Quick Answer

A $100,000 salary in the US typically results in:

$78,000–$81,000 take-home in no-tax states (Texas, Florida, Washington) $72,000–$76,500 take-home in high-tax states (California, New York, New Jersey)

Your exact net pay depends on your federal tax bracket, state taxes, filing status, and deductions like 401(k) or health insurance.

The Mistake That Costs Professionals $10K+ Every Year

You got a job offer for $120,000. Congrats — on paper.

But here’s the part nobody celebrates: your actual take-home pay after federal taxes, state taxes, Social Security, and Medicare could land somewhere between $78,000 and $92,000. That’s a $28K–$42K gap between what you “earn” and what hits your bank account.

I’ve spent over 15 years in HR watching smart professionals make the same mistake. They negotiate hard for a higher gross salary, then never once run the numbers on what they’ll actually keep. A take-home pay calculator isn’t just a nice tool — it’s the single most important step before you accept any offer, relocate to a new state, or benchmark your current compensation.

This guide breaks down exactly how your gross salary converts to net pay, state by state, with the 2026 tax brackets and FICA rates baked in. No fluff. Just the math that matters.

Take-Home Pay Calculator (Quick Estimate)

Before you dig into the full breakdown, here’s the quick-estimate formula every professional should know:

Net Pay = Gross Salary – Federal Tax – State Tax – FICA (7.65%) – Pre-tax Deductions

Quick Estimation Rule:

High-tax states (CA, NY, NJ) → you keep roughly 60–70% of gross Mid-tax states (CO, IL, NC) → you keep roughly 68–75% of gross No-tax states (TX, FL, WA) → you keep roughly 72–78% of gross

Quick Examples at a Glance:

| Gross Salary | Texas (No Tax) | California | New York City |

|---|---|---|---|

| $75,000 | ~$59,000 | ~$56,500 | ~$53,500 |

| $100,000 | ~$81,000 | ~$76,400 | ~$72,500 |

| $150,000 | ~$118,500 | ~$110,000 | ~$103,500 |

That gap at $150K? Nearly $15,000 per year between Texas and NYC. Same title, same work, wildly different bank accounts.

But these are estimates. The sections below show you exactly why, and how to use these numbers to make smarter career decisions.

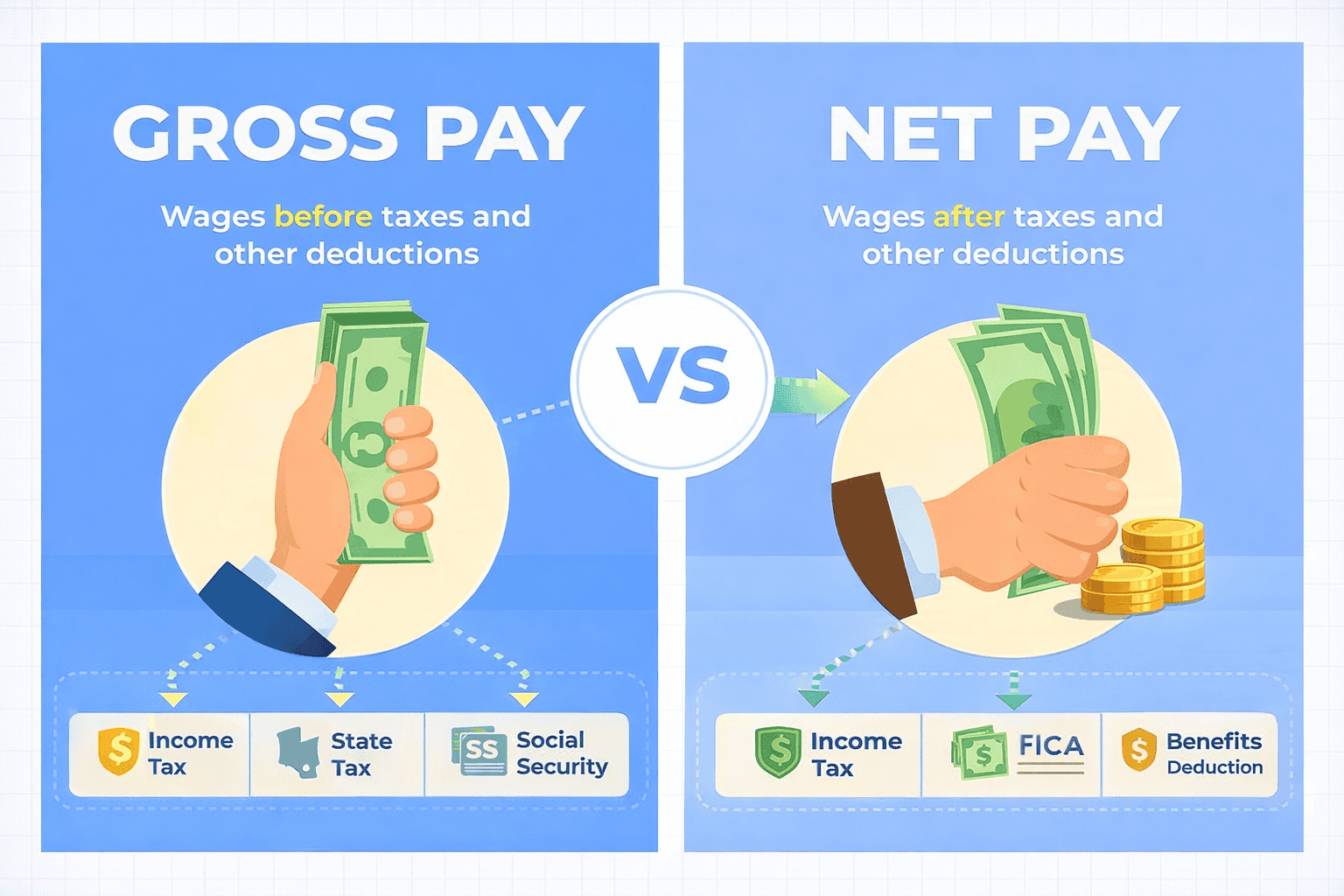

What Take-Home Pay Actually Means (And Why Gross Salary Lies to You)

Take-home pay — also called net pay — is the amount that actually lands in your checking account after every deduction has had its turn. Your gross salary is the number on your offer letter. Your take-home pay is the number that pays your rent.

The gap between those two numbers is larger than most people expect, and it’s not just federal income tax eating into it. Here’s what gets pulled out before you see a dime:

Federal income tax — calculated across seven progressive brackets (more on that below). State income tax — ranges from 0% in states like Texas and Florida to over 13% in California for top earners. Social Security (OASDI) — 6.2% of your wages, up to the 2026 wage base of $184,500. Medicare — 1.45% on all earnings, plus an extra 0.9% if you earn above $200,000. Pre-tax deductions — 401(k) contributions, health insurance premiums, HSA contributions.

Here’s the reality check most articles skip: on a $100,000 salary, you’re losing somewhere between $19,000 and $27,500 depending on your state, filing status, and deductions. That’s not a rounding error. That’s a used car. Every year.

And that’s exactly why comparing job offers by gross salary alone is like comparing apartments by square footage without checking the neighborhood. The number looks right, but it tells you almost nothing about what you’re actually getting.

How to Calculate Net Salary: Step by Step

Forget the complicated tax software for a moment. Here’s how a take-home pay calculator works at its core:

Step 1: Start with your gross annual salary Let’s say $100,000.

Step 2: Subtract the standard deduction For 2026, that’s $16,100 for single filers or $32,200 for married filing jointly. This reduces your taxable income before federal brackets even kick in.

Step 3: Apply federal income tax brackets Your taxable income ($83,900 for a single filer at $100K gross) gets sliced into brackets. You don’t pay 22% on all of it — you pay 10% on the first $12,400, 12% on the next chunk, and 22% on what’s left. The effective federal rate on $100K is roughly 13–15%, not the 22% marginal rate people fear.

Step 4: Subtract FICA taxes Social Security: 6.2% × $100,000 = $6,200. Medicare: 1.45% × $100,000 = $1,450. That’s $7,650 gone — no deductions, no exemptions, dollar one.

Step 5: Subtract state income tax This is where geography becomes destiny. More on that in the next section.

Step 6: Subtract pre-tax benefits 401(k) contributions, health insurance premiums, and FSA/HSA contributions come out before some taxes, which actually reduces your taxable income. If you’re contributing 6% to a 401(k), that’s $6,000 less in taxable income — saving you roughly $1,300–$2,000 in taxes depending on your bracket.

Quick mental shortcut: In a high-tax state, expect to keep roughly 60–70 cents of every dollar. In a no-tax state, you’re closer to 72–78 cents. That difference compounds fast over a career.

2026 Federal Tax Brackets: What You’ll Actually Owe

The 2026 federal income tax brackets, locked in after the One Big Beautiful Bill Act made the TCJA rates permanent, use seven progressive rates:

| Tax Rate | Single Filer Income Range |

|---|---|

| 10% | Up to $12,400 |

| 12% | $12,401 – $50,400 |

| 22% | $50,401 – $105,700 |

| 24% | $105,701 – $199,350 |

| 32% | $199,351 – $253,200 |

| 35% | $253,201 – $640,600 |

| 37% | Over $640,600 |

Standard Deduction (2026): $16,100 (single) | $32,200 (married filing jointly)

Here’s what trips people up: they see “22% bracket” and think they’re losing 22% of their paycheck. Nope. A single filer earning $100,000 has a taxable income of about $83,900 after the standard deduction. Their effective federal tax rate works out to roughly 13.5% — because the lower brackets absorb most of the income first.

I’ve sat across the table from candidates who turned down a raise because they thought it would “put them in a higher bracket” and cost them money. That’s not how progressive taxation works. Every additional dollar only gets taxed at the marginal rate — the rest of your income stays exactly where it was.

Let me put it bluntly: if someone offers you a $10,000 raise that pushes you from the 22% bracket into the 24% bracket, you’re only paying 24% on the dollars above the threshold. You still come out ahead. Always.

State Taxes: The Real Difference Maker

Federal taxes are the same whether you live in Manhattan or Montana. State income taxes? That’s where the real divergence happens — and where most people underestimate the impact on their take-home pay.

States with NO Income Tax (2026)

Alaska, Florida, Nevada, New Hampshire (dividends and interest only), South Dakota, Tennessee, Texas, Washington, Wyoming

Living in one of these states is the equivalent of giving yourself a 5–10% raise compared to a high-tax state. On a $100,000 salary, that’s $5,000 to $10,000 more in your pocket — every single year.

High-Tax States You Need to Plan For

California: Top marginal rate of 13.3% (kicks in above $1M, but rates start at 1% and climb fast — a $100K earner pays around 4–6% effective state tax) New York: Top rate of 10.9%, plus NYC residents pay an additional city tax of up to 3.876% New Jersey: Top rate of 10.75% Oregon: Top rate of 9.9% with no sales tax (so you save elsewhere) Minnesota: Top rate of 9.85%

The Middle Ground

States like Illinois (flat 4.95%), Colorado (flat 4.4%), and North Carolina (flat 4.5% in 2026) fall somewhere in between. Flat-tax states are actually easier to calculate — your effective rate equals the stated rate.

Here’s the part that rarely makes it into salary guides: state taxes interact with your overall financial picture in unexpected ways. Oregon charges high income tax but zero sales tax. Washington does the reverse — no income tax, but a 6.5% state sales tax plus local additions. When you’re running a take-home pay calculator, gross-to-net is only half the equation. Cost of living and consumption taxes fill in the other half.

$100K Salary: Take-Home Pay Across 6 States

Let’s get specific. Here’s what a single filer earning $100,000 (no 401(k) contribution, standard deduction) actually takes home in six different states in 2026:

| State | Federal Tax (est.) | State Tax (est.) | FICA | Annual Take-Home | Monthly Take-Home |

|---|---|---|---|---|---|

| Texas | ~$11,350 | $0 | $7,650 | ~$81,000 | ~$6,750 |

| Florida | ~$11,350 | $0 | $7,650 | ~$81,000 | ~$6,750 |

| Colorado | ~$11,350 | ~$4,400 | $7,650 | ~$76,600 | ~$6,383 |

| Illinois | ~$11,350 | ~$4,950 | $7,650 | ~$76,050 | ~$6,338 |

| California | ~$11,350 | ~$4,600 | $7,650 | ~$76,400 | ~$6,367 |

| New York (NYC) | ~$11,350 | ~$5,400 + ~$3,100 city | $7,650 | ~$72,500 | ~$6,042 |

Look at that spread. Same salary. Same job title. Same level of experience. But a $100K earner in Texas keeps roughly $8,500 more per year than the same earner in New York City. Over five years, that’s $42,500 — real money that could go into investments, a down payment, or just living with less stress.

And I haven’t even factored in cost of living yet. A one-bedroom in Austin runs about $1,400–$1,800/month. The same apartment in Manhattan? $3,200–$4,500. The net pay difference plus the rent difference makes these two very different financial lives.

$120K in California vs $100K in Texas — Who Wins?

This is the comparison that changes minds. I bring it up because it’s the exact scenario I see professionals face every year — and they almost always get it wrong on first instinct.

| Factor | California ($120K) | Texas ($100K) |

|---|---|---|

| Gross Salary | $120,000 | $100,000 |

| Federal Tax (est.) | ~$14,800 | ~$11,350 |

| State Tax (est.) | ~$5,800 | $0 |

| FICA | ~$9,180 | ~$7,650 |

| Annual Take-Home | ~$90,220 | ~$81,000 |

On net pay alone, California still edges ahead by about $9,200. But wait — here’s where the real comparison lives:

| Cost Factor | San Francisco | Austin |

|---|---|---|

| Rent (1BR, central) | ~$3,200/mo | ~$1,600/mo |

| Annual Rent | ~$38,400 | ~$19,200 |

| After Tax + Rent | ~$51,820 | ~$61,800 |

The $20K-higher California offer leaves you with $10,000 less in disposable income after taxes and housing. That’s not a marginal difference — it’s a completely different financial trajectory.

This doesn’t mean California is always the wrong choice. Career trajectory, industry density, network access — those matter too. But you need to make that decision with open eyes, not by staring at the gross salary and assuming bigger equals better.

Real Scenario: When the Lower Offer Was the Better Deal

I worked with a marketing director — let’s call her Priya — who had two offers on the table in late 2025:

Offer A: $135,000 at a SaaS company in San Francisco Offer B: $112,000 at a fintech startup in Austin, Texas

On paper, Offer A looked like the clear winner — $23,000 more in gross salary. Priya almost didn’t run the numbers. But we did.

| Factor | San Francisco | Austin |

|---|---|---|

| Gross Salary | $135,000 | $112,000 |

| Federal Tax (est.) | ~$17,200 | ~$13,100 |

| State Tax (est.) | ~$7,100 (CA) | $0 (TX) |

| FICA | ~$10,328 | ~$8,568 |

| Annual Take-Home | ~$100,372 | ~$90,332 |

| Rent (1BR, central) | ~$3,400/mo ($40,800/yr) | ~$1,600/mo ($19,200/yr) |

| After Rent | ~$59,572 | ~$71,132 |

Priya’s jaw dropped. The “lower” offer left her with $11,560 more per year in disposable income after taxes and housing. Over three years, that’s almost $35,000 in additional financial breathing room — from the offer that paid $23K less on paper.

She took Austin. Last I heard, she’s maxing out her 401(k) and saving for a house. In San Francisco, she’d have been splitting a two-bedroom to make it work.

That’s what a take-home pay calculator reveals: the decision that looks obvious on the surface often isn’t.

5 Costly Mistakes That Shrink Your Paycheck

Mistake #1: Comparing offers using gross salary only

This is the big one. I’ve seen it kill good decisions hundreds of times. Two offers, $15K apart in gross — but after state taxes and cost of living, the “lower” offer actually pays more. If you’re not running a net pay comparison, you’re negotiating blind.

Mistake #2: Ignoring state income tax when relocating

Moving from Houston to Portland for a $10K raise? Oregon’s income tax rate is among the highest in the country. That raise might net you $2,000–$3,000 after state taxes swallow the rest. Always run the relocation math before you accept.

Mistake #3: Forgetting that FICA is non-negotiable

Social Security and Medicare take 7.65% off the top of every paycheck (up to the $184,500 Social Security wage base in 2026). Unlike income tax, there’s no standard deduction protecting you from FICA. It hits dollar one.

Mistake #4: Not factoring in pre-tax benefits

A 401(k) contribution reduces your take-home pay — yes. But it also reduces your taxable income, which lowers your federal and state tax bill. Contributing 6% to a 401(k) on a $100K salary saves you roughly $1,300–$2,000 in taxes per year, depending on your bracket and state. It’s not “losing money” — it’s redirecting it to yourself.

Mistake #5: Overvaluing a high-cost city salary without checking the math

A $150K offer in New York sounds incredible until you realize your after-tax, after-rent take-home might be identical to someone earning $95K in Charlotte. The prestige of the number on your offer letter doesn’t pay bills. The net number does.

Smart Strategy: How to Maximize Take-Home Pay

Here’s a tactical playbook you can use right now — whether you’re evaluating a new offer or trying to optimize your current paycheck.

Step 1: Know your effective tax rate, not your marginal rate

Your marginal rate (the bracket your top dollar falls into) is always higher than your effective rate (the actual percentage of total income you pay). On a $100K salary with the standard deduction, your effective federal rate is around 13.5%, not 22%. Build your budget on the effective number.

Step 2: Max out tax-advantaged accounts first

In 2026, you can contribute up to $23,500 to a 401(k) ($31,000 if you’re 50+). Every dollar you put in reduces your taxable income. At the 22% federal bracket in a state like California, a $23,500 contribution saves you approximately $6,100 in combined federal and state taxes. You’re paying yourself instead of the government.

Step 3: Use an HSA if you’re on a high-deductible plan

The 2026 HSA contribution limit is $4,300 for individuals and $8,550 for families. HSAs are triple tax-advantaged: you deduct contributions, growth is tax-free, and withdrawals for medical expenses are tax-free. No other account in the tax code offers that triple play.

Step 4: Negotiate with net pay in mind

Here’s what I tell every candidate I coach: stop saying “I want $X salary.” Instead, figure out your target take-home pay first, then work backward to the gross number you need to ask for. If you need $6,000/month after taxes in California, you need roughly $100K–$105K gross. In Texas, you need about $90K for the same take-home. Your ask should change based on geography.

Step 5: Time your income when possible

If you’re expecting a year-end bonus or RSU vest, understand how supplemental income is taxed. Bonuses are typically withheld at a flat 22% federal rate. If your effective rate is lower, you’ll get some back at filing time — but it still affects your monthly cash flow.

Decision Framework: Use Before Accepting Any Offer

This is the four-step framework I’ve used with every professional I’ve coached on job decisions. Print it out, screenshot it — whatever works.

Step 1: Calculate your take-home pay in both locations Use the formula above. Don’t skip this. A $15K difference in gross salary can easily become a $2K difference — or even flip — after taxes.

Step 2: Adjust for rent and cost of living Subtract monthly rent, groceries, transportation, and childcare costs for each city. This is where “higher salary” offers frequently lose. A useful rule: if your rent exceeds 30% of your monthly take-home, you’re financially stretched no matter how impressive the gross number looks.

Step 3: Compare benefits side by side A $5K lower salary with an employer 401(k) match of 6% and fully covered health insurance can easily outperform a $5K higher salary with no match and $400/month in insurance premiums. Do the full comparison — don’t just look at the paycheck line.

Step 4: Evaluate your savings potential After all expenses, how much can you actually save and invest each month? This is the number that builds long-term wealth. A job where you can save $1,500/month beats a “better” job where you save $400/month — even if the second one has a fancier title and a bigger gross number.

This framework alone has changed dozens of decisions I’ve personally witnessed. The offer that “obviously” wins on paper often finishes second once you run the full analysis.

The Insider View: What HR Won’t Tell You

After years on the employer side of compensation conversations, here are a few things most HR teams know but rarely volunteer:

Your total compensation is not your salary. Employer 401(k) matches, health insurance premiums paid by the company, stock options, and other benefits add 20–40% to your “real” compensation. A $100K salary with a 6% 401(k) match, employer-paid health insurance, and equity is often worth $125K–$140K in total comp. When you’re using a take-home pay calculator, you should also be running a total comp calculation alongside it.

HR benchmarks on total comp, not gross salary. When companies decide what to pay you, they’re looking at total cost of employment — not just the number on your paycheck. This means the gap between two offers might actually be smaller (or larger) than it appears when you factor in benefits.

Relocation adjustments aren’t always generous. If a company asks you to move from Dallas to New York, the cost-of-living adjustment they offer rarely covers the full gap. I’ve seen adjustments of 10–15% for moves that actually require a 30–40% pay bump to maintain the same quality of life. Run the calculator yourself — don’t rely on HR’s estimate.

The “standard deduction” conversation is changing. With the One Big Beautiful Bill Act making the higher standard deduction permanent in 2026, fewer employees are itemizing. That simplifies take-home pay calculations for most people, but it also means state and local tax (SALT) deductions — capped at $40,000 for joint filers starting 2025 — become more relevant for high earners in expensive states.

FAQ

How much tax do I pay on a $100,000 salary in the US in 2026?

On a $100K salary as a single filer using the standard deduction, you’ll pay roughly $11,300–$11,500 in federal income tax and $7,650 in FICA (Social Security + Medicare). Add state income tax — $0 in Texas, around $4,500–$5,000 in California — and your total tax burden ranges from $19,000 to $24,500 depending on location.

Which US states have no income tax in 2026?

Nine states don’t levy a broad-based individual income tax: Alaska, Florida, Nevada, New Hampshire (limited to investment income only), South Dakota, Tennessee, Texas, Washington, and Wyoming. Living in these states means your take-home pay calculator only needs to account for federal tax and FICA.

What is the Social Security wage base for 2026?

The 2026 Social Security taxable wage base is $184,500, up from $176,100 in 2025. You and your employer each pay 6.2% on earnings up to this limit. Once your income passes $184,500 in a calendar year, Social Security withholding stops — but Medicare (1.45%) continues on all earnings, with an additional 0.9% above $200,000.

Does contributing to a 401(k) reduce my take-home pay?

Yes, in the short term — but it also reduces your taxable income, which lowers your tax bill. Contributing $500/month to a traditional 401(k) reduces your paycheck by $500, but your actual income reduction is closer to $380–$420 after the tax savings. You’re effectively paying yourself at a discount.

How accurate are online take-home pay calculators?

Most reputable calculators give you a solid estimate — within 2–5% of your actual net pay. Where they fall short is on pre-tax deductions (401(k), health insurance, HSA), local taxes (city and county levies), and mid-year changes. Use them as a planning tool, not a precise prediction. For exact numbers, check your actual pay stub or consult a tax professional.

Is it better to live in a no-tax state for higher take-home pay?

Not automatically. A zero-state-tax paycheck in Wyoming doesn’t help much if job opportunities in your field are limited and salaries are 20% lower than in a high-tax state like Massachusetts. The right question isn’t “which state has the lowest tax?” — it’s “which state gives me the highest net income after taxes AND cost of living for the career opportunities available to me?”

How do I calculate take-home pay from an hourly wage?

Multiply your hourly rate by your weekly hours, then by 52 to get annual gross pay. Apply the same formula: subtract the standard deduction, calculate federal tax across the brackets, subtract FICA (7.65%), subtract state tax, and subtract any pre-tax deductions. For example, $35/hour at 40 hours/week is $72,800 gross — roughly $55,000–$60,000 take-home depending on your state.

What changed in the 2026 federal tax brackets compared to 2025?

The seven rates (10% through 37%) stayed the same, but all income thresholds increased by roughly 2–3% to account for inflation. The standard deduction rose to $16,100 for single filers and $32,200 for married filing jointly. The One Big Beautiful Bill Act, signed in July 2025, made these TCJA-era rates permanent, ending years of uncertainty about whether brackets would revert to higher pre-2018 levels.

What Actually Matters

Look — your salary is a vanity metric. I know that sounds harsh, but after counseling hundreds of professionals through job changes, relocations, and negotiations, this is the one truth that separates people who build wealth from people who just chase bigger numbers on offer letters.

The professionals who get ahead aren’t the ones earning the highest gross salary. They’re the ones who understand what they actually keep. They use a take-home pay calculator before every career decision. They negotiate based on net income, not headline numbers. They pick the state, the benefits package, and the 401(k) match that maximizes their real financial position — not the one that sounds best at a dinner party.

Run the math. Then decide.

Emily Carter is a career coach and former McKinsey talent advisor with 15+ years of experience helping professionals navigate career transitions, promotions, and high-stakes job decisions. She has advised professionals across consulting, technology, finance, and corporate leadership roles on offer negotiations, career positioning, and long-term growth strategy.

Role: Career Coach & Ex-McKinsey Talent Advisor: Focuses on helping professionals make smarter career moves—switching jobs, negotiating offers, and long-term career growth. She blends structured thinking with real-world coaching insights.