If you’re relying solely on employer life insurance, here’s the uncomfortable reality: you’re almost certainly underinsured. I’ve advised hundreds of mid-career professionals through job transitions, layoffs, and benefits reviews over 18 years — and this is the financial blind spot I see most often. People assume the coverage that comes with their job is enough. It isn’t.

Most group life insurance policies cover 1x your annual salary. Some employers offer up to 2x or 3x. Meanwhile, every credible financial planning benchmark — from IRDAI in India to LIMRA in the US — recommends at minimum 10–15x your income to adequately protect your family. There’s a massive gap between those two numbers, and most professionals have never stopped to think about it.

This guide cuts through the noise. By the time you finish reading, you’ll know exactly whether your current coverage is sufficient, when supplemental life insurance makes sense, and what the smartest move is for someone at your career stage.

Quick Answer

For most working professionals with dependents, debts, or financial obligations, employer life insurance alone is not enough. It typically covers 1–3x your salary, while you need 10–15x for genuine protection. An independent term life policy — bought young and held personally — is the smartest complement to whatever your employer provides.

What Is Employer-Provided Life Insurance?

Employer life insurance — technically called group life insurance — is a death benefit policy your company purchases for its employees, usually at zero or very low cost to you. It’s bundled into your benefits package alongside health insurance, PF contributions, and paid leave.

The structure is almost always the same, regardless of whether you’re in India, the US, or the UK. Your employer pays a flat premium rate for a group policy covering all employees. Because it’s a group arrangement, individual underwriting is minimal — you don’t need a medical exam to enroll, which is genuinely useful if you have any pre-existing conditions.

Here’s what it typically looks like in practice:

- Basic life coverage — usually 1x your annual salary, provided at no cost to you

- Optional supplemental add-on — you can often purchase additional coverage (2x to 5x salary) at group rates through payroll deductions

- Accidental death & dismemberment (AD&D) — a separate benefit many employers include, covering accidental death at a higher payout

- Dependent coverage — some plans extend smaller coverage amounts to your spouse or children

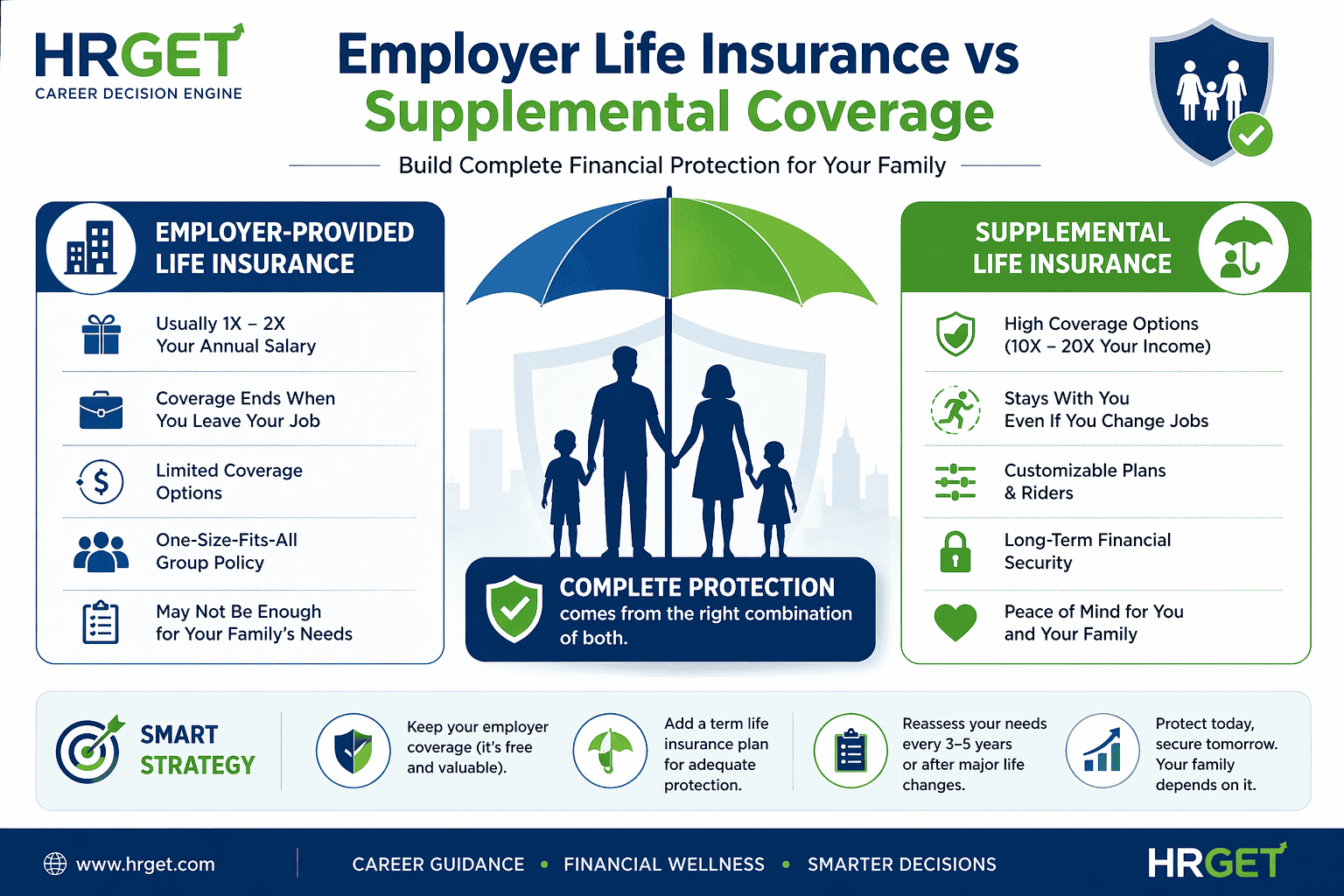

The free basic coverage is legitimately valuable. Don’t dismiss it. But once you understand what it doesn’t cover — and what happens the moment your employment ends — you’ll see why it can’t be the foundation of your family’s financial protection.

How Much Coverage Do You Actually Get?

Let’s put hard numbers on this. Here’s how employer life insurance typically breaks down across common salary levels — in both India and the US, since our audience spans both markets:

| Coverage Type | India (₹40 LPA salary) | US ($90K salary) | Typical Limit |

|---|---|---|---|

| Basic (free) | ₹40 lakh | $90,000 | 1x annual salary |

| Supplemental (paid add-on) | Up to ₹2 crore | Up to $450,000 | 3–5x salary |

| What you actually need | ₹4–6 crore | $900K–$1.35M | 10–15x salary |

| The gap (basic only) | ~₹3.6–5.6 crore short | ~$810K–$1.26M short | Significant |

That gap isn’t a minor shortfall. For most people with a home loan, dependents, or financial obligations, the difference between what their employer provides and what their family actually needs is enormous. And most professionals I’ve worked with have never done this calculation.

Insider View

From conversations with benefits consultants at Fortune 500 companies: the 1x salary benchmark wasn’t designed to replace your income. It was designed to cover immediate funeral expenses and give your family a few months of breathing room. It’s a gesture of goodwill from your employer — not a financial plan.

Why Employer Life Insurance Usually Falls Short

Coverage amount is only part of the problem. The deeper issues are structural — and they affect every professional regardless of how generous their employer’s benefits appear on paper.

1. It disappears the moment you leave

This is the biggest risk most people never think about until it’s too late. Group life insurance is employment-linked. The day you resign, get laid off, or take a career break — coverage ends. No grace period. No automatic conversion. If something happens to you during your job transition (which can last weeks or months), your family has nothing.

In 2025–2026, mid-career professionals are changing jobs every 2–4 years on average. That means your coverage resets repeatedly throughout your career — and there will be gaps. The longer your job searches, the bigger those gaps get.

2. The coverage math doesn’t add up for anyone with real obligations

The 10–15x income rule exists for a concrete reason: your dependents need to replace your earning power for a decade or more, not just cover your outstanding loan balance. That means living expenses, children’s education, your spouse’s ability to rebuild financially — none of which a 1x or even 3x employer plan comes close to covering.

3. You can’t control it

Employers can and do change benefits — reducing coverage caps, switching insurers, or eliminating programs entirely during cost-cutting cycles. I’ve seen this happen at companies that seemed rock-solid. Your family’s protection shouldn’t depend on decisions made in a boardroom you’re not in.

4. Costs increase as you age

If you rely primarily on employer supplemental coverage — the add-on you pay for through payroll — be aware that most group plans re-price annually based on your age bracket. What costs you ₹800/month at 32 might cost ₹2,200/month at 44. An independent term policy bought at 28 locks in a rate that doesn’t move.

5. Customization is minimal

You can’t add riders for critical illness, waiver of premium, or accidental disability to a group policy in the same way you can with an individual plan. For professionals with health concerns or family medical history, those riders can be genuinely important.

When You Do Need Supplemental Coverage

Let me be direct: not everyone needs additional life insurance on top of their employer plan. If you’re single, debt-free, and have no financial dependents — your employer’s basic coverage is probably fine as a short-term arrangement.

But you need supplemental life insurance if any of the following apply:

- You have a spouse or partner who depends on your income — even partially

- You have children, or plan to within the next 5 years

- You support aging parents financially

- You have a home loan, personal loan, or education loan outstanding

- Your family’s monthly survival depends on your continued employment

- You’ve recently had a significant salary increase that your coverage hasn’t caught up with

- You’re planning a career transition, sabbatical, or entrepreneurial leap in the next 2–3 years

That last one is underappreciated. If you’re planning to leave corporate life to start a business — which many professionals in their 30s are — the window between leaving your job and establishing a new income stream can be 12–24 months. During that entire period, your employer coverage is gone. An independent policy bridges that gap.

Warning

Many professionals assume they’ll “sort out life insurance” after their next job starts. During the gap between jobs — which can be weeks or months — you have zero employer coverage. If you have dependents, this is an unacceptable risk to leave unaddressed.

Real Scenario: Where Professionals Get This Wrong

Real Scenario

Rahul, 34, Senior Product Manager — Bengaluru

Rahul earns ₹40 lakh/year. His employer provides ₹40 lakh in basic coverage — which feels like a lot. He also has a home loan of ₹1.2 crore, a spouse who works part-time, and a 4-year-old daughter. He’s been meaning to “look into term insurance” for two years.

Here’s the math if something happened to Rahul today: The ₹40 lakh payout goes entirely toward the home loan — and still leaves ₹80 lakh outstanding. His wife and daughter get nothing for living expenses, nothing for education, and nothing to replace his ₹40 lakh annual income stream. On a 10x income basis alone, Rahul needs ₹4 crore in coverage. He has ₹40 lakh. He’s 90% underinsured.

A ₹2 crore term policy bought at 34 for a non-smoker in good health costs approximately ₹18,000–22,000 per year. That’s less than ₹2,000/month to cover the gap. The cost of not doing it is catastrophic for his family.

Rahul’s situation isn’t unusual — it’s nearly universal among professionals I’ve coached in the 30–40 age bracket. The home loan alone often exceeds total employer coverage by a multiple of 2 or 3.

Types of Supplemental Life Insurance Compared

When you decide to buy additional coverage, you’ll encounter several options. Here’s a clear comparison of what’s actually relevant for most working professionals:

| Type | Best For | Cost | Portable? | Verdict |

|---|---|---|---|---|

| Individual Term Life | Most professionals aged 25–45 | Low (locked in at purchase) | Yes — stays with you | Best choice for 90% of cases |

| Employer Supplemental Add-On | Short-term gap coverage, no medical exam | Medium (rises with age) | No — lost at job change | Convenient but not a long-term solution |

| Whole Life / ULIP | Estate planning, high-net-worth individuals | High | Yes | Not suitable if primary goal is protection |

| Group Term via Professional Association | Self-employed / freelancers without employer benefits | Low-Medium | While membership active | Better than nothing for freelancers |

Term life insurance is the answer for the vast majority of working professionals. It’s pure protection — no investment component, no cash value, no complexity. You pay a fixed premium for a fixed period (typically 20–30 years), and if you die during that period, your family receives the full sum assured. Clean, affordable, and exactly what most families need.

Don’t let anyone sell you a ULIP or whole life policy by framing it as “insurance plus investment.” Keep those two things entirely separate — it’s almost always the financially better decision.

How Much Extra Coverage Should You Buy?

Use this framework — the same one I walk senior leaders through when they’re reviewing their personal financial picture:

Calculate your income replacement need: Multiply your annual take-home income by 10–12 for a conservative estimate, or 15 if you have young children and a long financial runway to protect.

Add outstanding liabilities: Home loan balance + personal loan + education loan + any guarantees you’ve signed.

Add future obligations: Estimated cost of children’s higher education (₹30–50 lakh per child in India; $150K+ in the US), and any other commitments you’d want to cover.

Subtract existing assets: Savings, EPF/401k balance, other investments that your family could liquidate if needed.

Subtract existing coverage: Employer basic plan + any existing policies.

The result is your coverage gap — what you need to buy independently.

A simple example: Professional earning ₹50 LPA, home loan of ₹1.5 crore, one child aged 6, existing savings of ₹40 lakh, employer coverage of ₹50 lakh. Income replacement need: ₹5–7.5 crore. Add home loan: ₹1.5 crore. Add education: ₹50 lakh. Subtract savings and employer coverage: ₹90 lakh. Independent coverage needed: approximately ₹6.5–9 crore.

That sounds like a lot, but a ₹1 crore term policy from a leading insurer like LIC, HDFC Life, or Max Life costs roughly ₹8,000–15,000/year for a 30–35 year old non-smoker. For ₹6 crore coverage at those ages, you’re typically looking at ₹50,000–90,000 annually — less than the EMI on a mid-range car, for protection that genuinely covers your family.

Smart Strategy: The Optimal Coverage Setup

Here’s the approach I recommend to every professional I work with — and it’s simpler than most financial advisors make it sound:

Pro Tip

The Layered Coverage Model: Treat your employer’s plan as Layer 1 (a bonus you didn’t pay for). Build Layer 2 with your own independent term policy that covers your real needs. For high earners with ₹75L+ annual income, consider splitting Layer 2 across two separate term policies — bought at different ages — so you can reduce coverage as debts get paid off without cancelling your entire policy.

The four-step implementation:

Step 1 — Accept the employer coverage as a windfall, not a plan. Keep it. It’s free money. But don’t let it make you complacent about your actual gap.

Step 2 — Buy your primary independent term policy now, not later. Every year you wait is a year of higher premiums locked in for the life of the policy. A 28-year-old buying a ₹2 crore, 30-year term policy might pay ₹14,000/year. At 36, that same policy could cost ₹24,000+. That difference compounds over 30 years into a significant sum.

Step 3 — Don’t over-rely on employer supplemental add-ons. They’re not portable, costs rise with age, and they evaporate the moment you change jobs. They’re a convenient short-term bridge — not a long-term strategy.

Step 4 — Reassess every 3–5 years. Life changes — salary jumps, new loans, additional children, salary increases — all alter your coverage needs. Your insurance strategy should keep pace with your career trajectory.

Common Mistakes That Leave Families Exposed

Common Mistakes

- “My company gives me coverage, so I’m covered.” The most dangerous assumption. Usually 1x salary. Rarely adequate. Always temporary.

- Waiting until after the next job offer. Gap periods between jobs are real. They’re unpredictable. Don’t leave your family unprotected during a career move.

- Treating life insurance as an investment. ULIPs and endowment plans aren’t bad products in isolation — but if your goal is protecting your family’s financial future, pure term insurance gives you dramatically more coverage per rupee or dollar paid.

- Ignoring inflation on coverage amounts. ₹1 crore today does not have the purchasing power of ₹1 crore in 15 years. Build in a margin — or buy a second policy at a later life stage to top up coverage.

- Never reviewing coverage after salary jumps. If you went from ₹20 LPA to ₹45 LPA in five years (common in tech and consulting), your 10x coverage need more than doubled. Your old policy didn’t grow with you.

The Verdict

Employer life insurance is a starting point — not a finish line. For any professional with dependents, debt, or financial obligations, it leaves a gap that’s not just inconvenient — it’s potentially catastrophic for the people you’re responsible for.

The solution is straightforward: accept the free employer coverage as a bonus layer, then build your real financial protection independently with a term policy you control, at premiums locked in while you’re young and healthy. It’s one of the highest-ROI financial decisions you’ll make in your 30s.

The cost of acting now is modest. The cost of waiting — or assuming you’re already covered — can be enormous for the people who depend on you.

Frequently Asked Questions

Is employer life insurance enough?

In most cases, no. Employer life insurance typically covers only 1–3x your annual salary, while financial planning benchmarks recommend 10–15x your income to adequately protect dependents, cover debts, and replace lost income. For anyone with a home loan, children, or aging parents to support, employer coverage alone leaves a significant gap that an independent term policy needs to fill.

What happens to employer life insurance if I leave my job?

You lose the coverage. Most group life insurance policies terminate on your last day of employment — whether you quit, are laid off, or take a career break. Some plans offer a conversion option to an individual policy, but the premium you’d pay as an individual is usually far higher than a standalone term policy bought when you were younger and healthy. During any job transition, you have zero employer coverage.

Should I buy term insurance even if I have employer coverage?

Yes, absolutely. Think of your employer’s plan as a bonus layer — not your foundation. An independent term policy is portable, stays with you regardless of job changes, and can be bought at very low premiums when you’re young. It gives your family real, reliable protection that doesn’t disappear if your employment situation changes, which it will multiple times in a typical career.

Is supplemental life insurance through employer worth it?

It’s a reasonable short-term convenience — especially if you can enroll without a medical exam and need a quick coverage boost. But it shouldn’t replace a personal term policy. Employer supplemental coverage isn’t portable, costs tend to increase as you age, and coverage limits are often capped well below what your family genuinely needs. Use it as a top-up bridge, not your primary safety net.

How much life insurance do I really need?

The standard benchmark is 10–15x your annual income, plus outstanding debts (home loan, personal loan), plus projected child education costs, minus existing savings and investments. For a professional earning ₹40 lakh/year in India or $90,000 in the US, that typically means ₹4–6 crore or $900K–$1.35M in total coverage — far beyond what any employer plan provides.

When is the best time to buy life insurance?

As early as possible — ideally in your mid-to-late 20s, right after you land your first serious job. Premiums on term policies are calculated largely on age and health status at purchase. A ₹1 crore term policy bought at 28 can cost less than half what it costs at 38 for the same coverage period. Waiting is an expensive habit in the life insurance context.

Can I have multiple life insurance policies?

Yes, and for high-income professionals it’s often the smarter approach. Splitting coverage across two or three term policies — bought at different life stages — gives you flexibility to reduce coverage as your home loan is paid off and financial obligations decrease. It can also lower your total premium outlay over time compared to one large policy. There’s no rule limiting how many policies you can hold.

Related Reading: Understanding your full employee benefits package — not just life insurance — is one of the highest-leverage moves in your career. Read our guide on how to read and negotiate your employee benefits package to make sure you’re extracting every rupee and dollar of value from your compensation.

Jonathan Reed: Executive Career Strategist & Leadership Advisor | Former Partner, McKinsey & Company | Executive Coach to Amazon & Unilever Leaders | 18+ Years in Career Strategy

Jonathan Reed spent nearly two decades as a Partner at McKinsey & Company, where he advised organisations on leadership development, talent strategy, and organisational design across the US, UK, and Asia. Since leaving consulting, he has worked as an executive coach to senior leaders at Amazon, Unilever, and a clutch of high-growth scale-ups — helping them navigate promotions, career pivots, and the unwritten rules of visibility and influence at the top. Based between London and New York, Jonathan writes for HRGet.com to give working professionals an honest look at how careers actually scale — and why so many talented people stall without ever knowing why.