I’ll be honest — the number on your severance agreement and the number that hits your bank account are two very different things.

I’ve processed hundreds of severance packages across tech, finance, and manufacturing. And the single biggest mistake I see? Professionals planning their post-layoff finances around the gross figure. A $30,000 severance sounds solid until you realize you’re walking away with $18,000 to $20,000 after withholding.

This severance tax calculator helps you estimate what you’ll actually receive after federal, state, and FICA taxes. More importantly, this guide explains why those deductions happen — and what you can do about them before you sign anything.

Table of Contents

- What This Severance Tax Calculator Does

- How Severance Is Taxed in the US (2026 Rules)

- Lump Sum vs. Salary Continuation: The Tax Difference Most People Miss

- Step-by-Step: Estimate Your Net Severance

- Real Scenario: What a $30K Severance Actually Looks Like

- Smart Strategies to Reduce Your Severance Tax Hit

- 5 Costly Mistakes People Make With Severance Taxes

- The Insider View: What HR Won’t Volunteer About Severance Structure

- FAQs: Severance Tax Calculator

What This Severance Tax Calculator Does

A severance tax calculator estimates your net payout after the IRS and your state take their share. The math looks simple on paper:

Gross Severance – Federal Tax – FICA – State Tax = Net Severance

But here’s the thing. Severance isn’t taxed like your regular paycheck. It falls under IRS supplemental wage rules, which means your employer uses a different withholding method — often a flat rate that catches people off guard.

This calculator accounts for the three big deductions:

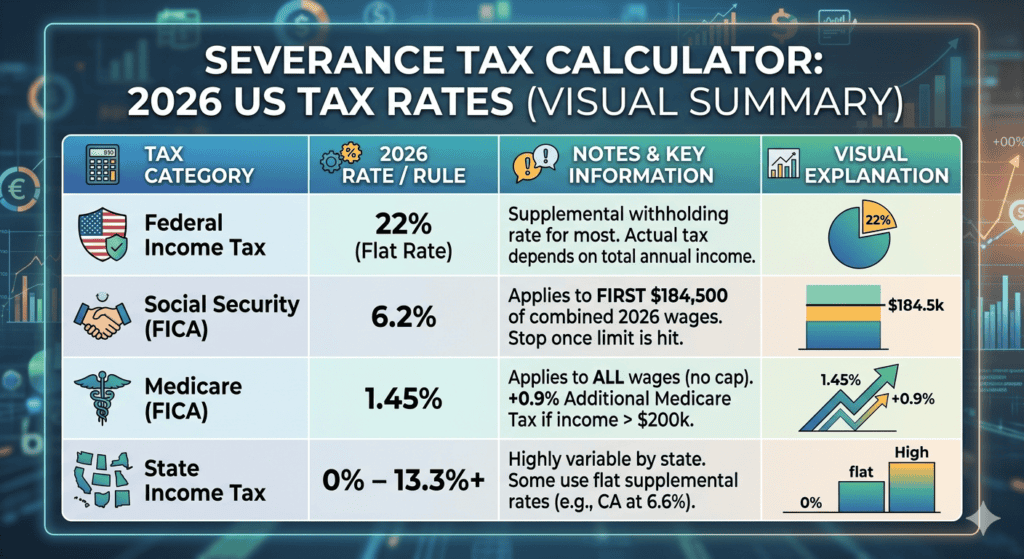

Federal withholding at the IRS supplemental rate (22% flat for most earners, 37% if your total supplemental wages for the year exceed $1 million). FICA taxes, which include Social Security at 6.2% up to the 2026 wage base of $184,500 and Medicare at 1.45% with no cap. State income tax, which ranges from 0% in states like Texas and Florida to over 13% in California.

The result? Most employees lose between 25% and 40% of their gross severance to withholding.

How Severance Is Taxed in the US (2026 Rules)

Let’s clear up the biggest misconception first: severance pay is not “bonus money” with special tax treatment. The IRS treats severance as supplemental wages — the same category as bonuses, commissions, and back pay. And supplemental wages follow their own withholding rules.

Federal Withholding: The 22% Flat Rate

Under IRS Publication 15, when an employer pays severance separately from regular wages, they typically withhold at a flat 22% federal rate. No consideration of your actual bracket, your deductions, or your filing status. Just a straight 22% off the top.

For 2026, the One Big Beautiful Bill Act permanently extended these rates from the 2017 Tax Cuts and Jobs Act. If your total supplemental wages from one employer exceed $1 million in a calendar year, the rate jumps to 37% on everything above that threshold.

Here’s what most articles won’t tell you: this 22% is withholding, not your final tax liability. Your actual tax depends on your total income for the year. If you were laid off in March and don’t earn much for the rest of the year, your effective tax rate could be significantly lower than 22%. You’d get the difference back as a refund when you file. But that refund comes 6–12 months later — and it doesn’t help you pay rent next month.

FICA: The Taxes Everyone Forgets

On top of federal income tax, your severance gets hit with:

Social Security tax at 6.2%, applied to the first $184,500 of total wages you earn in 2026. If your regular salary already pushed you past that cap before the layoff, you won’t owe additional Social Security tax on the severance. Medicare tax at 1.45% on all earnings, with no cap. And if your total income for the year exceeds $200,000 (single filers), an additional 0.9% Medicare surtax kicks in.

Combined, FICA adds roughly 7.65% for most employees — though it can be less if you’ve already exceeded the Social Security wage base earlier in the year.

State Taxes: The Wild Card

This is where geography makes a massive difference. Nine states charge zero income tax on wages: Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington, and Wyoming. If you’re in one of these states, you just saved yourself 5–13% on your severance.

But in high-tax states, the bite is real. California’s top rate reaches 13.3%. New York state goes up to 10.9%, and if you’re in New York City, add another 3.876% on top. Oregon, Minnesota, and New Jersey also have rates above 9%.

Some states also have their own supplemental wage withholding rates that differ from their standard brackets. California, for example, uses a flat 6.6% supplemental rate rather than its full bracket schedule.

Lump Sum vs. Salary Continuation: The Tax Difference Most People Miss

Here’s where smart employees gain a real edge — and most people don’t even know this is negotiable.

Lump Sum Payment

Your employer cuts one check for the full severance amount. It’s taxed immediately at the supplemental wage rate. You get a big deposit, a big tax hit, and you’re done.

Salary Continuation

Your employer keeps you on payroll for the severance period. You receive regular paychecks on the normal schedule. Taxes are withheld using the standard method — based on your W-4, your filing status, and the amount per pay period.

Why does this matter? With salary continuation, each individual paycheck is smaller, which often results in lower per-period withholding. If your severance spans months where you have no other income, the effective withholding on each check could be well below 22%.

Pro Tip: If you expect to earn significantly less in the second half of the year — whether from unemployment or a slower job search — salary continuation almost always results in lower total withholding. It also keeps your health insurance active longer in many cases, since you’re technically still on payroll. I’ve seen this save employees anywhere from $1,500 to $5,000 on a $50K severance, depending on the state and timing.

Step-by-Step: Estimate Your Net Severance

Even without a calculator, you can ballpark your net severance in five minutes. Here’s the framework I walk employees through in exit meetings.

Step 1: Start with gross severance. This is the total dollar amount in your separation agreement. Let’s use $30,000 as an example.

Step 2: Subtract federal withholding. For most earners, that’s 22% flat. $30,000 × 22% = $6,600 withheld for federal taxes.

Step 3: Subtract Social Security tax. 6.2% of the severance — but only if you haven’t exceeded the $184,500 wage base for 2026. If your YTD earnings plus severance stay below this cap: $30,000 × 6.2% = $1,860.

Step 4: Subtract Medicare tax. 1.45% on the full amount, no cap. $30,000 × 1.45% = $435. If your total income exceeds $200,000, add 0.9% additional Medicare tax.

Step 5: Subtract state tax. This varies. For California at 6.6% supplemental rate: $30,000 × 6.6% = $1,980. For Texas: $0.

Your estimate:

In California: $30,000 – $6,600 – $1,860 – $435 – $1,980 = $19,125 net In Texas: $30,000 – $6,600 – $1,860 – $435 – $0 = $21,105 net

That’s a 36% cut in California and a 30% cut in Texas — on the same severance package.

Real Scenario: What a $30K Severance Actually Looks Like

Let me walk through a disguised but realistic case I’ve seen play out many times.

The situation: A product manager in San Jose earns $140,000 annually. The company conducts a reduction-in-force in April. She receives 3 months’ base pay as severance — roughly $35,000 gross — paid as a lump sum.

By April, she’s already earned about $46,600 in regular wages. Her total income for the year (if she doesn’t find a new job) would be roughly $81,600.

What she expects: $35,000 in the bank. Enough for 4–5 months of expenses.

What she actually receives:

Federal withholding (22%): –$7,700. Social Security (6.2%): –$2,170. Medicare (1.45%): –$507.50. California state (6.6% supplemental): –$2,310.

Net deposit: ~$22,312

That’s $12,688 less than the headline number. And she planned her financial runway around $35K.

Now, here’s the twist. Because she only earns $81,600 total for the year and files as single, her actual effective federal tax rate would be around 13–14% — not 22%. She’d get roughly $2,800 back when filing taxes in early 2027. But that doesn’t help with July rent.

The takeaway: Plan your cash flow around net severance, not gross. And if you have leverage, push for salary continuation to smooth out the tax impact.

Smart Strategies to Reduce Your Severance Tax Hit

These aren’t loopholes. They’re legitimate planning moves that experienced HR professionals and tax advisors routinely recommend.

1. Negotiate salary continuation over lump sum. I covered this above, but it bears repeating. If your employer offers a choice, continuation usually wins on taxes. It also preserves benefits enrollment longer.

2. Split the payment across tax years. If you’re getting laid off in November or December, ask if the severance (or part of it) can be paid in January. If your next-year income will be lower, you could land in a lower bracket, reducing your actual tax — not just withholding.

3. Max out your 401(k) with severance dollars. Some employers allow you to direct severance contributions into your 401(k) up to the annual limit ($23,500 for 2026, or $31,000 if you’re 50+). Every dollar you contribute reduces your taxable income dollar-for-dollar. If you’ve only contributed $10,000 so far this year, you could shelter up to $13,500 of your severance from immediate taxation.

4. Contribute to an HSA if you’re on an HDHP. The 2026 HSA contribution limit is $4,400 for individuals and $8,750 for families. HSA contributions reduce your taxable income and grow tax-free. If you haven’t maxed out for the year, this is low-hanging fruit.

5. Leverage the low-income year advantage. If you remain unemployed for several months, your total annual income may be significantly lower than usual. This means the IRS withholding of 22% was too high. You’ll recover the over-withholding as a refund — but plan your cash flow knowing the refund is coming later.

5 Costly Mistakes People Make With Severance Taxes

After years of guiding employees through exits, these are the patterns I see over and over.

Mistake 1: Treating the 22% withholding as final. It’s not your tax rate — it’s a prepayment. Your actual liability depends on your total income for the year, your deductions, and your filing status. You might owe more. You might get a refund. But you won’t know until you file.

Mistake 2: Ignoring state taxes entirely. I’ve watched employees in California calculate their runway based on federal deductions alone — then get blindsided by another $2,000–$4,000 in state withholding. Always factor in your state rate.

Mistake 3: Accepting lump sum without asking about alternatives. Most companies default to lump sum because it’s simpler for payroll. But that doesn’t mean it’s your only option. I’ve seen at least 40% of severance agreements where the employee could have requested salary continuation — they just didn’t ask.

Mistake 4: Forgetting that severance can affect unemployment eligibility. In many states, receiving a lump sum severance delays when your unemployment benefits start. California, New York, and Illinois all have rules that effectively push back your eligibility window based on the severance period. Check your state’s Department of Labor guidelines before signing.

Mistake 5: Not budgeting for benefits costs. Your severance agreement ends your employer-subsidized health insurance. COBRA continuation typically costs $500–$700/month for individual coverage and $1,400–$2,100/month for family coverage. That’s money coming out of your net severance that many people don’t account for until the first bill arrives.

The Insider View: What HR Won’t Volunteer About Severance Structure

Look, I’ve sat on the HR side of these conversations. Here’s what I wish every employee knew walking in.

Severance is more negotiable than you think. Companies budget severance as a cost of the layoff. The initial offer is rarely the ceiling. I’ve seen employees negotiate from 2 weeks per year of service to 4 weeks — simply by asking and providing reasoning. The company’s risk of a wrongful termination claim or negative publicity often justifies the incremental cost.

Structure matters as much as — sometimes more than — the dollar amount. A $40,000 lump sum in California nets you roughly $24,000 to $26,000. The same $40,000 as salary continuation over 4 months, timed to bridge into a new job, could net you $28,000+ and keep your health insurance active. Same headline number, very different outcome.

Your employer optimizes for simplicity, not your tax outcome. Payroll departments prefer lump sums because they’re one transaction. Salary continuation means maintaining your payroll record, benefits enrollment, and tax reporting for months. If you want a structure that works better for you, you need to ask for it explicitly — and frame it as a reasonable accommodation, not a demand.

The separation agreement is a legal document. Read it with a lawyer. Especially the release of claims section. You’re typically giving up your right to sue in exchange for the severance. An employment attorney’s review costs $300–$500 and can be the best investment you make during a layoff.

FAQs: Severance Tax Calculator

Is severance pay taxed differently than regular salary?

Severance is classified as supplemental wages under IRS rules. While it’s subject to the same income tax brackets as your salary, the withholding method differs. Employers typically withhold a flat 22% for federal income tax instead of using your W-4 settings. Your actual tax liability, though, is calculated on total income when you file your return.

Why does my severance check look so much smaller than expected?

Because three layers of taxes hit simultaneously: 22% federal withholding, 7.65% in FICA taxes (Social Security and Medicare combined), and state income tax ranging from 0% to 13%+. In high-tax states, total deductions can reach 35–40% of the gross amount.

Can I legally reduce the taxes on my severance?

Yes, through legitimate tax planning. Strategies include negotiating salary continuation instead of a lump sum, maximizing 401(k) contributions with severance funds, contributing to an HSA, and timing payments across tax years. Each reduces your taxable income in the year of the severance.

Will I get a tax refund on over-withheld severance?

Possibly. If 22% was withheld but your actual effective tax rate for the year is lower — common if you were laid off early and didn’t earn much afterward — you’ll receive the excess back when filing your return. Use Form W-4 adjustments on any new job to avoid further over-withholding.

Is severance subject to Social Security tax?

Yes, up to the annual wage base limit of $184,500 in 2026. If your regular salary plus severance stays below this threshold, the full severance amount is subject to the 6.2% Social Security tax. If you’ve already exceeded the cap through prior earnings, no additional Social Security tax applies to the severance.

Does severance pay affect my unemployment benefits?

In many states, yes. A lump sum severance payment can delay the start of your unemployment benefits. The delay period typically equals the number of weeks your severance covers. Rules vary significantly by state — California, New York, and Illinois each handle this differently. Check with your state labor department before finalizing your agreement.

Which states don’t tax severance pay?

Nine states impose no income tax on wages or severance: Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington, and Wyoming. Employees in these states save anywhere from 5% to 13% compared to high-tax states like California or New York.

Should I take a lump sum or salary continuation for my severance?

It depends on your specific situation, but salary continuation often results in lower withholding and extended benefits. If you expect lower income for the rest of the year, continuation spreads the tax impact across smaller payments. Lump sum gives you immediate access to the full net amount. Consider your cash flow needs, state tax rates, and benefits continuation before deciding.

Your Severance Is a Financial Strategy, Not Just a Number

Here’s what I want you to remember: a severance package is the last negotiation you’ll have with your employer. And unlike salary negotiations where you have years to make up a mistake, this one is final.

Focus on net, not gross. Understand that withholding isn’t the same as your tax bill. And don’t accept the default structure without at least asking about alternatives.

Use the calculator above to estimate your real take-home amount. Then, if the numbers look tight, explore the strategies in this guide before you sign.

Next step: If you haven’t received your severance offer yet, read our severance pay calculator guide to estimate what you should be receiving — and how to negotiate for more.

Disclaimer: This calculator provides estimates based on 2026 federal supplemental wage withholding rates, FICA rates, and approximate state tax rates. It is not tax advice. Your actual tax liability depends on your complete financial situation. Consult a qualified tax professional for personalized guidance. Tax rates sourced from IRS Publication 15 (2026) and SSA wage base announcements.