Losing your job is stressful enough. But here’s what nobody warns you about: your health insurance doesn’t just pause — it disappears, usually by the end of the month you were let go. That’s when COBRA health insurance enters the picture, and most people either overpay for it blindly, blow the enrollment deadline, or never realize there were cheaper options the whole time.

I’ve helped dozens of professionals navigate this exact moment — the panicked “what do I do about insurance?” call that comes 48 hours after a layoff notice. After seeing the same costly mistakes repeat, I put this guide together. By the time you finish reading, you’ll know exactly what COBRA costs you, what the deadlines actually mean (including a legal strategy most people don’t know), and whether you should bother with COBRA at all.

What Is COBRA Health Insurance (Plain-English Explanation)

COBRA stands for the Consolidated Omnibus Budget Reconciliation Act — a federal law passed in 1986. The practical translation: if you lose your job or experience certain life events, you have the legal right to keep your employer’s group health plan running for a limited period.

That sounds like a lifesaver. And it can be — under the right circumstances. But it comes with a price tag that catches most people completely off guard.

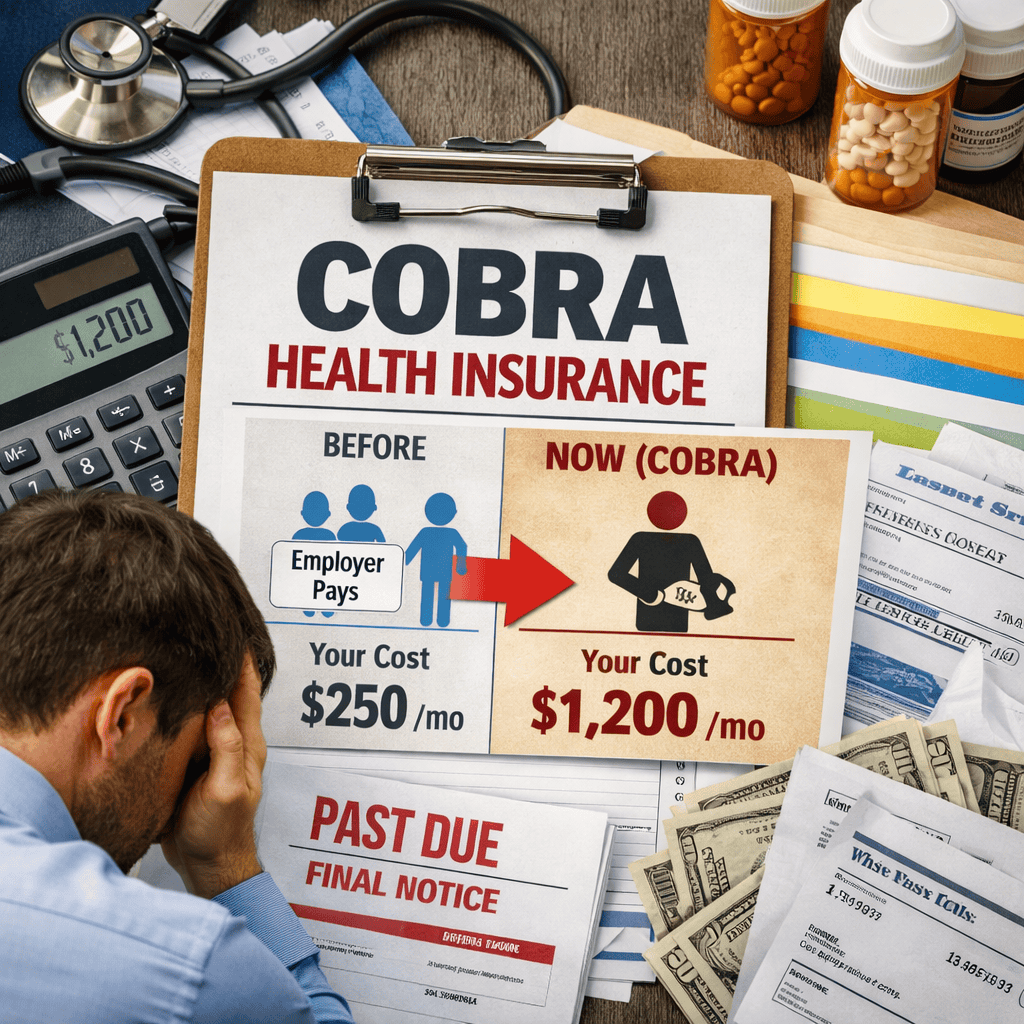

Here’s the thing: while you were employed, your employer was quietly subsidizing a huge chunk of your monthly health premium. Most workers never notice because it comes out of payroll before you ever see it. COBRA strips away that subsidy. You now owe the full premium — plus an administrative fee.

Same plan. Same network. Same doctors. Just a dramatically higher price tag — paid entirely by you.

Who Qualifies for COBRA Coverage

COBRA isn’t available to everyone. The federal law applies to employers with 20 or more employees who offer group health insurance. If you worked for a smaller company, check whether your state offers a “mini-COBRA” equivalent — many do, including California, New York, and Texas, though the rules vary.

You qualify for federal COBRA if you experienced a qualifying event, which includes:

- Voluntary resignation or involuntary termination (except for gross misconduct)

- Reduction in work hours that drops you below benefit eligibility

- Divorce or legal separation (for a spouse on your plan)

- Death of the covered employee (for dependents)

- A dependent child aging off the plan (typically at age 26)

Coverage duration depends on the qualifying event. Job loss or reduced hours typically gives you 18 months of continued coverage. Certain circumstances — like disability or divorce — can extend that to 36 months.

One thing HR departments often don’t volunteer: even if you were fired for cause, you may still qualify for COBRA unless the termination was specifically for “gross misconduct” — a high legal bar that most routine terminations don’t clear.

COBRA Costs: Why It’s More Expensive Than You Think

This is where people get genuinely shocked. And I don’t blame them — the jump from what you were paying to what COBRA costs feels almost punitive.

The math is simple but brutal. Your employer was covering 60–80% of your monthly premium as part of your total compensation. You only saw the remaining slice come out of your paycheck. The moment you’re on COBRA, that employer contribution disappears entirely. You pay the full premium — and then up to a 2% administrative fee on top of that.

| Coverage Type | Total Monthly Premium | What You Paid Before | COBRA Cost |

|---|---|---|---|

| Individual | ~$600/month | ~$120–$180 | ~$612/month |

| Employee + Spouse | ~$900/month | ~$200–$280 | ~$918/month |

| Family Plan | ~$1,200/month | ~$280–$400 | ~$1,224/month |

These are ballpark figures based on 2025–2026 national averages, and they vary significantly by plan type, employer size, and geography. But the pattern holds: your out-of-pocket cost typically jumps 3 to 5 times overnight.

For a family plan, that’s potentially $14,000–$15,000 per year in premiums — paid post-tax, while you’re unemployed. It adds up fast.

COBRA Deadlines — The Part Most People Get Wrong

This section can literally save or cost you thousands. Pay attention here.

The COBRA process follows a specific sequence of deadlines, and missing any of them has serious consequences.

The Deadline Sequence

- Your employer must notify the health plan administrator within 30 days of your qualifying event.

- The plan administrator then has 14 days to send you an election notice (sometimes called a COBRA notice).

- You have 60 days from the date of that notice — or the date your coverage ended, whichever is later — to elect COBRA.

- Once you elect COBRA, you have 45 days to make your first payment, which covers all retroactive premiums back to when your coverage ended.

This retroactive feature is one of the most powerful and underused aspects of COBRA. It effectively lets you carry COBRA as a 60-day “insurance policy on your insurance” — you only activate it if something medical actually happens.

Real Scenario: What You Actually Pay Month-to-Month

📋 The Numbers for a Real Layoff Situation

Profile: Marketing director, 38 years old, laid off. Annual salary was $110,000. Family of three, employer-sponsored PPO plan.

Before layoff: Total premium was $1,200/month. He paid $320/month out of paycheck; employer covered $880.

After layoff (COBRA): Full premium of $1,200 plus 2% admin fee = $1,224/month out of pocket.

Monthly jump: From $320 to $1,224 — nearly 4x increase. That’s an extra $10,848/year he wasn’t planning for.

What he actually did: Waited 45 days, found a marketplace silver plan for $340/month after subsidy (his projected income for the year dropped significantly post-layoff). He kept COBRA on standby as a fallback and never needed to activate it.

That decision alone saved him over $10,000. And he wasn’t doing anything unusual or risky — he was just using the system the way it’s designed to work, which most people simply don’t know about.

When COBRA Makes Sense (and When It Absolutely Doesn’t)

Look, I’m not here to tell you COBRA is always the wrong choice. It’s genuinely the right call in specific situations. The problem is that most people default to it out of habit or fear — not because they actually evaluated the tradeoffs.

Choose COBRA if:

- You’re mid-treatment — surgery, chemotherapy, a high-risk pregnancy, or any ongoing specialist care where switching networks would disrupt your care

- You have a new job starting within 30–60 days and just need a clean bridge with no plan changes

- You or a dependent have a complex chronic condition where the current network is genuinely irreplaceable

- Your income won’t drop much and marketplace subsidies won’t apply to you

Skip COBRA if:

- You’re generally healthy with no ongoing treatments or prescriptions

- Your household income will drop significantly — you’ll likely qualify for marketplace subsidies or Medicaid

- You’re expecting to be unemployed for more than 2–3 months

- You’re paying over $800/month for individual coverage — the math rarely works in your favor

The honest truth that most insurance articles won’t say out loud: COBRA is designed for the short-term bridge, not the long-term solution. If you’re looking at 4+ months without employer coverage, the cost difference between COBRA and a subsidized marketplace plan can be staggering.

Cheaper Alternatives to COBRA in 2026

This is where the real money is saved. And yet most people, in the stress of a layoff, never look past COBRA. Here are your actual options:

1. ACA Marketplace Plans (HealthCare.gov)

Job loss is a qualifying life event, which means you have a Special Enrollment Period of 60 days to sign up for a marketplace plan outside of open enrollment. This is your most important alternative to investigate first.

The key variable is your projected annual income for the year. If it drops significantly after a layoff — which it usually does — you may qualify for substantial premium tax credits. Many professionals in the $40,000–$70,000 income range pay $50–$300/month for silver-tier marketplace plans after subsidies. Compare that to $800–$1,200 for COBRA on a family plan.

Go to HealthCare.gov, enter your projected income, and run the numbers before you make any decision.

2. Medicaid

If your income will genuinely drop to low levels — especially if you’re the sole earner and your household has limited savings — Medicaid may cover you at little to no cost. In states that have expanded Medicaid under the ACA, the income threshold for a single adult is around $22,000/year (2026 estimates). Families can qualify at higher income levels.

There’s no enrollment window for Medicaid — you can apply any time of year if you qualify. Don’t rule it out because of pride; it exists precisely for situations like this.

3. Spouse’s Employer Plan

Often overlooked because it feels inconvenient. But if your spouse has employer-sponsored insurance, your job loss is a qualifying event that triggers a Special Enrollment Period on their plan too — typically 30 days. Group plans through an employer almost always cost less than COBRA.

4. Short-Term Health Insurance

Short-term plans are low-premium, limited-coverage plans available outside of ACA rules. They don’t cover pre-existing conditions, mental health, or preventive care in most cases. Use these only as a genuine last resort for a gap of a few weeks — not as a primary coverage strategy.

Smart Strategy: The 60-Day Decision Framework

Here’s the tactical approach I’d give a friend going through a layoff right now. Don’t just “pick COBRA” — work the window strategically.

Days 1–7: Don’t elect COBRA yet. Breathe. Your coverage typically extends through the end of the month you were terminated, so you’re not immediately uninsured in most cases.

Days 7–21: Go to HealthCare.gov and run the numbers on marketplace plans using your projected income for the year (not your old salary — your actual expected income for the remaining months of the year). Check if your spouse’s plan has an enrollment window opening up. Check Medicaid eligibility.

Days 21–45: Evaluate your health risk. Do you have any ongoing treatments, scheduled procedures, or prescriptions that depend on your current network? If yes, COBRA may be worth the cost for continuity. If no, a marketplace plan is almost certainly cheaper.

Days 45–59: Make your final call. If you’ve found a better alternative, enroll in it and let the COBRA window close. If you need COBRA — for network continuity or because you’ve already had a medical event in this window — elect it now and make the retroactive payment.

Common Mistakes That Cost People Thousands

Mistake 1: Electing COBRA on autopilot. The election form shows up in the mail and you fill it out without comparing anything. You’re now locked into $1,200/month when you could have paid $250.

Mistake 2: Assuming marketplace plans are low quality. This perception is stuck in 2014. In 2026, silver-tier marketplace plans often have comparable networks and deductibles to mid-tier employer plans — especially in metro areas. Don’t dismiss them without checking.

Mistake 3: Missing the 60-day COBRA window entirely. If you let this deadline pass without electing COBRA and without enrolling elsewhere, you may end up uninsured with no retroactive option. Set a calendar reminder. This deadline is absolute.

Mistake 4: Not accounting for the subsidy cliff. If your income is near subsidy eligibility thresholds on the marketplace, a small income difference can result in a very large premium difference. Run the actual numbers — don’t estimate.

Mistake 5: Forgetting dental and vision. COBRA can extend these too, if they were part of your employer plan. Many people assume it’s health-only. Confirm what’s included in your specific election notice.

Frequently Asked Questions About COBRA

How much does COBRA typically cost per month in 2026?

For individual coverage, expect to pay $500–$700/month. Family plans commonly run $1,100–$1,400/month. The exact amount depends on your former employer’s plan and location. The key is that you’re now paying 100% of the premium plus up to a 2% administrative fee — compared to the 20–40% you likely paid while employed.

Can I get COBRA if I quit voluntarily (not laid off)?

Yes. Voluntary resignation qualifies as a COBRA-triggering event the same way a layoff does. The only exception is termination for gross misconduct — a specific legal threshold that most terminations don’t meet. If you resigned, you’re eligible as long as your employer had 20+ employees and offered group health coverage.

Is COBRA coverage retroactive if I wait to enroll?

Yes — this is one of COBRA’s most important and underused features. If you elect COBRA within your 60-day window, coverage goes back to the date your employer-sponsored insurance ended. You’ll need to pay all retroactive premiums, but you won’t have a coverage gap. This means you can legitimately wait and see before committing.

What’s the difference between COBRA and marketplace plans?

COBRA keeps your exact existing plan — same network, same doctors, same deductible — but you pay the full premium. Marketplace plans are new plans purchased through HealthCare.gov, often with income-based subsidies that significantly reduce cost. Marketplace plans may have different networks, so if you have a specific doctor or treatment in progress, verify they’re covered before switching.

Can I switch from COBRA to a marketplace plan mid-year?

Yes, but timing matters. You can drop COBRA voluntarily and enroll in a marketplace plan during open enrollment (November–January) or if you experience another qualifying life event. Simply canceling COBRA mid-year without a qualifying event doesn’t trigger a Special Enrollment Period, so you’d need to wait for open enrollment.

Does COBRA cover dental and vision?

Only if those were part of your employer-sponsored plan and they’re listed in your COBRA election notice. Many employers offer dental and vision as separate benefit elections, which means they can be continued under COBRA independently of your medical plan. Check your specific election notice — don’t assume.

What happens when COBRA runs out after 18 months?

You’ll need to transition to another plan. Losing COBRA coverage after the maximum period is a qualifying life event, which opens a Special Enrollment Period on the marketplace. You won’t be left without options, but plan ahead — don’t let COBRA expire without having a replacement lined up. Start comparing marketplace plans at least 60 days before your COBRA end date.

The Bottom Line on COBRA Health Insurance

Here’s the framing that matters: COBRA is a right, not a recommendation. The law gives it to you as an option, not as the obvious default. Most people elect it because they’re scared, busy, and don’t realize they have alternatives — and then spend 6 months paying premiums they didn’t need to.

If you’re in the middle of active medical treatment or you expect a new job within 4–6 weeks, COBRA is a legitimate and often smart choice. In every other situation, spend a few hours on HealthCare.gov before you sign anything. A subsidized marketplace plan will almost certainly cost you less — sometimes dramatically less.

The 60-day election window is your friend, not a pressure tactic. Use it to compare, decide, and then act. That’s the smartest thing you can do with your COBRA health insurance decision in 2026.

Related read: What Benefits Are You Entitled to After a Layoff? (Complete US Guide)

Michael Reeves | Former Senior Counsel, Littler Mendelson | Severance & Restructuring Specialist | 18+ Years in Employment Law

Author bio: Michael Reeves spent nearly two decades as Senior Counsel at Littler Mendelson — one of the world’s largest employment law firms — advising on mass layoffs, corporate restructurings, and severance negotiations for Fortune 500 companies across the US and Europe. He has worked both sides of the table: structuring cost-efficient separation packages for employers and, more recently, helping employees understand exactly where their leverage lies. Based between Chicago and London, Michael writes for HRGet.com to demystify the legal and financial dimensions of layoffs — so employees stop leaving money on the table.