Losing your job isn’t just a career shock — it’s a financial emergency. And most people don’t treat it like one until it’s too late.

Here’s the uncomfortable truth I’ve seen play out in hundreds of severance consultations over 18 years: professionals don’t fail after a layoff because they lack skills or experience. They fail because they mismanage the first 90 days. They run out of cash before they run out of opportunities.

The good news? If you manage this window correctly, you buy yourself something more valuable than a paycheck — you buy time, control, and leverage. If you don’t, you’re forced into bad decisions: accepting lowball offers, making panic moves, or accumulating debt that takes years to clear.

This guide gives you a real, practical 90-day financial plan to survive a layoff and come out stronger. No generic advice. No platitudes. Just the moves that actually work.

Understanding the 90-Day Survival Window

When a layoff hits, your financial life splits immediately into two phases: the survival phase (days 0–90) and the recovery phase (day 90+). Almost all the critical decisions happen in that first window — and almost all the critical mistakes do too.

Most people walk out the door focused on “getting a job fast.” I get it — it feels productive. But here’s what that mindset actually does: it pushes you into a reactive, rushed job search where you’re negotiating from desperation, not strength.

Your real goal in the first 90 days is not to find any job. It’s to extend your financial runway.

Runway = Total Savings ÷ Bare Minimum Monthly Expenses

Increase your runway from 3 months to 6 months and everything changes — you negotiate better offers, avoid panic decisions, and choose the right next role instead of the first available one.

Every decision in this plan is designed to move that number in your favour.

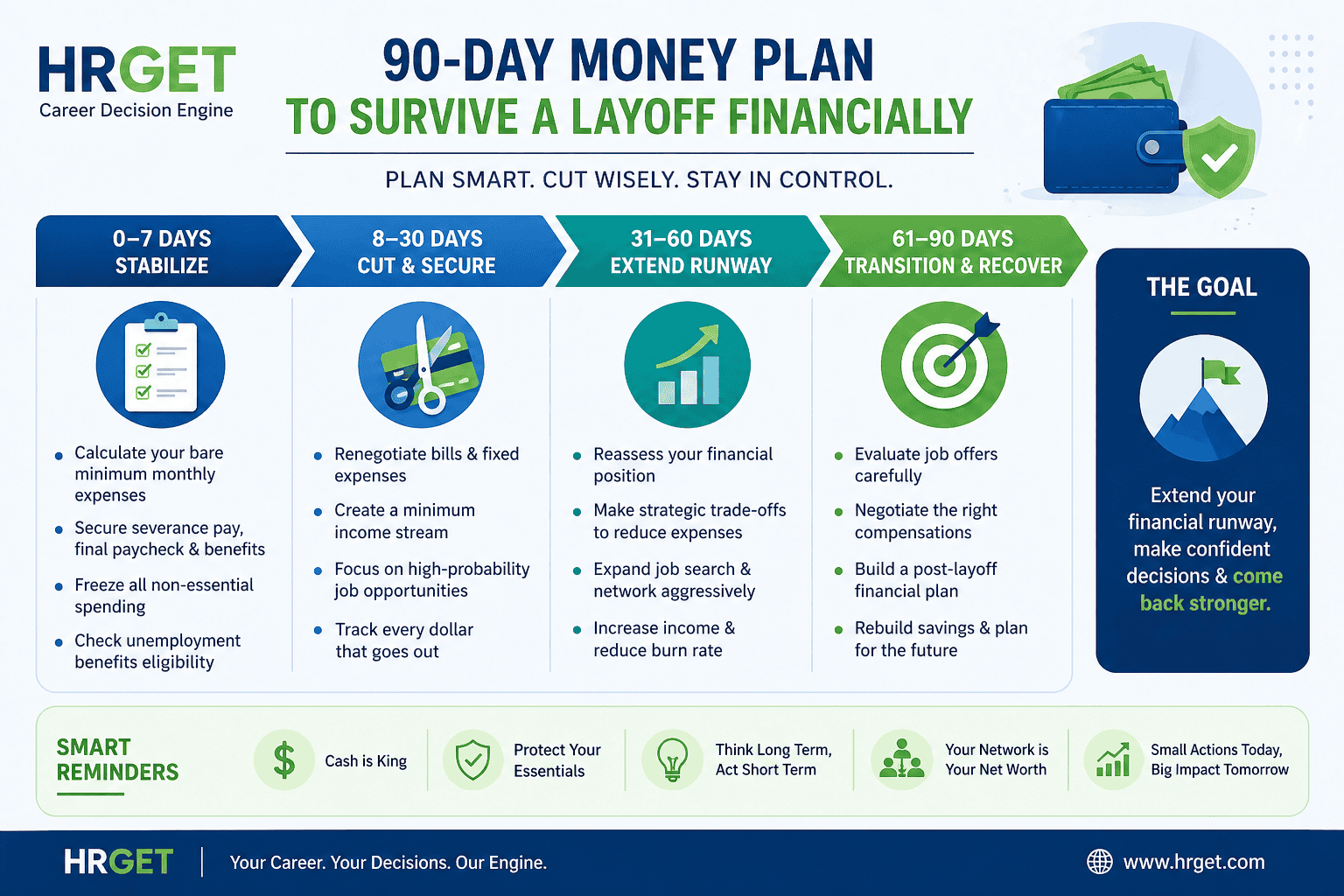

Day 0–7: Stabilize Your Finances Immediately

This is where most people mess up. They either spiral into panic or enter a kind of denial — “I’ll sort it out once things settle.” There’s no settling-in period. You need to act in the first seven days.

Step 1: Calculate Your Bare Minimum Monthly Expense (BMME)

Forget your pre-layoff lifestyle. Right now, you have one number that matters: what does it cost to keep yourself alive and housed each month?

Include only:

- Rent or mortgage EMI

- Groceries and household essentials

- Utilities (electricity, water, internet)

- Health insurance premiums

- Essential transport (fuel or transit pass)

- Minimum debt repayments

Cut immediately: Streaming subscriptions, dining out, shopping, travel, gym, SaaS tools, anything non-essential.

Once you have your BMME, divide your liquid savings by it. That’s your runway in months. If it’s under 4 months, you’re in high-risk territory and every subsequent step in this plan becomes critical.

Step 2: Lock In Every Immediate Cash Source

Don’t let administrative delays bleed you out. Within the first week, confirm and initiate:

- Severance pay — review your agreement carefully; if the package feels thin, this is the moment to negotiate (more on this below)

- Final paycheck — including any outstanding reimbursements

- Accrued PTO payout — in most US states and many countries, unused vacation must be paid out

- Unemployment benefits — file immediately; there’s often a 1–2 week waiting period, so every day of delay is money lost

- COBRA (US) or equivalent — compare the cost against marketplace plans; COBRA is often expensive but has its uses if you have ongoing medical needs

In India, this means confirming gratuity eligibility (if you’ve served 5+ years), PF withdrawal or transfer, and any notice pay owed. Delay here isn’t just inconvenient — it’s genuinely costly.

Step 3: Freeze, Don’t Just Reduce, Non-Essential Spending

“Reducing” spending is a mindset trap — it leaves room for negotiation with yourself. Freeze it instead. Cancel or pause every non-essential subscription today. This single move typically extends runway by 20–30% without touching savings. A ₹3,000–5,000/month or $60–$100/month subscription pile adds up to months of additional runway when you remove it completely.

Day 8–30: Cut Burn Rate and Secure Partial Cash Flow

You’ve stabilized. Now you move from reactive panic into deliberate control. This phase has two objectives: reduce what’s going out and start something — anything — coming in.

Renegotiate Fixed Expenses — Most People Never Do This

Call your landlord, bank, and lenders. Explain the situation. Ask for a temporary rent reduction or deferment, an EMI pause or restructure, and interest rate negotiation on credit cards.

I know — it feels uncomfortable. Do it anyway. Companies and landlords would far rather restructure a payment than deal with a default. In the UK, most mortgage lenders have a formal “payment holiday” process. In India, banks have EMI moratorium options. In the US, credit card hardship programmes are far more accessible than most people realise. One phone call can reduce your monthly outflow by ₹15,000–₹30,000 or $200–$500.

Build a Minimum Income Stream — You Don’t Need a Full Salary Yet

You don’t need to replace your income in week two. You just need to slow the burn. Even partial income changes the math dramatically.

Options that work quickly:

- Freelancing your existing skill set — a product manager, data analyst, or marketing lead can earn ₹40,000–₹80,000 or $800–$2,000/month from two or three short contracts

- Short-term consulting gigs — former employers are often the fastest route; they know your work

- Contract or interim roles — many companies hire on a day-rate basis during hiring freezes

Adding even 20–30% of your previous income while cutting expenses by 25% can extend your runway by 50% or more. That’s not a small advantage — it’s the difference between a panicked three-month search and a strategic six-month one.

Prioritise High-Probability Job Leads, Not Volume

This is the phase where people waste enormous energy sending 50 cold applications into an ATS void. Stop. Focus your job search energy on referrals, former colleagues, and your immediate professional network. Research consistently shows that 60–70% of roles are filled through networking before they’re ever posted. Volume doesn’t win this game — relevance does.

Day 31–60: Extend Your Runway Strategically

This is the phase that separates people who recover well from those who spiral. The first month’s panic has faded. Now you need clear-eyed strategic thinking — which is exactly when ego tends to show up and cause problems.

Reassess Your Financial Position With Real Numbers

By day 30, you have real data. Run the numbers again:

- Actual burn rate (what you’re actually spending, not what you planned)

- Actual income inflow (freelance, unemployment, severance)

- Remaining savings

Recalculate runway. If it’s still under three months, you need aggressive action in this phase — not modest tweaks.

Make the Strategic Trade-offs Ego Won’t Let You Make

Here’s where I’ve watched smart, capable people make costly mistakes: they refuse trade-offs that feel like admissions of failure. They’re not. They’re runway multipliers.

- Temporarily moving to a cheaper location — even for 2–3 months, this can extend runway by 30–40%

- Moving in with family — removing rent entirely is the single biggest runway lever available to most people

- Selling underused assets — a second vehicle, high-end equipment, or furniture you won’t miss

None of these are permanent. All of them buy time. And time is the asset that translates directly into a better next job.

Shift From “Any Job” to “Right Job With Acceptable Timeline”

By day 45, if your runway is healthy, resist the temptation to accept the first offer that arrives. You’re balancing three things: salary (which should be at or above your previous band), stability (avoid companies with recent funding issues or obvious cultural red flags), and growth (does this role move you forward, or sideways?). A wrong hire after a layoff often leads to a second job search within 12 months — and that’s a much harder story to tell in interviews.

Day 61–90: Transition to Recovery Mode

By now, one of three things is true: you have a job offer, you’re close to one, or you’re still searching. Each requires a different play.

If You Have an Offer

Don’t rush the signature. Evaluate the company’s financial stability (particularly important in early-stage or recently funded companies), role alignment with your career trajectory, and real growth potential. A bad job after a layoff isn’t just inconvenient — it’s a second financial and career crisis compressed into 6–12 months. Take two days. Think clearly.

If You’re Close to an Offer

Double down on execution: rigorous interview preparation, timely follow-ups within 24 hours of each round, and early groundwork on salary negotiation. This is the stage where many candidates lose offers not from lack of qualification but from poor follow-through. A thank-you note, a specific follow-up, a well-timed check-in — these details matter more than people admit.

If You’re Still Searching

Now is the time to pivot deliberately. Expand your role criteria — adjacent titles, smaller companies, different industries that use your skills. Consider contract or interim work as a bridge. The goal shifts from “ideal role” to “sustainable income that extends financial stability while the right role emerges.” This isn’t settling. It’s strategic sequencing.

Real Scenario: Two Layoff Outcomes — Same Salary, Different Decisions

I worked with two professionals in 2024, both senior managers earning similar salaries in tech. Both received layoff notices in the same month. Here’s what happened:

Person A

- Kept existing spending habits for 6 weeks (“I’ll be employed soon”)

- Applied broadly and randomly — 80+ applications, minimal network activation

- Didn’t negotiate expenses or seek partial income

- Ran out of runway at month 3

Accepted a role 18% below previous salary under financial pressure

Person B

- Cut to bare-minimum budget in week 1

- Took two short-term consulting contracts (approx. 40% of prior income)

- Renegotiated lease — saved ₹18,000/month

- Extended runway to 7 months

Landed a role with a 28% salary increase — on their terms, on their timeline

Same starting point. Completely different outcomes. The only variable was financial decision-making in the first 30 days.

Smart Strategy: The Runway Multiplier Framework

Here’s the framework I walk every client through. It’s not complicated — but it’s powerful because the effects compound.

Three levers. Pull all three simultaneously.

1

Reduce Burn Rate — Cut non-essentials, renegotiate fixed costs. Target: reduce monthly outflow by 25–35%.

2

Add Micro-Income — Freelance, consult, or contract. Target: replace 20–30% of prior income within 30 days.

3

Protect Savings — No new discretionary spending, no investment contributions, no large purchases. Liquidity is your lifeline.

The math: reduce expenses by 25% and add 20% income? Runway increases by over 50%. That’s the difference between a 3-month panic spiral and a 5-month strategic search. Pull all three levers at once and it compounds further.

What to Do vs. What Not to Do: A Quick Comparison

| Smart Move | Common Mistake |

|---|---|

| Calculate BMME and runway on day 1 | Assume the job search will be quick |

| File for unemployment benefits immediately | Delay filing by weeks, losing benefits |

| Freeze all non-essential subscriptions | “Reduce” spending without actually cutting |

| Renegotiate rent and loan repayments | Assume fixed costs can’t be changed |

| Start freelancing or consulting within 2 weeks | Wait for the “right” full-time job only |

| Focus job search on referrals and network | Spray 100 cold applications |

| Pause investment contributions, preserve liquidity | Keep investing while savings drain |

| Evaluate all three factors before accepting an offer | Accept the first offer out of desperation |

5 Common Mistakes That Destroy Your Finances After a Layoff

I’ve seen all of these. Repeatedly. They’re avoidable — but only if you know to watch for them.

1. Ignoring the timeline reality. “I’ll find something in a month” is a hope, not a plan. The average job search for a mid-to-senior professional in the US takes 3–5 months in normal market conditions. In a cooling market, 4–7. Plan for the realistic scenario, not the optimistic one.

2. Maintaining your previous lifestyle. This is the biggest silent killer. Every month you delay cutting expenses is a month of runway lost. Lifestyle inflation feels invisible during employment — it becomes very visible when the paychecks stop.

3. Waiting too long to take action. The most expensive decisions in a layoff are the ones that get deferred. Delaying severance negotiation, delaying the unemployment claim, delaying the expense review — all of it compounds.

4. Accepting the first offer. Financial pressure is real, but a rushed decision here can cost you far more over the next 2–3 years. A $10,000 or ₹8 LPA salary deficit from a panic hire compounds painfully. If your runway is managed well, you can afford to wait for the right offer.

5. Not leveraging your network. Cold applications are the least efficient job search strategy available. And yet, when people feel embarrassed about a layoff, that’s exactly what they lean on. The people most likely to help you get your next role already know you. Use them.

Pro Tips Most People Miss

💡 Health Insurance Strategy

In the US, COBRA lets you keep your employer plan — but it’s often expensive (you now pay the full premium). Compare it against ACA marketplace plans immediately after your layoff. A marketplace plan at a lower premium can save $200–$500/month during your search period. In India, port your employer group health cover to an individual policy within 30 days to avoid the waiting period reset.

💡 Emergency Side Hustle Mindset

This isn’t about passion projects. During a layoff, a side hustle is purely functional — it slows the cash bleed. Think in terms of your most marketable existing skill and the fastest path to payment. Fiverr, Toptal, Upwork, or a direct outreach to former colleagues asking for project work. Even ₹25,000–₹40,000 or $500–$800/month changes your financial position meaningfully.

💡 Cash Is King Right Now

Avoid locking money into illiquid investments — SIPs, term deposits, or anything you can’t access immediately. This is temporary. Once you’re re-employed, you resume. Right now, liquidity is worth more than any potential return.

💡 Track Every Expense — Awareness Is Control

Use a simple spreadsheet or an app like YNAB, Money Manager, or even a Google Sheet. When you can see your burn rate in real time, you make better decisions. Most people who “think” they’ve cut spending are still spending more than they realise.

💡 Psychological Control Is a Financial Asset

Financial stress is one of the leading causes of poor decision-making in a job search. People under stress make short-term choices — accepting lowball offers, burning bridges, or making erratic decisions — that have long-term costs. A structured plan reduces anxiety. Stay structured, even when it feels artificial.

FAQs: Surviving a Layoff Financially

How long should my savings last after a layoff?

Aim for a minimum of 3 months of bare-minimum expenses at the point of layoff, and work to extend it to 6–9 months through the cuts and micro-income strategies in this plan. Mid-to-senior professionals in competitive markets should plan for a 4–6 month search. Building towards 6 months gives you genuine negotiating leverage.

Should I use credit cards during unemployment?

Sparingly and with a clear plan. Credit cards are a last resort for genuine essentials — food, utilities, critical bills — not a lifestyle buffer. High-interest revolving debt during a job search compounds your financial pressure significantly. If you must use credit, treat every charge as a loan you’ll repay from your first post-layoff paycheck.

Is it okay to take a lower-paying job after a layoff?

Yes — if it extends your runway, reduces financial pressure, and keeps you in the workforce. A bridge role at 80% of your previous salary is often better than a 6-month gap, both financially and for your next interview narrative. The key is treating it as a strategic move, not a surrender. Negotiate an exit clause or timeline review upfront.

Should I pause investment contributions after a layoff?

In most cases, yes. Pause SIPs, 401k contributions above any employer match (if still applicable), and any non-liquid investments. Redirect that cash to your liquid runway. The short-term opportunity cost is far outweighed by the financial resilience you gain. Resume contributions once you have three months of new employment confirmed.

How quickly should I start job hunting after a layoff?

Immediately — but not chaotically. Start your financial stabilisation (days 0–7) in parallel with your job search, not sequentially. The first week should include both: securing your cash position and activating your professional network. The job search itself should be strategic rather than volume-driven from day one.

What’s the single biggest financial mistake after a layoff?

Not cutting expenses fast enough. Every week of delayed action at your previous lifestyle costs you significant runway. Professionals who act on expenses in the first week extend their search capacity by months. Those who wait until month two or three often find themselves in a financial corner — and that’s when bad decisions happen.

Can freelancing fully replace a full-time salary during a layoff?

Sometimes — but treat it as a bridge, not a guarantee. Freelancing works best as a runway extender, not a full income replacement during an active job search. The exception is if you have strong existing client relationships or a specialist skill with high market demand. In that case, a full contract pivot may actually be strategically better than a rushed permanent hire.

A Layoff Is a Financial Test — and You Can Pass It

I’ll be direct: the professionals who survive a layoff financially and come out stronger aren’t the ones with the most impressive CVs. They’re the ones who manage the first 90 days with clarity and discipline.

Your goal isn’t just survival. It’s to buy time. Time gives you options. Options give you negotiating power. And negotiating power is what turns a layoff into a genuine career inflection point — the kind where you land a better role, on better terms, than the one you left.

Run the framework: reduce burn rate, add micro-income, protect your runway. Do it in week one, not week four. Make the trade-offs ego resists. And approach the job search strategically, not desperately.

If your severance package hasn’t been finalised yet, that’s actually one of the most important moves to get right before any of this — read our guide on how to negotiate your severance package to make sure you’re starting this 90-day plan with the strongest possible financial foundation.

Michael Reeves

Employment & Severance Advisor — Former Senior Counsel at Littler Mendelson | 18+ years advising Fortune 500 restructurings | Chicago & London

Updated: April 2026 | Category: Layoffs & Severance | 8 min read

Michael Reeves | Former Senior Counsel, Littler Mendelson | Severance & Restructuring Specialist | 18+ Years in Employment Law

Author bio: Michael Reeves spent nearly two decades as Senior Counsel at Littler Mendelson — one of the world’s largest employment law firms — advising on mass layoffs, corporate restructurings, and severance negotiations for Fortune 500 companies across the US and Europe. He has worked both sides of the table: structuring cost-efficient separation packages for employers and, more recently, helping employees understand exactly where their leverage lies. Based between Chicago and London, Michael writes for HRGet.com to demystify the legal and financial dimensions of layoffs — so employees stop leaving money on the table.