Most professionals tick “disability insurance” during their onboarding paperwork and never think about it again. It’s right there in your benefits package, it sounds comprehensive, and your employer is paying for at least part of it. What’s not to like?

Here’s the problem: disability insurance through your employer was never designed to fully replace your income. It was designed to keep you from complete financial collapse while you recover. That’s a meaningful difference — and one that can cost you tens of thousands of dollars if you don’t understand it before you need it.

I’ve spent 14 years working in HR and employee benefits, and the most common financial blindspot I see among professionals aged 28–45 isn’t a bad investment or a missed salary negotiation. It’s a misplaced assumption that their employer’s group disability plan “has them covered.” This guide will show you exactly where that assumption breaks down — and what to do about it.

What Is Employer Disability Insurance?

Employer disability insurance is a group benefit that partially replaces your income if you become unable to work due to illness, injury, or a qualifying medical condition. It’s one of the most commonly offered — and least understood — components of a total compensation package.

Most employers offer it in one of two ways: a basic plan that’s fully employer-paid at no cost to you, or a contributory plan where the company covers a base level and you can buy up additional coverage at a group rate. Either way, it typically shows up quietly in your benefits summary without much fanfare.

The underlying structure is a group policy. Your employer buys it in bulk for the workforce, which keeps premiums low — but also means the policy is standardized, not tailored to your income, lifestyle, or financial obligations. That distinction matters enormously when you actually need to use it.

💼 Insider View:

In my experience reviewing benefits packages across mid-size and enterprise employers, the language around disability coverage tends to be deliberately vague. Plans often lead with headline numbers like “60% income replacement” — but the fine print on benefit caps, elimination periods, and definition of disability tells a very different story. Most employees never read that fine print until they’re filing a claim.

Short-Term vs. Long-Term Disability: Key Differences

These two types of coverage serve different purposes, and understanding that distinction is critical before you evaluate whether what you have is adequate.

Short-Term Disability (STD)

Short-term disability bridges the gap between the onset of a health condition and your return to work — or the point at which long-term disability kicks in. Typical parameters: it replaces 60–70% of your base salary, has an elimination period of 7–14 days (meaning you must be disabled for that long before benefits begin), and covers you for 3–6 months. Common triggers include surgery recovery, a difficult pregnancy, or a temporary injury.

Long-Term Disability (LTD)

Long-term disability is the coverage that matters for serious, extended conditions — think a cardiac event at 38, a cancer diagnosis, a degenerative musculoskeletal condition, or a severe mental health episode. LTD typically begins after your STD coverage ends and replaces 50–60% of your pre-disability earnings, often capped at a monthly dollar maximum. Duration varies: some plans cover two years, others run to age 65.

The gap most people don’t anticipate is the handoff period — the weeks between when STD ends and LTD begins processing. That’s usually where the financial stress hits hardest, and where having liquid savings makes an outsized difference.

⚠️ Warning:

Many professionals assume their employer’s short-term and long-term disability plans are seamlessly linked. In practice, LTD applications often require separate paperwork and a new approval process. Delays of 4–8 weeks are not uncommon. Without a savings buffer of 3–6 months of expenses, this gap can force people into debt or early retirement account withdrawals.

How Much Do You Actually Receive? (The Real Numbers)

This is where most explanations of employer disability insurance gloss over the uncomfortable details. Let’s be specific.

Take a software engineer in Austin earning $120,000 a year — a reasonable benchmark for a mid-level professional in a major US metro. Their employer offers a standard LTD plan that replaces 60% of pre-disability income. On paper, that’s $72,000 a year, or $6,000 a month. Sounds workable, right?

📊 The Real Income Calculation — $120K Salary, 60% LTD Plan

That’s a 59% drop in real spending power from $120K down to roughly $49K — all while your rent, mortgage, car payment, and student loan obligations stay exactly the same.

Now add a monthly benefit cap. Many group LTD plans cap payouts at $8,000–$10,000 per month regardless of your actual salary. For anyone earning above $160,000–$200,000, the cap kicks in immediately, meaning your effective income replacement rate is far below 60% from day one.

This isn’t a flaw in the system — it’s a feature. Group policies are priced for the average worker. If you’re above average in earnings, the average policy wasn’t built for your situation.

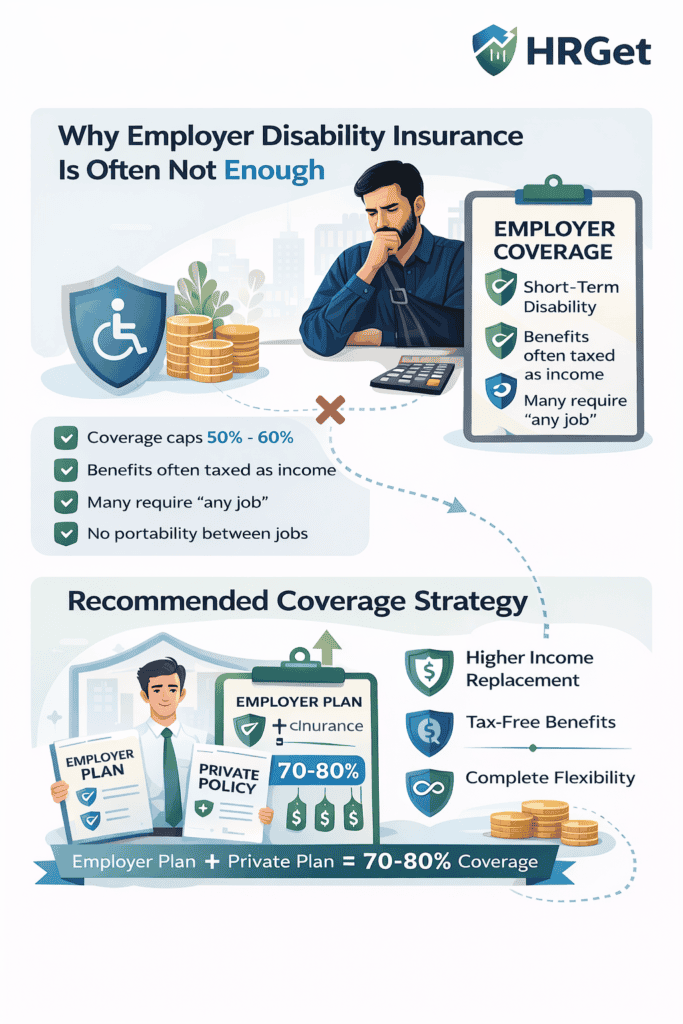

Why Employer Disability Coverage Usually Falls Short

I want to be direct here: employer-provided disability insurance is not a bad benefit. It’s a genuinely useful foundation. The problem is when professionals treat it as a complete solution rather than a baseline — and that’s an easy mistake to make when no one explains the gaps at onboarding.

1. The “Any Occupation” Definition Is the Biggest Trap

This is the clause most employees never read, and it’s the one that derails the most claims. Many group LTD policies define disability as the inability to perform any occupation for which you are reasonably qualified — not your specific occupation. A surgeon who loses the dexterity to operate but can still teach or consult may find their claim denied. A software engineer with severe carpal tunnel who can theoretically do administrative work might get zero payout. “Own occupation” policies, which pay if you can’t do your current job specifically, are far more protective — and far less common in standard group plans.

2. Benefits Are Taxable When the Employer Pays the Premium

The IRS rule here is straightforward but often unknown: if your employer pays the disability insurance premium (which most do), the benefit payments you receive are subject to federal and state income tax. That 60% replacement rate shrinks to somewhere between 42% and 48% of your original gross income after taxes, depending on your bracket and state. If you pay the premium yourself through after-tax payroll deductions, benefits are generally tax-free — a significant planning distinction.

3. Coverage Doesn’t Travel With You

Group disability coverage is tied to your employment. If you leave the company — voluntarily, through a layoff, or even during a medical leave that stretches beyond FMLA’s 12-week protection — you typically lose your LTD coverage. This creates a dangerous exposure gap during job transitions, which happen to be exactly the times when many professionals are taking on new financial obligations or are between insurance continuity options.

4. Mental Health and Chronic Conditions Are Often Limited or Excluded

This is increasingly relevant in 2026. Many group LTD plans cap mental health disability claims at 24 months, regardless of whether the condition is fully disabling. Conditions like severe depression, PTSD, anxiety disorders, and burnout-related disorders — which account for a growing proportion of disability claims among professionals under 45 — frequently hit this wall. Chronic conditions like long-COVID complications and fibromyalgia also face heightened scrutiny from group plan administrators.

5. The Elimination Period Creates an Immediate Cash Crisis

Most LTD plans have an elimination period of 90 to 180 days. That means you’re on your own — relying on STD, sick leave, and personal savings — for up to six months before LTD benefits begin. For a household carrying a mortgage, car payments, and childcare costs, six months without full income isn’t a speed bump. It’s a financial emergency.

Real Scenario: Where It Goes Wrong

📁 Real Scenario:

Marcus, 36, Senior Product Manager — fintech company, Chicago

Marcus earns $145,000 a year. His employer provides a standard LTD plan: 60% income replacement, capped at $8,500/month, with a 90-day elimination period and an “any occupation” disability definition. He also carries a mortgage of $3,200/month, a car loan, and contributes $2,000/month to his daughter’s education fund.

At 36, he’s diagnosed with relapsing-remitting multiple sclerosis. After three months on STD (which depletes his PTO and short-term savings), his LTD claim is initially approved. His benefit: $8,500/month gross, taxed as ordinary income. After federal and Illinois state tax, he nets roughly $6,100/month — against fixed monthly obligations of $6,800.

Two years in, his condition stabilizes enough that he can perform basic cognitive tasks, though not at the pace his product management role demands. The insurer argues he qualifies for sedentary work and terminates his LTD benefit. He’s now earning nothing, with no private supplemental coverage and a legal appeals process ahead of him.

The gap that hurt him most wasn’t the diagnosis — it was the policy definition and the benefit cap he’d never examined.

Employer vs. Private Disability Insurance: An Honest Comparison

| Feature | Employer Group Plan | Private / Individual Policy |

|---|---|---|

| Cost to you | Low or free (employer-funded) | Higher monthly premium (you pay) |

| Income replacement rate | 50–60% (before tax) | 60–80% (often tax-free) |

| Monthly benefit cap | Usually $8K–$12K | Customizable to income level |

| Disability definition | Often “any occupation” | “Own occupation” available |

| Portability | ✗ Lost when you leave employer | ✓ Follows you across jobs |

| Tax treatment of benefits | Taxable (employer-paid premium) | Tax-free (you pay premium) |

| Mental health coverage | Often capped at 24 months | Can be unlimited with riders |

| Underwriting | Guaranteed issue (no medical exam) | Medically underwritten (cleaner health = lower premium) |

| Inflation protection | Rarely included | Available via COLA rider |

| Best for | Baseline protection & lower earners | High earners, specialized roles, long-term security |

The smart play isn’t to replace your employer plan — it’s to stack them. Your group plan costs you nothing and provides a base layer. A private policy, purchased while you’re young and healthy, sits on top and fills the gap. Together, they can get you to 75–80% of your actual take-home income — which is the real target number.

💡 Pro Tip:

Buy individual disability insurance while you’re under 35 and in good health. Premiums are dramatically cheaper — often 30–40% lower than if you wait until your mid-40s. A 32-year-old non-smoker in a professional occupation can typically lock in own-occupation LTD coverage for $150–$250/month that would cost $400+ at 45. Once issued, the policy can’t be cancelled and premiums can’t be raised if you choose a non-cancelable, guaranteed-renewable contract. That’s the version worth buying.

How Much Disability Coverage Do You Actually Need?

The industry benchmark is 70–80% of your gross income protected. But I’d frame it differently: you need enough coverage to keep every non-negotiable financial obligation paid, plus a modest buffer, for the duration of your potential disability. Let’s make that concrete.

Start With Your Fixed Monthly Obligations

Add up your mortgage or rent, car payment, minimum debt service, insurance premiums, and childcare or school fees. This number doesn’t change just because you’re ill. Call it your “floor.” Your disability coverage should exceed this number after tax.

Then Factor In Medical Costs

If you’re on disability, you’re almost certainly spending more on healthcare — specialist visits, medications, physical therapy, or home care. Budget an additional $500–$1,500/month above your normal medical spend, depending on the condition.

Apply the Coverage Framework

- Minimum viable: 60% gross income — survival-level. Covers basics, nothing else.

- Comfortable stability: 70–75% gross income — recommended for most professionals with fixed obligations and dependents.

- Full lifestyle protection: 80% gross income — appropriate for high earners or single-income households where a disability would be financially catastrophic.

If your employer’s plan gets you to 60% pre-tax (which is really 42–50% post-tax), you’re most of the way to “minimum viable” before you account for caps. You are not at “comfortable stability.” That gap is exactly what a private supplemental policy is designed to close.

Common Mistakes That Leave Professionals Exposed

These aren’t abstract risks. I’ve watched each of these play out — often with people who thought they had solid coverage.

Mistake 1: Assuming “I’m Covered” Without Reading the Policy

Most employees couldn’t tell you the elimination period, benefit cap, or disability definition in their own LTD plan. Spend 20 minutes with your Summary Plan Description (SPD) — your HR team is required to provide it on request. The three things to look for: elimination period, monthly benefit maximum, and whether the definition is “own occupation” or “any occupation.”

Mistake 2: Ignoring the Tax Math

The difference between a 60% pre-tax benefit and a 60% post-tax benefit is enormous over a multi-year disability. Don’t evaluate your coverage at the headline percentage — evaluate it at the net-of-tax dollar amount. That’s the number that actually pays your bills.

Mistake 3: Waiting Until You’re Older (or Sick) to Buy Private Coverage

Once you have a diagnosed condition, you’ll either be declined for individual coverage or rated up significantly. The window to buy portable, own-occupation coverage at the best rates is when you’re healthy and don’t need it yet. That sounds counterintuitive, but it’s how insurance math works.

Mistake 4: Not Accounting for Career Transitions

Layoffs, voluntary job changes, and entrepreneurial pivots all sever your group coverage. If you’re planning a career move — especially one that includes a gap period — securing private coverage before that transition protects you during the period when you’re most exposed and least likely to qualify for a new group plan immediately.

Mistake 5: Overlooking Mental Health and Chronic Illness Clauses

Burnout, anxiety disorders, and chronic pain conditions — the most common causes of disability among professionals under 50 — frequently hit policy exclusions or caps first. Read the mental health and “self-reported symptom” clauses specifically. If yours is limited to 24 months for mental health, that’s a meaningful gap for conditions that routinely last longer.

💼 Insider View:

One pattern I’ve noticed consistently: the professionals who end up in the worst financial situations aren’t the ones with the worst health outcomes. They’re the ones with the best incomes and the most assumptions. A $200K-a-year director assumes their benefits are proportionally generous. They rarely are. The group plan was built for the median employee. At the higher end of the income distribution, you’re quietly self-insuring the gap — you just don’t know it yet.

Is disability insurance through your employer enough? For most professionals — no. Not if you have fixed financial obligations, dependents, a specialized career, or earn above $80,000 a year.

It’s a genuinely valuable foundation: it costs you nothing, provides guaranteed coverage without medical underwriting, and pays benefits during legitimate short-term and long-term health events. But it was never designed to be your entire safety net.

The professionals who navigate a serious disability without financial catastrophe are almost always the ones who had a private policy stacked on top — bought early, structured correctly, and reviewed annually alongside their salary growth.

Frequently Asked Questions About Employer Disability Insurance

Still figuring out your total compensation picture? Disability insurance is just one piece of the financial protection puzzle. If you’ve recently navigated a layoff or are evaluating a new job offer, understanding your full benefits package — including severance entitlements — can make a meaningful difference to your financial security. Read our guide on how to negotiate severance pay for the strategies that most employees don’t know they can use.

Emily Carter is a career coach and former McKinsey talent advisor with 15+ years of experience helping professionals navigate career transitions, promotions, and high-stakes job decisions. She has advised professionals across consulting, technology, finance, and corporate leadership roles on offer negotiations, career positioning, and long-term growth strategy.

Role: Career Coach & Ex-McKinsey Talent Advisor: Focuses on helping professionals make smarter career moves—switching jobs, negotiating offers, and long-term career growth. She blends structured thinking with real-world coaching insights.