If you just got laid off and you’re holding a severance offer, the first question that hits most people isn’t “is this fair?” — it’s “does severance affect unemployment, and am I about to lose my benefits?” That fear is completely valid, and the frustrating part is that most generic articles give you a half-answer and leave you guessing.

Here’s the short version: severance can reduce or delay your unemployment benefits — but whether it does depends almost entirely on two things: how your severance is structured and which state you’re in. Get those two factors right, and you can often collect both. Get them wrong, and you may lose weeks of benefits you’d otherwise be entitled to.

I’ve spent 15+ years on the HR side of these conversations — watching smart professionals accept the wrong severance structure because nobody explained the mechanics. This guide fixes that. By the time you finish reading, you’ll know exactly what questions to ask before you sign anything.

What Actually Counts as Severance?

Severance is any compensation your employer pays you because your employment ended — not for work you’re actively performing. That’s the key legal distinction, and it matters more than most people realize when you’re dealing with unemployment agencies.

In practice, a severance package can include several components, and they’re not all treated the same way:

- Lump sum cash payment — a one-time payout, often calculated as X weeks per year of service

- Salary continuation — your regular paycheck keeps coming for a set number of weeks after your last day

- Accrued PTO payout — payment for unused vacation or sick days

- COBRA subsidy — employer contribution to continue your health insurance

- Outplacement services — career coaching or job search support (rarely affects unemployment)

- Signing bonus clawback waiver — sometimes included in larger packages

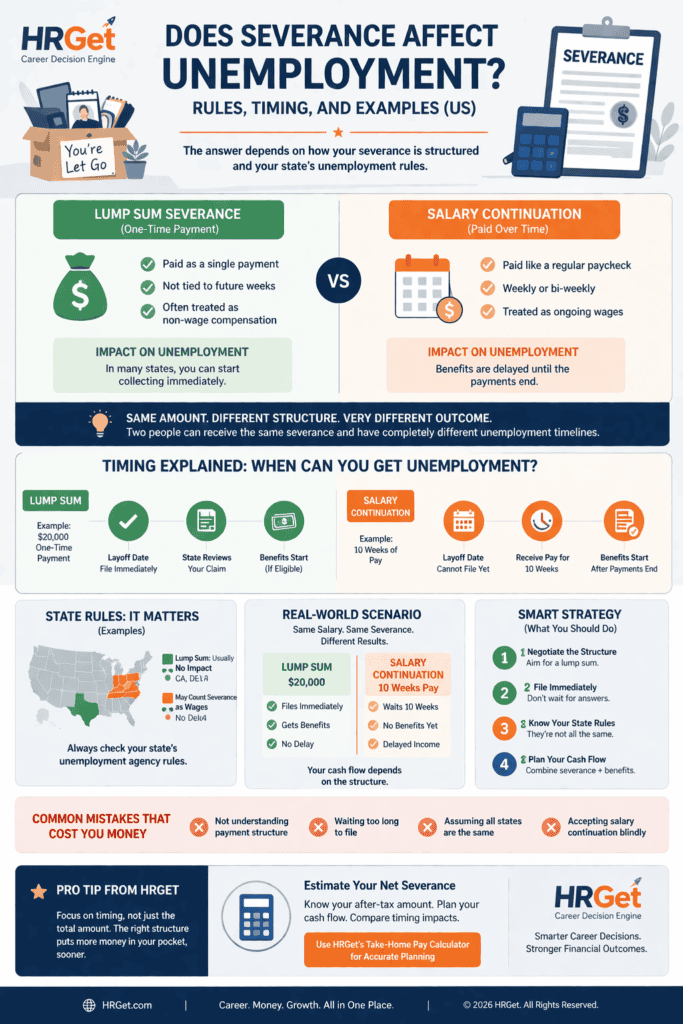

Here’s what surprises most people: two employees at the same company, both laid off on the same day, can receive the exact same dollar amount in severance — and one gets unemployment immediately while the other waits 10 weeks. The difference isn’t the amount. It’s the structure.

Unemployment agencies don’t just look at how much you received — they look at how it’s classified. Payments tied to a specific time period (like weekly salary continuation) are treated very differently from a one-time separation payment.

Does Severance Affect Unemployment Benefits?

Let’s answer this directly, because you deserve a straight answer before the nuance: severance can affect unemployment benefits, but it doesn’t automatically disqualify you or permanently reduce your payments. The most common impact is a delay — not a cancellation.

The key mechanism most state unemployment agencies use is called the “allocated period” or “severance period.” If your severance is treated as wages covering a future time period, the state considers you “employed” (or at least compensated) for those weeks — and you can’t claim unemployment until that period ends.

If your severance isn’t tied to any future period — say, it’s a clean one-time payment recognizing your years of service — most states don’t count it as ongoing wages, and your unemployment eligibility starts immediately.

| Severance Type | Typically Treated As | Impact on Unemployment |

|---|---|---|

| Lump sum (service-based) | Separation payment | Often no delay |

| Salary continuation | Ongoing wages | Usually delays benefits |

| Accrued PTO payout | Earned wages | May delay benefits |

| COBRA subsidy | Benefits (non-wage) | Rarely affects eligibility |

| Outplacement services | In-kind benefit | No impact |

The bottom line: your severance affects unemployment primarily through timing, not through permanent disqualification. Once the severance period ends, you can typically claim full benefits — assuming you meet your state’s other eligibility requirements.

Lump Sum vs Salary Continuation: The Critical Difference

I’ll be honest — this is the section that most people skip over, and it’s the one that costs them the most money. So let’s slow down here.

Lump Sum Severance: The Better Structure

A lump sum is a single payment made on or shortly after your last day. It’s not tied to any future weeks of “employment.” In the eyes of most state unemployment agencies, it’s a one-time recognition of your service — not an ongoing wage replacing your paycheck.

In states like California, Texas, and New York, a true lump sum severance generally does not delay your unemployment eligibility. You can file your claim the week after your termination date and start receiving benefits during the waiting period your state requires (typically one week).

Financially, this is the best structure for a laid-off employee. You get a lump sum and your unemployment benefits run concurrently — maximizing total cash flow during your job search.

Salary Continuation: The Hidden Delay Trap

Salary continuation feels like the same deal — sometimes it’s even for the same total amount. But instead of paying you upfront, your employer continues running payroll on a normal schedule: bi-weekly checks, same deductions, sometimes even continued benefits.

The problem? Most state unemployment agencies look at salary continuation and say: “This person is still receiving wages. They’re not unemployed yet.” Your benefit period doesn’t start until the last salary continuation check clears.

If you’re receiving 12 weeks of salary continuation on a $90,000/year salary, that’s $20,769 in gross payments — but you’re potentially forfeiting 12 weeks of unemployment benefits you would have received simultaneously under a lump sum structure. At a typical state benefit of ~$500/week, that’s $6,000 in lost unemployment payments.

Some employers default to salary continuation because it’s administratively simpler for their HR and payroll teams — not because it’s better for you. If you don’t ask for a lump sum, you probably won’t get one.

State Rules: Why Your Location Changes Everything

Unemployment insurance in the US is a federal-state partnership. The federal government sets the framework; each state administers its own program and writes its own rules about how severance interacts with benefits. This is why generic advice fails — what’s true in California may be completely wrong for Ohio.

There are three broad categories of states:

| State / Category | How Lump Sum Is Treated | How Salary Continuation Is Treated | General Stance |

|---|---|---|---|

| California | Not counted as wages | Allocated; delays benefits | Employee-Friendly |

| Texas | Generally not allocated | Allocated; delays benefits | Employee-Friendly |

| New York | Not counted | Allocated week by week | Employee-Friendly |

| New Jersey | May be allocated | Allocated; benefits delayed | Mixed |

| Illinois | Depends on how structured | Allocated if above threshold | Mixed |

| Pennsylvania | Allocated for first X weeks | Fully allocated; significant delay | Strict |

The most reliable source for your specific state’s rules is the official state workforce agency. The CareerOneStop directory maintained by the U.S. Department of Labor links directly to every state’s unemployment agency — takes 90 seconds to find and can save you thousands.

One underappreciated factor: some states look at the language in your severance agreement to determine whether a lump sum is truly non-allocated. If your agreement says “we are paying you 10 weeks of severance in lieu of notice,” some state agencies may treat that as 10 weeks of allocated wages — even if it’s paid upfront. The wording matters. Ask your employer to use language like “one-time separation payment in recognition of service” rather than “payment in lieu of X weeks.”

Real Scenarios: What Actually Happens

Profile: Marketing Manager, $95,000/year, laid off after 5 years at a SaaS company.

Package: $18,250 lump sum (one week per year of service, calculated at base salary).

State: California

What happens: She files for unemployment the Monday after her last day. The lump sum is not allocated as wages. Her weekly California UI benefit of approximately $450 starts after the state’s one-week waiting period. She receives both the full severance and unemployment benefits simultaneously. Total cash flow over the 3-month job search: ~$23,600 between the lump sum and UI benefits combined.

Profile: Software Engineer, $130,000/year, laid off after 8 years at a financial services firm.

Package: 12 weeks salary continuation at regular bi-weekly pay.

State: New Jersey

What happens: He files for UI immediately, but New Jersey allocates the salary continuation week by week. His unemployment claim is effectively suspended for 12 weeks. After the last paycheck clears, he can finally begin collecting NJ’s maximum weekly benefit of $875. He lost 12 weeks of UI payments — roughly $10,500 — compared to what he would have received under a lump sum structure. The total package amount was identical either way.

Profile: Operations Director, $115,000/year, laid off with 3 weeks unused PTO.

Package: $13,269 lump sum severance + $6,634 PTO payout.

State: Texas

What happens: The lump sum doesn’t affect UI eligibility. But Texas treats PTO payouts as wages — so her unemployment claim is delayed by approximately 3 weeks (the PTO allocation period). She files immediately, the state delays her start date by 3 weeks, then benefits kick in. Far better than salary continuation, but the PTO timing cost her roughly $1,200 in benefits. Lesson: in Texas, consider whether PTO is better negotiated as a separate check or absorbed into the lump sum with clear language.

Timing Strategy: How to Maximize Your Benefits

Most people treat severance negotiation as a single question: “How much can I get?” The sharper question is: “How do I structure this to maximize my total cash over the next six months?” Here’s the playbook.

- Negotiate structure before amount. Before you push for an extra week of pay, ask for a lump sum. Many companies will agree without blinking — it’s often simpler for their payroll team too. Frame it simply: “I’d prefer a lump sum payment rather than salary continuation for cash flow reasons.” You don’t need to explain the unemployment angle.

- Review the agreement language carefully. Look for phrases like “in lieu of notice” or “equivalent to X weeks of pay.” Push to replace them with “one-time separation payment in recognition of tenure and service.” This framing is less likely to trigger allocation rules in mixed-stance states.

- Separate PTO from severance where possible. Ask your employer to classify the PTO payout separately on your final paperwork. In some states this doesn’t change the outcome, but in others it limits how far the allocated period extend

- File for unemployment immediately — don’t wait. Even if you’re unsure whether severance will delay things, file the day after your last day (or as soon as your state’s online portal allows). Many states are not retroactive. Every week you delay is a week of potential benefits you’re forfeiting permanently.

- Check your specific state’s rules before you sign. Spend 15 minutes on your state workforce agency’s website. Search “[your state] severance unemployment allocation.” The rules are public and usually clearly documented. Don’t rely on what a colleague experienced — state rules change, and individual circumstances vary.

If your employer is insisting on salary continuation and won’t budge, ask whether they’d be willing to pay it all out in the first payroll cycle as a “final paycheck” equivalent. Some payroll teams will accommodate this with minor administrative changes, effectively converting it to a lump sum payout.

Common Mistakes That Cost You Thousands

After reviewing hundreds of severance situations, the same five mistakes show up over and over. None of them are complicated. All of them are avoidable.

Mistake 1: Focusing only on the total amount, not the structure. A $30,000 severance as salary continuation in Pennsylvania might net you less total cash than a $22,000 lump sum — because you can stack unemployment benefits with the lump sum immediately. Run the math before you sign, not after.

Mistake 2: Waiting to file unemployment “until things settle.” There’s no administrative reason to wait. States aren’t offended by early claims. The waiting period starts when you file, not when you think you’re ready. Every week of delay is typically a permanent loss — most state programs don’t backdate your claim.

Mistake 3: Assuming your HR team will explain this to you. They won’t. HR’s job in a layoff situation is to execute the company’s separation process efficiently. They aren’t your unemployment counselor, and telling you to negotiate for a lump sum doesn’t serve the company’s interests. The information exists — you just have to seek it yourself.

Mistake 4: Not reading the severance agreement for allocation language. The exact wording of your agreement can determine how your state classifies the payment. A sentence that says “this payment covers weeks 1 through 10 following your separation” is very different from “this payment is made as a one-time separation benefit.” Same money, different impact.

Mistake 5: Believing state rules are the same everywhere. I’ve talked to people who relocated from California to New Jersey and were genuinely blindsided by how different the rules were. Always check your current state — not where you worked before, and not what your friend experienced somewhere else.

The Insider View: What HR Actually Thinks

Look, I’ve been in rooms where these severance packages were designed. Here’s what I’ll tell you that most articles won’t: companies almost never think about how severance structure affects your unemployment eligibility. That’s genuinely not part of the conversation.

What HR cares about in a layoff is legal liability protection (the release of claims you sign), administrative simplicity, and consistency across the RIF (reduction in force) cohort. Salary continuation is sometimes preferred by HR teams because it keeps the employee on payroll systems for a defined period, simplifying benefits continuation and reducing the need to cut a large one-time check through accounts payable.

None of that is malicious. But it means the default structure is often whatever is easiest for them — which may not be optimal for you.

The employees who come out ahead in these situations are the ones who ask specific questions before signing. In my experience, most HR teams will accommodate a reasonable request to restructure payment as a lump sum — especially if it’s framed as a preference rather than a demand, and especially if the total amount isn’t changing.

There’s also this: companies want clean separations. A signed agreement that’s accepted without dispute is worth something to them. That gives you modest but real leverage to make structural requests that cost them nothing.

Frequently Asked Questions

Can I collect unemployment if I received severance pay?

Yes, in most cases. Whether your severance affects unemployment depends on how it’s structured and your state’s rules. A lump sum severance in many states — including California, Texas, and New York — doesn’t delay or reduce your benefits. Salary continuation typically does cause a delay, but once those payments end, you can file and receive full benefits assuming you otherwise qualify.

Does lump sum severance delay unemployment benefits?

In most states, a true lump sum severance payment — classified as a one-time separation benefit rather than “pay in lieu of notice” — does not delay unemployment benefits. California, Texas, Florida, and New York generally take this position. However, a handful of states, including Pennsylvania, may still allocate even lump sums over a set number of weeks. Always verify with your state’s workforce agency before assuming.

Does salary continuation affect unemployment eligibility?

Yes, salary continuation almost always delays your unemployment eligibility. Because the payments mirror your regular paycheck — same schedule, same deductions — most states treat them as ongoing wages. You’re considered compensated for those weeks and cannot claim UI until the continuation payments stop. The delay equals the full length of the salary continuation period.

Should I delay filing for unemployment if I’m receiving severance?

No. File immediately after your last day, regardless of your severance arrangement. The state will determine when your benefit period begins based on your situation — that’s their job. If your severance does cause a delay, the clock on your claim still starts from when you filed. Waiting to file only shortens the total period you’re eligible to collect benefits.

Does a PTO payout count as income for unemployment purposes?

It depends on the state. Many states treat accrued PTO payouts as earned wages, which can result in a short delay equal to the number of PTO days paid out. In Texas, for example, PTO is allocated as wages and can push your UI start date back by the equivalent number of weeks. In California, the rules around PTO allocation are more nuanced. Check your state’s specific policy before assuming it won’t matter.

Can I negotiate how my severance is paid — lump sum vs salary continuation?

Yes, and you should. Most employers will agree to a lump sum structure if you ask, especially in individual layoff situations. In large-scale RIFs, there may be less flexibility due to uniformity requirements, but it’s still worth raising. Frame the request professionally: “I’d prefer a lump sum payment for personal cash flow planning.” You don’t need to mention the unemployment angle at all.

Is unemployment reduced by the amount of severance I received?

In most states, unemployment isn’t reduced dollar-for-dollar by your severance — it’s more commonly delayed. Once the severance period (if any) ends, you generally collect your full state-determined weekly benefit. A few states do have offset provisions for high earners, but this is the exception rather than the rule. The practical risk is losing weeks of benefits during a delay period, not a permanent reduction in your weekly payment.

What happens if my employer pays severance after I’ve already started collecting unemployment?

This is more common than people realize — especially when severance agreements are finalized weeks after a layoff date. If your severance is paid after you’ve already filed and begun collecting UI, you’re generally required to report it to your state unemployment agency. Depending on how your state classifies the payment, it may affect your ongoing claim or require a repayment of overlapping weeks. Transparency here is important — UI fraud carries serious penalties.

The Bottom Line on Severance and Unemployment

Here’s what separates people who come out financially whole from those who lose thousands in avoidable delays: they ask one question before signing anything — “Is this a lump sum or salary continuation, and what does my state do with each?”

Does severance affect unemployment? Sometimes yes, sometimes no — but it’s almost never out of your control. The structure of your package matters enormously, and in most cases, you have at least some ability to influence it. Push for a lump sum. File for unemployment immediately. Spend 15 minutes on your state agency’s website. Those three actions alone put you ahead of the vast majority of people navigating a layoff in 2026.

You’ve already lost a job you didn’t want to lose. Don’t lose money on top of it by missing something entirely fixable.

📎 Related on HRGet.com: How to Negotiate a Severance Package: Scripts, Strategies & What HR Won’t Tell You — if you’re still in the negotiation phase, this guide walks you through exactly how to push for a better structure and a higher amount without burning bridges.

Victoria Hale | Former Partner, Freshfields Bruckhaus Deringer | Employment Law Specialist | 20+ Years Advising Multinationals & Executives

Author: Victoria Hale spent over two decades as an Employment Law Partner at Freshfields Bruckhaus Deringer — one of the world’s most prestigious Magic Circle law firms — advising multinational corporations and senior executives on some of the most complex employment disputes in the US and Europe. Her practice covered wrongful termination litigation, executive exits, non-compete enforcement, FLSA compliance, and cross-border workforce restructuring under EU labour law. Now based between London and New York, Victoria writes for HRGet.com to close the gap between legal theory and how employment law actually plays out in the real world — for employees who need to know their rights before it’s too late.