Every open enrollment season, I watch the same thing happen. Employees skim the HSA vs FSA comparison on their HR portal — both seem vaguely tax-advantaged, both involve medical spending — and they just pick whichever one they had last year. Or worse, they pick neither, because the whole thing feels confusing.

I’ve spent 20 years advising companies and executives on benefits strategy. And I’ll tell you plainly: the wrong choice between an HSA and FSA can quietly cost a mid-career professional $800 to $2,000 in annual tax savings. Over a decade? That compounds into real money.

This guide cuts through the noise. By the end, you’ll know exactly which account fits your situation — and how to use it the way high earners actually do.

What Is an HSA vs FSA? (No Jargon)

Both accounts let you set aside pre-tax money for medical expenses. That’s where the similarity ends.

An HSA (Health Savings Account) is essentially a medical investment account that you own outright. The money is yours whether you change jobs, retire, or move states. It rolls over indefinitely, it can be invested in mutual funds once your balance crosses a threshold (typically $1,000), and it comes with a triple tax advantage that’s genuinely rare in the US tax code.

An FSA (Flexible Spending Account) is a short-term tax-saving tool. Your employer technically owns the account. Most of the money has to be used within the plan year, and you can’t invest it. That said, it’s available on almost any health plan — not just high-deductible ones — which makes it accessible to a broader group of employees.

The short version: HSA is a long-term wealth tool that happens to cover medical expenses. FSA is a tax-efficient spending wallet for predictable near-term costs.

Insider View:

When I ran compensation reviews at Fortune 500 clients, we’d consistently find that fewer than 30% of employees who were HSA-eligible were actually maximizing the contribution. The ones who did — typically senior engineers, finance professionals, and anyone who’d spent time with a financial advisor — were quietly building tax-free nest eggs while their colleagues spent FSA money on last-minute December eyeglass purchases.

2026 Contribution Limits: What the IRS Is Allowing

The IRS adjusts these limits annually for inflation. For 2026, here’s the current guidance (note: official final IRS figures are typically confirmed in late 2025; the ranges below reflect projected adjustments based on the 2025 baseline and inflation trends):

HSA Limits (2026)

- Individual coverage: ~$4,300

- Family coverage: ~$8,550

- Catch-up (age 55+): +$1,000

- Minimum HDHP deductible: ~$1,650 individual / $3,300 family

FSA Limits (2026)

- Standard FSA: ~$3,300

- Carryover limit: ~$660 (if employer allows)

- Dependent care FSA: $5,000 (household)

- Grace period option: 2.5 months post plan year

The gap matters: a family that maxes an HSA vs an FSA is sheltering roughly $5,000 more in pre-tax income each year. At a 30% marginal rate, that’s $1,500 in tax savings annually — before any investment growth on the HSA balance.

Important:

Always confirm final IRS contribution limits on IRS.gov or via your benefits administrator before your enrollment deadline. The figures above reflect projected 2026 guidance; final numbers may vary slightly.

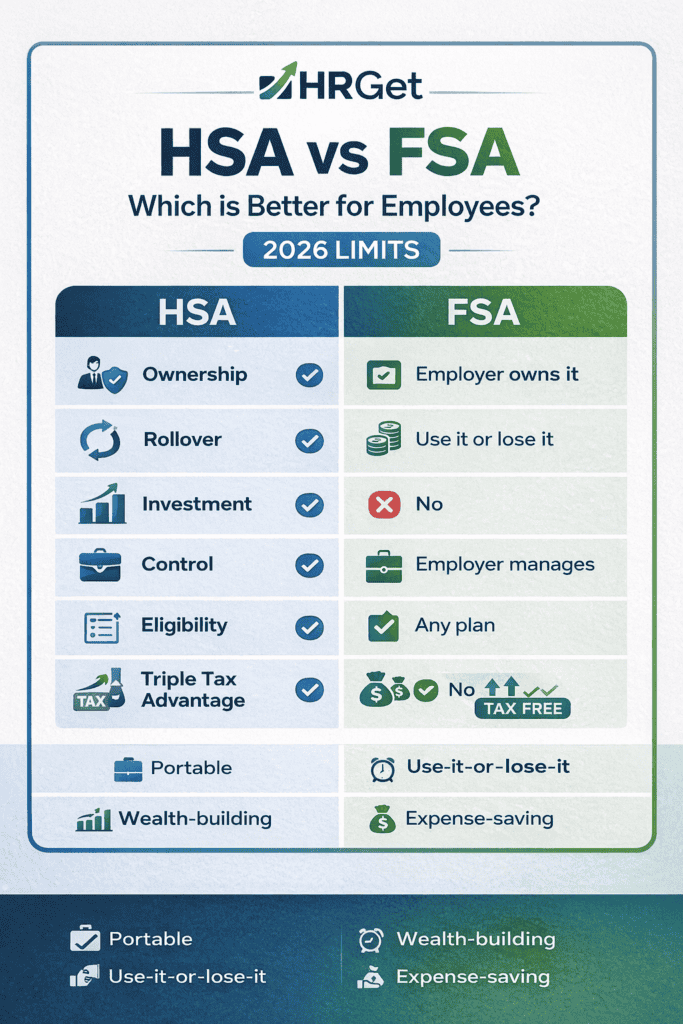

Key Differences: The Ones That Actually Matter

Here’s the full picture side by side — but I want you to focus on the last three rows. Those are the ones that determine whether you’re building wealth or just saving on next year’s tax bill.

| Feature | HSA | FSA |

|---|---|---|

| Who owns the account | You (portable) | Your employer |

| Rollover | Unlimited, forever | Limited (~$660) or lose it |

| Investment option | Yes — mutual funds, ETFs | No |

| If you change jobs | Keep it entirely | Typically forfeit unused balance |

| Plan eligibility | Requires HDHP only | Any qualified health plan |

| 2026 max contribution (family) | ~$8,550 | ~$3,300 |

| Tax structure | Triple tax advantage | Double tax advantage |

| Reimburse old expenses? | Yes — no deadline | No — current year only |

| After-65 use | Any expense (pay income tax) | Account closes at year end |

| Employer can contribute | Yes | Yes |

That row about reimbursing old expenses deserves emphasis. With an HSA, you can pay a medical bill out of pocket today, keep the receipt, and pull the reimbursement from your HSA five years from now — after the balance has grown tax-free. That’s a legal wealth-building move that almost nobody in your HR portal brochure explains.

Real Scenario: Which One Saves More Over Time?

Real Scenario:

Profile: Marcus, 34, Senior Marketing Manager, earning $92,000 in Chicago. Tax bracket: 24% federal + 5% state. Annual medical expenses: ~$1,800/year (healthy, no chronic conditions). Open enrollment choice: HDHP with HSA vs PPO with FSA.

FSA Path: Marcus contributes $1,800 to FSA. Tax savings at ~29% combined rate: $522/year. Uses all of it by December. Net benefit: $522 saved. Zero balance carried forward.

HSA Path: Marcus contributes $4,300 to HSA. Tax savings on contributions: $1,247/year. He pays his $1,800 in medical bills out of pocket, keeps receipts. HSA balance is invested at a conservative 6% annual return. After 20 years, that $4,300/year in contributions grows to approximately $167,000 — all of which can be withdrawn tax-free for medical use (or at income tax rates for any expense after 65).

Difference over 20 years: Not $522 vs $1,247. It’s $10,440 vs $167,000. The account you pick in open enrollment compounds for decades.

I’m not saying this to be dramatic. I’ve shown this math to executives who’d been FSA users for a decade and watched the realization land. The FSA isn’t bad — it’s just a different tool. Marcus’s scenario assumes he can absorb a slightly higher deductible on the HDHP. If he can’t, FSA is the right call. But if he can? The wealth gap is significant.

When HSA Is the Clear Winner

HSA wins in your situation if most of the following are true:

You’re relatively healthy with low to moderate annual medical costs. The HDHP you’d pair with an HSA has a higher deductible, but if you’re not hitting it anyway, the premium savings often offset the difference. Run the math on your specific plan options — most HR platforms show this comparison, though few employees actually use it.

You’re in a mid-to-high tax bracket. The triple tax advantage hits harder the higher your marginal rate. A $4,300 HSA contribution at a 32% combined federal/state rate saves you $1,376 upfront — and that’s before investment growth.

You change jobs more than once per decade. The portability factor is underrated. Your HSA moves with you. Your employer’s FSA does not.

You think about retirement with any seriousness. Healthcare costs in retirement are the single largest unplanned expense most Americans face. Fidelity’s research estimates the average retired couple needs over $300,000 for medical expenses in retirement. An HSA is the only account in the US tax code that is triple-tax-advantaged specifically for this purpose.

Pro Tip:

Check whether your employer contributes to the HSA. Many companies add $500–$1,500 annually — especially at larger firms offering wellness incentives. That’s free money on top of your tax savings. If your employer contributes $750 to an HSA and nothing to an FSA, that alone should move the needle in your decision.

When FSA Is the Smarter Move

FSA gets underrated because most articles frame it as the “loser” in this comparison. That’s too simple. There are real situations where FSA is the better choice — and picking HSA in those situations can actually cost you money.

You have predictable, significant medical expenses this year. If you know you’re having a planned surgery, orthodontic work, a baby, or ongoing prescription costs — FSA’s use-it-or-lose-it structure aligns perfectly. You contribute what you know you’ll spend, get the tax break, and pay nothing extra out of pocket.

You can’t afford the HDHP deductible risk. This is the honest conversation most HR materials avoid. If a $1,650 individual deductible would create genuine financial stress, don’t chase HSA benefits. A plan you can actually afford is always the right plan. Take the FSA on a lower-deductible PPO and get the partial tax benefit without the financial exposure.

You have dependents with recurring healthcare needs. Predictability is FSA’s superpower. Quarterly therapist visits, a child’s allergy medication, annual dental work — if you can forecast the spending, FSA lets you pre-fund it tax-efficiently with no investment friction.

And don’t overlook Dependent Care FSAs — these are separate accounts that cover childcare, after-school programs, and elder care costs. They have nothing to do with your health insurance choice and are worth maxing for almost every working parent.

Smart Strategy: How High Earners Actually Use Their HSA

The employees who get maximum value from HSAs don’t use them the way the brochure describes. Here’s what the financially sophisticated actually do:

Strategy 1: Contribute the max, touch nothing

Max the HSA contribution every year ($4,300 individual or $8,550 family in 2026). Pay all medical bills out of pocket. Keep every receipt — digitally scan and store them. Let the HSA balance accumulate and compound. This works if your cash flow can absorb out-of-pocket medical costs without stress.

Strategy 2: Reimburse yourself years later

Here’s the tax hack almost nobody talks about: the IRS sets no deadline on HSA reimbursements. You can pay a $400 dental bill today, let that $400 sit invested in your HSA for 10 years, and then reimburse yourself $400 (plus whatever it grew into). The reimbursement is tax-free. Your original $400 grew tax-free. This is one of the most powerful legal tax-deferral strategies available to W-2 employees.

Strategy 3: The Limited Purpose FSA combo

Some employers offer a “Limited Purpose FSA” — a dental and vision-only FSA that’s compatible with an HSA. If yours does, this is the optimal setup: fund the Limited FSA for planned dental and vision expenses, keep the HSA for everything else, and invest the HSA balance aggressively. You’re effectively running two pre-tax accounts simultaneously.

Insider View:

When I was advising a large tech company on their benefits redesign, we introduced the Limited Purpose FSA specifically because we kept seeing employees leave HSA money on the table because they were spending it on Lasik and orthodontics. Separating the accounts — dental/vision to FSA, everything else to HSA — let employees actually build the HSA balance they intended to build. Ask your HR team if this option exists in your plan.

Common Mistakes That Cost Employees Real Money

Treating the HSA like a second FSA. This is the most common error I see. Employees contribute to the HSA, then spend it down immediately on copays and prescriptions. That eliminates the compounding advantage entirely. If you’re going to use HSA like a spending account, you’d often be better off in an FSA.

Overfunding the FSA without a realistic spending plan. Every December, someone at your company is panic-buying blue light glasses, massage cushions, and first aid kits because they over-contributed to their FSA and the grace period is ending. This is money you earned going toward purchases you don’t need. Contribute only what you can reasonably forecast spending.

Ignoring the employer HSA contribution. Employers who seed the HSA with $500–$1,500 a year are offering you free compensation. I’ve seen employees on the wrong health plan — a PPO with an FSA — when their employer was contributing $1,000 to HSAs on the other plan. Check your plan documents before enrollment closes.

Not investing the HSA balance. Most HSA providers (Fidelity, HealthEquity, Optum Bank) allow you to invest your balance once it exceeds $1,000. A surprising number of employees leave tens of thousands sitting in cash for years. Check your provider’s investment menu and set up automatic investment at the threshold.

Assuming HDHP always costs more. Run the actual numbers during enrollment. For healthy employees, the HDHP premium savings often exceed the additional deductible exposure — before you account for HSA tax savings. The PPO can be the more expensive choice when you add everything up.

Common Mistake:

If you leave a job mid-year after your employer has contributed to your FSA and you’ve already spent down the full election, you generally don’t owe the employer back — a quirk called the “uniform coverage rule.” But if you’ve only used part of your FSA contributions, you forfeit the unused portion. Understand your FSA terms before timing a job change.

The HSA vs FSA Decision Framework

Work through these four questions in order. The answer usually becomes obvious by question three.

If you have a chronic condition, young children with frequent healthcare needs, or ongoing prescriptions, the HDHP’s higher deductible may cost you more than the tax savings recoup. If you’re healthy and the HDHP deductible feels manageable, proceed to step 2.

Planned surgery, orthodontics, fertility treatment, ongoing physical therapy — if your out-of-pocket costs are large and predictable, FSA’s immediate full-election access may be more valuable than HSA’s investment potential. If expenses are modest or uncertain, the HSA is likely better.

If you already max your 401(k) and are looking for additional tax-advantaged vehicles, HSA is the obvious next step — it’s often called the “stealth IRA” by financial planners. If you’re still working on cash flow and immediate tax relief, FSA’s simplicity has real value.

If a job change is plausible, the HSA’s portability is significant. You keep the account, the balance, and the investment growth regardless of what happens next. FSA users in volatile employment situations often forfeit balances. HSA users never do.

The shortcut: if you answered “healthy, unpredictable costs, investing-focused, possibly changing jobs” — that’s an HSA. If you answered “higher healthcare needs, predictable costs, cash flow sensitive, stable employer” — that’s an FSA. Both are legitimate answers; neither is wrong.

Frequently Asked Questions

Can I have both an HSA and FSA at the same time?

Generally no — you can’t hold a standard FSA and an HSA simultaneously. The exception is a Limited Purpose FSA, which covers only dental and vision expenses and is fully compatible with an HSA. If your employer offers this option, it’s the most efficient setup: use the FSA for predictable dental and vision costs, and let the HSA compound for everything else.

What happens to my FSA if I quit or get laid off?

Your FSA typically ends at separation. You have until your termination date (or a short run-out period, usually 30–90 days depending on your plan) to submit claims for expenses incurred before you left. Any unspent balance is forfeited — it goes back to your employer. This is one of the most significant practical differences from an HSA, which you keep permanently regardless of employment status.

Is HSA better than FSA for young, healthy employees?

Usually yes, and significantly so. Young, healthy employees are the ideal HSA candidates — they have low medical costs (meaning the HDHP deductible risk is manageable), high investment time horizons, and decades for compounding to work. A 28-year-old who maxes an HSA and invests the balance annually can accumulate $200,000+ in tax-free healthcare savings by retirement with conservative return assumptions.

Can I use my HSA to pay for a spouse or child’s medical expenses?

Yes. HSA funds can be used tax-free for qualified medical expenses of your spouse and dependents, even if they’re not enrolled in your health plan. This includes children up to age 26 under the ACA dependent rules. You cannot, however, use HSA funds for a domestic partner’s expenses unless they qualify as a tax dependent.

What can HSA money be used for after age 65?

After 65, your HSA functions like a traditional IRA for non-medical expenses — you can withdraw for any purpose and pay ordinary income tax, but no penalty. For qualified medical expenses (including Medicare premiums, dental, vision, and long-term care insurance premiums), withdrawals remain completely tax-free. This flexibility is why financial planners increasingly recommend HSA-as-retirement-account strategies for high earners.

How do I start investing my HSA balance?

Log into your HSA provider’s portal (common providers include Fidelity HSA, HealthEquity, Optum Bank, and Lively). Most platforms allow investment once your cash balance exceeds $1,000. You’ll typically choose from a menu of index funds or mutual funds — low-cost index funds tracking the S&P 500 are a common choice. Set up auto-invest if available so new contributions sweep into investments automatically above the threshold.

Is an FSA worth it if my employer doesn’t offer an HSA-eligible plan?

Absolutely. If an HDHP isn’t available or isn’t right for your situation, FSA is still a meaningful tax benefit. At a 25% combined marginal rate, a $2,500 FSA contribution saves you $625 on expenses you’d pay anyway. It’s not a wealth-building tool, but it’s a legitimate way to reduce taxable income on predictable medical, dental, and vision costs.

The Bottom Line on HSA vs FSA in 2026

If you take nothing else from this: HSA and FSA are not interchangeable accounts with a minor feature difference. They’re tools for fundamentally different financial strategies.

HSA is a long-term wealth instrument that happens to cover medical costs. FSA is a tax-efficient spending account for near-term predictable expenses. Both are legitimate — but most employees who are HSA-eligible and relatively healthy should be in the HSA, maxing the contribution, investing the balance, and paying current medical costs out of pocket while their HSA compounds.

The HSA vs FSA decision looks minor during open enrollment. Across 20 years, it’s anything but. Run your numbers, check your employer’s contribution, and choose the account that matches your actual financial situation — not just the one you had last year.

Understand Your Full Compensation Package

Benefits like HSA and FSA are just one component. See how total compensation — salary, equity, benefits, and bonuses — should factor into your next job offer evaluation.

Eleanor Whitmore | Former Partner, Mercer | Advisor, World Economic Forum | 20+ Years in Global Compensation

Author bio: Eleanor Whitmore has spent over two decades shaping how the world’s leading organisations pay, retain, and reward talent. As a former Partner at Mercer and an advisor to World Economic Forum working groups on the Future of Work, she has designed compensation frameworks for Fortune 500 companies across the US, UK, Europe, and emerging markets. Based between London and New York, Eleanor writes for HRGet.com to translate boardroom-level pay strategy into actionable guidance for working professionals navigating real compensation decisions.