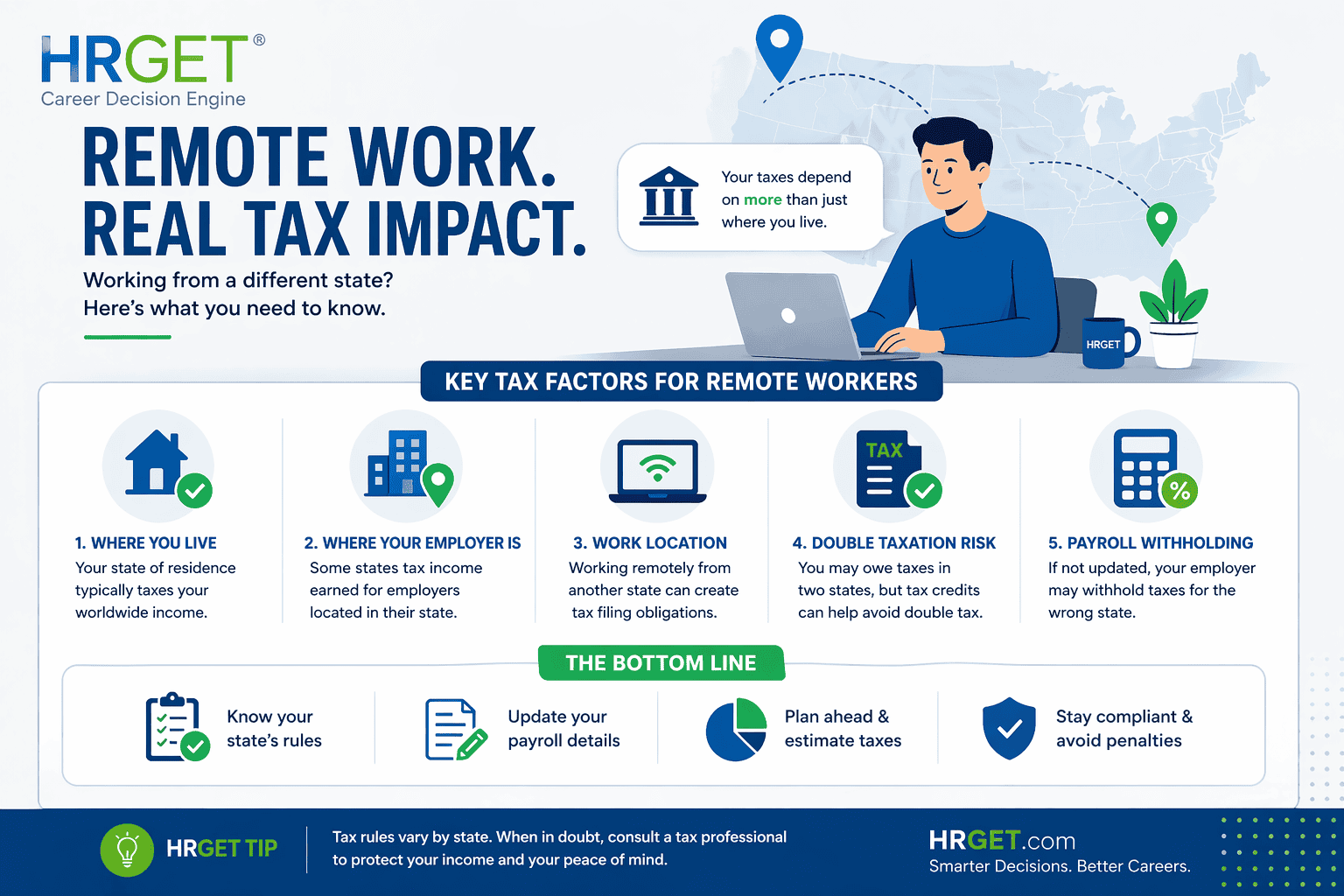

When you work remotely from a state different from your employer’s, you potentially create three separate tax obligations simultaneously:

| Tax Obligation | Triggered By | Who This Affects |

|---|---|---|

| Resident State Tax | Where you physically live | Everyone |

| Non-Resident State Tax | Where your employer is located or where income is sourced | Most cross-state remote workers |

| Payroll Withholding State | Where your employer’s payroll system is set up | Depends on employer’s setup—often wrong |

These three don’t always align. When they don’t, you end up over-withheld, under-withheld, or filing in the wrong states entirely. The IRS doesn’t care—your state revenue department will eventually find the discrepancy, and the notice you get won’t be friendly.

Insider View

Most HR and payroll departments default to the employer’s office location for withholding. They don’t proactively update your tax profile when you move. That’s your job. I’ve seen senior professionals earning $200K+ go two full years being withheld for a state they left—and then face a messy correction process. The system isn’t built to protect you here.

Residency vs. Work Location: What Actually Controls Your Tax Bill

Here’s the distinction most articles gloss over, and it’s the foundation of everything else.

Your Resident State: Primary and Unlimited

Your state of domicile—where you maintain your permanent home, driver’s license, voter registration, and primary financial ties—has the right to tax your worldwide income. It doesn’t matter where the work happens or where your employer is incorporated. If you’re a New York resident, New York taxes your salary, your RSUs, your freelance income, and your side gig, regardless of where the work physically occurred.

Establishing residency somewhere new isn’t just about signing a lease. States like California and New York are aggressive about residency audits. To truly sever ties, you need to update your driver’s license, voter registration, banking address, and ideally, spend fewer than 183 days in the old state in a calendar year. Miss any of these, and the old state may continue to claim you.

Your Work State: Secondary But Real

Separately, many states assert the right to tax income earned within their borders—or, in some cases, income tied to work that benefits an employer located there. This is where things get genuinely complicated, because states differ significantly on what “earned within our borders” means for a remote worker.

Warning

California is particularly aggressive. Even if you leave CA and work remotely, if your employer is a California entity and your work is considered “California-sourced,” the Franchise Tax Board may assert taxing authority. Moving to Nevada or Texas isn’t automatically a CA tax escape. Your employment agreement and work classification matter enormously.

The bottom line: residency creates a primary tax obligation, and your employer’s state may create a secondary one. The two can overlap. That overlap is exactly what tax credits are designed to address—but only partially, and only if you file correctly.

Do You Have to File Taxes in Two States?

The short answer is: probably yes, but “filing in two states” doesn’t automatically mean paying full taxes in both.

| Your Situation | Filing Requirement | Risk Level |

|---|---|---|

| Live and work in same state | One state return | Low |

| Live in State A, employer in State B, fully remote | Resident return (A) + possibly non-resident return (B) | Medium–High |

| Moved mid-year, worked in two states | Part-year resident returns for both states | High |

| New York employer, work from any state remotely | NY non-resident return likely required | Very High |

| States with reciprocal agreements (e.g., PA ↔ NJ) | Only resident state return needed | Low |

When you do file in two states, the typical structure is: file your non-resident return first (for the employer’s state), then file your resident return and claim a credit for taxes paid to the non-resident state. The credit reduces—but often doesn’t entirely eliminate—your resident state liability.

There are 17 states with reciprocal agreements as of 2026, meaning residents of one state who work in the other only file in their home state. Pennsylvania–New Jersey, Maryland–Virginia–DC, and Indiana–several surrounding states are common examples. If your employer is in one of these states and you live in the other, you may only need one return. But you must file the exemption certificate with your employer—it’s not automatic.

The “Convenience of Employer” Rule — The Trap Nobody Warns You About

This is the one rule that blindsides more remote workers than anything else. And it’s genuinely unfair—but it’s legal.

A handful of states—most notably New York, and also Connecticut, Delaware, Nebraska, and Pennsylvania—apply what’s called the “Convenience of Employer” doctrine. The rule goes like this:

If you’re working remotely for your own convenience (not because your employer requires you to be outside the state), those states can tax your income as if you were physically working in their state.

Real Scenario

The situation: Marcus is a senior product manager earning $155,000. His employer is headquartered in New York City. In 2024 he relocated to Florida—which has no state income tax—and has been working fully remote ever since. His HR team updated his address but not his tax withholding. Marcus assumes he now pays zero state income tax.

What actually happens: New York’s Convenience of Employer rule means that because Marcus chose to work remotely (his employer didn’t mandate it), New York still considers his income NY-sourced. He owes NY state income tax—potentially at the top marginal rate of 10.9%—on a large portion of his salary. He’s been under-withheld for two years and owes back taxes plus interest.

The fix? Marcus needed a written employer mandate requiring remote work, and even then, NY would scrutinize it closely. Simply moving isn’t enough with a NY employer.

The Convenience rule has survived several legal challenges. The US Supreme Court declined to review a case challenging it as recently as 2021 (New Hampshire v. Massachusetts). In 2026, it remains fully in effect in New York. If your employer is in one of the five states listed above and you work remotely, consult a multi-state tax professional before assuming you’ve escaped their taxing authority.

Real Scenario: California Employer, Texas Remote Worker

California doesn’t use the Convenience of Employer rule—but it has its own version of tax aggression that catches people off guard.

The Setup

Sarah earns $120,000 working for a Bay Area tech company. She moves to Austin, Texas (no state income tax), and her employer approves a permanent remote arrangement. She expects her state income tax bill to drop from approximately $9,000 to zero.

What Actually Determines Her Outcome

| Factor | Favorable for Sarah | Unfavorable for Sarah |

|---|---|---|

| Payroll updated? | Yes → TX withholding only | No → CA still withholds |

| True CA domicile severed? | Updated DL, voter reg, 183-day rule | Maintains CA ties → CA residency |

| Is income “CA-sourced”? | Fully remote, no CA clients/travel | Visits CA for work, CA-based projects |

| Employer classification? | Reclassified as TX remote employee | Employer still treats her as CA-based |

California’s Franchise Tax Board tracks departing high earners. If you earned significant income in CA, moved, and suddenly stop filing CA returns, expect a letter. Sarah needs to document every element of her departure—not just change her mailing address. Done correctly, yes, she can legitimately eliminate her CA tax liability. Done carelessly, she could face a CA audit years later.

“Moving to Texas doesn’t automatically make you a non-California taxpayer. California decides that—and they’ll ask questions.”

How to Avoid Double Taxation (Tax Credits Explained)

The mechanism designed to prevent you from paying full tax in two states is the Resident Credit for Taxes Paid to Another State. Most states offer this—but the details matter.

How It Works (The Simple Version)

- You earn $100,000 and pay $5,000 in non-resident tax to State B (your employer’s state)

- Your resident State A calculates that you owe $7,000 in resident tax on that same income

- State A gives you a credit of up to $5,000 for what you paid to State B

- You pay State A the remaining $2,000

- Total effective state tax: $7,000—same as if you only filed in State A

Where the System Breaks Down

This works cleanly when your resident state has a higher tax rate than your employer’s state. But it breaks down in several common scenarios:

- High-tax employer state, lower-tax home state: State A’s credit may only cover up to the resident state’s rate—so you could still owe tax to State B above what State A credits you for

- Convenience of Employer states: Credits may not apply to income taxed under the convenience rule, since the income is deemed “sourced” in the employer’s state regardless of where you worked

- Paperwork errors: Missing a non-resident filing for State B means you can’t claim the credit on your State A return—and may owe penalties to State B as well

Pro Tip

Always file your non-resident return first. The credit calculation on your resident return requires the non-resident liability number. Tax software often prompts this order, but if you’re working with an accountant, confirm they understand multi-state filing—it’s a specialty, not something every generalist CPA handles well.

Employer Payroll Mistakes You Must Catch Yourself

Here’s an uncomfortable truth I share with every senior professional I advise: your employer’s payroll system is not looking out for your tax accuracy. It’s looking out for compliance at the entity level. Your individual situation is your problem until it becomes a compliance issue for them.

The most common payroll errors I see with remote workers:

1

Withholding for the old office state after you moved

The system defaults to where you were classified. If you moved in March and never formally updated HR, your December paycheck is still showing California or New York withholding. You’ll get a refund from that state—eventually—but you’ll also owe your new home state back taxes and potentially interest.

2

Withholding for the employer’s state even when you should be classified elsewhere

Some payroll teams assume “remote” means they still withhold for the company’s primary location. This is incorrect in most states but common in practice. If your W-2 shows withholding for a state you never lived in and can’t claim a credit for, it’s a mess.

3

Failing to update the work location field in the HRIS

Payroll withholding is often tied to the “work location” field in systems like Workday or ADP—not your personal address. Updating your home address is not the same as updating your work location. Both need to change.

4

Not registering with the new state for employer tax purposes

When you move states, your employer technically needs to register as an employer in your new state and potentially pay state unemployment insurance there. If they haven’t done this, they may resist updating your payroll—and that delay costs you. This is a legitimate friction point, and you may need to escalate through HR.

Check your paystub every single month when you’re in a multi-state situation. Specifically confirm: which state is listed for withholding, the dollar amount withheld, and whether it aligns with your current physical work location.

Smart Tax Strategies for Remote Workers in 2026

Compliance is the floor. Smart remote workers treat their work location as a financial optimization variable—and in 2026, with more employer flexibility than ever, that leverage is real.

1. Choose Your Home State Strategically

If your employer allows permanent remote work from anywhere, your state of residence choice is a compensation decision. The nine states with no income tax—Texas, Florida, Nevada, Washington, Wyoming, South Dakota, Alaska, Tennessee, and New Hampshire—offer meaningful tax savings at higher income levels. At $150,000 income, moving from California to Texas saves roughly $12,000–$14,000 per year in state income taxes. That’s real money that no salary increase conversation needs to happen for.

The caveat: if your employer is in a Convenience of Employer state like New York, this strategy has limits. You need to verify that your income genuinely escapes that state’s reach before banking on the savings.

2. Update Payroll the Day You Move—Not the Day You File

Employers typically need 1–2 pay cycles to process a state change. If you move on March 1 and don’t notify HR until March 15, you’ve already generated incorrect withholding for two payroll periods. Start the paperwork immediately. Submit a written address change, a new state W-4 or equivalent, and confirm with payroll that the work location field is updated—not just your home address.

3. Build a Documentation Trail for Remote Work Status

If a state revenue department audits you and argues you were “really” working in their state, your defense rests on documentation. Keep: your remote work agreement or email approval, any home office lease or mortgage showing your physical work location, VPN logs or timestamped communications establishing where you worked from, and records showing you didn’t travel to the employer’s state for work during the period in question.

4. Pay Quarterly Estimated Taxes If Your Withholding Is Wrong

If you discover mid-year that your employer’s withholding is incorrect and the fix will take several pay cycles, don’t wait. Pay estimated taxes directly to your home state on a quarterly schedule (April, June, September, January) to avoid underpayment penalties. The threshold in most states is owing more than $500–$1,000 at filing—easily reached if withholding is off by a few months.

5. Understand and Use Reciprocal Agreements

If you live in a state with a reciprocal agreement with your employer’s state, submit the exemption certificate to your HR team. This exempts you from non-resident withholding in the employer’s state. Without it, payroll will default to withholding for the employer’s state regardless.

Pro Tip

Reciprocal agreement certificates go by different names in different states—Virginia calls it Form VA-4, Maryland uses MW507, Illinois uses IL-W-5-NR. If you think you qualify, search “[home state] + [employer state] + reciprocal agreement certificate” and submit the right form directly to payroll. It takes five minutes and can eliminate an entire state filing obligation.

5 Common Mistakes That Quietly Cost Remote Workers Thousands

✕

Assuming the move automatically changed your taxes

It didn’t. Your employer’s payroll system still has your old state. Your W-2 will reflect it. You’ll owe your new home state taxes that weren’t withheld. Without a corrective payment, that becomes a penalty-generating underpayment.

✕

Skipping the non-resident return because “I don’t owe anything there”

If you have a tax obligation in a state—even if it’s fully offset by credits—you typically still need to file a return. Failure-to-file penalties don’t care that you don’t owe money. California and New York actively pursue non-filers.

✕

Not claiming available tax credits

If you paid taxes to State B and failed to claim the credit on your State A return, you overpaid. This happens when people use software and don’t connect the returns, or when they file the resident return first (before the non-resident liability is established).

✕

Assuming “no employer presence” means no tax obligation

Nexus rules are complex. Some states argue that a remote employee working from their state creates nexus for the employer—and separately, that the employee owes income tax there. This varies by state and income level, but the aggressive enforcement trend in 2026 is real.

✕

Waiting until April to discover a multi-state problem

By then you’ve locked in a full year of incorrect withholding, potentially owe penalties, and are correcting the problem retroactively instead of prospectively. A 30-minute mid-year review of your paystub and tax situation prevents most of this.

Pro Tips: What High Earners Do Differently

I’ll be direct here—because this is the section most articles skip. High-earning remote workers (typically $150K+) treat state taxes as a recurring financial optimization, not a once-a-year filing exercise. They do four things consistently:

They involve a multi-state CPA, not a generalist. Not every accountant understands the Convenience of Employer rule, California’s residency audit triggers, or the mechanics of filing part-year returns across three states. For incomes above $120,000 with cross-state complexity, the cost of a specialist ($500–$1,500 per year) is almost always recouped in prevented penalties or identified credits.

They model their tax outcome before accepting a remote work arrangement. If you’re negotiating to go fully remote from a different state, understand whether your employer’s state will still tax you before you agree to it. That conversation changes your actual net compensation calculus significantly.

They treat location as a total compensation lever. Moving from California ($150K income, ~$12K state tax) to Washington ($0 state income tax) is effectively a $12,000 raise. Most professionals who’ve done this negotiation would say getting a $12K raise from a manager is harder than making a well-structured move. Same money—different path.

They don’t travel to the employer’s state casually. If you’re a New York employer, every day you work in New York (even for a quarterly meeting) is a day potentially taxable in New York. Track your travel days. In some states, even 14 days of in-state work triggers a partial non-resident obligation.

Insider View

State revenue departments have gotten significantly more sophisticated about tracking remote workers. Data sharing between the IRS and state agencies, employer payroll reporting, and even cell phone location data (in audit situations) means that gaming your residency status is increasingly difficult and not worth the risk. The strategy isn’t to hide—it’s to structure your situation correctly from the start.

Bottom Line

Remote work tax implications are real, often significant, and not self-correcting. Here’s what you need to hold onto from this article:

- Your resident state taxes all your income—regardless of where your employer is

- Your employer’s state may still claim a portion—especially under the Convenience rule (NY, CT, DE, NE, PA)

- Payroll errors are the norm, not the exception—verify your withholding monthly

- Tax credits prevent true double taxation in most cases, but only if you file correctly and in the right order

- Your work location is a financial decision—treat it that way when evaluating remote opportunities

The remote work tax implications you face in 2026 are more complex than what existed three years ago. But with the right structure, they’re entirely manageable—and even optimizable.

Frequently Asked Questions

Do I have to file a tax return in two states if I work remotely for an out-of-state employer?

In most cases, yes. You’ll typically file a resident return in your home state and a non-resident return in your employer’s state—unless a reciprocal agreement applies. Filing in two states doesn’t necessarily mean paying full taxes in both; your home state usually gives you a credit for taxes paid to the other state. But skipping the non-resident return entirely can trigger failure-to-file penalties even if you don’t owe additional tax.

Can my employer’s state tax me if I never physically worked there?

Yes—if your employer is in a state that uses the “Convenience of Employer” rule (New York, Connecticut, Delaware, Nebraska, and Pennsylvania). These states tax income as if you worked in their state, even if you worked entirely from another state, unless your employer mandated that you work remotely. Simply choosing to work remotely for your own reasons doesn’t exempt you from their taxing authority under this doctrine.

What is the “Convenience of Employer” rule and which states use it?

The Convenience of Employer rule allows certain states to tax income as if it were earned within their borders, even when the employee works entirely from another state—provided the remote arrangement was the employee’s choice rather than a documented employer requirement. As of 2026, the states that apply this rule are New York, Connecticut, Delaware, Nebraska, and Pennsylvania. New York is the most aggressive enforcer. If your employer is based in any of these states, consult a multi-state tax specialist.

How do tax credits work for remote workers who owe taxes in two states?

Most states offer a Resident Credit for Taxes Paid to Another State. After filing your non-resident return (employer’s state), you bring that tax liability number to your resident return and claim a credit. Your home state’s tax is reduced by what you paid to the other state—up to the resident state’s own rate on that income. File the non-resident return first; otherwise you can’t calculate the credit accurately on your home state return.

What should I do immediately after moving to a new state for remote work?

Notify HR and payroll in writing. Update both your home address and your work location field in your employer’s HRIS system (these are separate fields in most platforms like Workday or ADP). Submit a new state withholding form. If a reciprocal agreement exists between your old and new state, submit the exemption certificate to payroll. Then verify the change appears on your next paystub—don’t assume it happened automatically. Do this within the first week, not at year-end.

Does moving to a no-income-tax state like Texas or Florida eliminate my state tax obligation?

Not automatically—and sometimes not at all. If your employer is in a Convenience of Employer state (especially New York), moving to a no-tax state won’t necessarily eliminate that state’s tax claim on your income. Even for non-COE states like California, you need to fully sever residency ties—updating your license, voter registration, and spending fewer than 183 days in CA—before the Franchise Tax Board accepts your departure. The move is a necessary step, not a sufficient one.

Do states have reciprocal tax agreements for remote workers?

Yes. As of 2026, approximately 17 states have reciprocal agreements with neighboring states, meaning residents of one state who work in the other only need to file in their home state. Common examples include Pennsylvania–New Jersey, Maryland–Virginia–DC, and Indiana with several surrounding states. To benefit, you must submit an exemption certificate to your employer—it’s not applied automatically. Reciprocal agreements don’t apply to the Convenience of Employer states, so New York employees can’t use this route.

At what income level should I hire a multi-state tax professional?

If you earn above $100,000 and work remotely for an employer in a different state—particularly in New York, California, Connecticut, or Delaware—the complexity almost certainly justifies a multi-state CPA or tax attorney. At that income level, a single filing error, missed credit, or incorrect residency classification can cost $5,000–$15,000 in back taxes, penalties, and interest. The specialist fee ($500–$1,500) is typically recovered many times over. For lower incomes with straightforward cross-state situations, high-quality tax software (TurboTax, H&R Block) handles most multi-state scenarios adequately.

Next: How Remote Work Affects Your Salary Negotiation

Your tax situation changes the real value of any offer. Learn how to negotiate remote compensation accounting for location-based adjustments.

The Bottom Line: Remote Work Taxes Reward the Prepared

The remote work tax implications of working from a different state aren’t a minor administrative nuisance—they’re a meaningful financial variable that can shift your effective compensation by tens of thousands of dollars annually. I’ve seen professionals make well-reasoned career moves that looked worse on paper once the multi-state tax picture became clear. And I’ve seen others capture real financial upside by treating their work location as strategically as they treat their salary.

You can’t outsource your awareness here. Your employer’s payroll team isn’t going to proactively protect your tax outcome. Your CPA will only know what you tell them. The remote workers who come out ahead are the ones who understand the basic mechanics—Convenience rules, residency triggers, credit stacking—and act on that understanding continuously, not once a year in April.

Treat your work location like the financial decision it is. Update your payroll the day you move. Document everything. And if you’re earning above $100K in a multi-state situation, get a specialist. The upside of getting this right far outweighs the cost of figuring it out the hard way.

Eleanor Whitmore | Former Partner, Mercer | Advisor, World Economic Forum | 20+ Years in Global Compensation

Author bio: Eleanor Whitmore has spent over two decades shaping how the world’s leading organisations pay, retain, and reward talent. As a former Partner at Mercer and an advisor to World Economic Forum working groups on the Future of Work, she has designed compensation frameworks for Fortune 500 companies across the US, UK, Europe, and emerging markets. Based between London and New York, Eleanor writes for HRGet.com to translate boardroom-level pay strategy into actionable guidance for working professionals navigating real compensation decisions.

Remote work tax stuff can be so confusing. Have you seen any common mistakes people make when dealing with different states?