MR

Michael Reeves

Employment & Severance Advisor — Former Senior Counsel, Littler Mendelson | Fortune 500 Restructurings | 18+ Years Across the US & UK

Getting laid off is disorienting enough on its own. Then HR hands you a severance agreement — maybe a lump sum, maybe “salary continuation for eight weeks” — and a very specific question becomes urgent: does severance affect unemployment benefits?

Here’s my honest answer after 18 years advising on severance negotiations and workplace exits: yes, severance can affect unemployment — but not always, not automatically, and not the same way in every state. I’ve seen employees in California collect unemployment the week after signing a $30,000 lump-sum agreement, and I’ve seen employees in other states sit in a benefits gap for two months because of how their salary continuation was structured. Same situation on the surface. Very different outcomes.

The federal government doesn’t control this. The U.S. Department of Labor is clear that severance is generally a matter of agreement between employer and employee, and the Fair Labor Standards Act doesn’t require it. That means the real rules come from your state’s unemployment insurance law — and those rules vary enormously. What follows is everything you need to understand before you sign a severance agreement or file a single claim.

Quick Answer

Severance may affect unemployment benefits depending on your state, the payment structure, and the language in your agreement. A lump-sum payment may have minimal impact in states like California, while salary continuation is more likely to delay eligibility in most states. The type of payment, when it’s paid, and whether it’s allocated to specific weeks all matter — which is why you should never assume the answer and always check your state’s current guidance before filing.

What Counts as Severance Pay (and What Doesn’t)

Before you can understand how severance affects unemployment, you need to know that unemployment agencies don’t simply ask “did you get severance?” They ask something more nuanced: what kind of payment was it, when was it paid, and what period does it cover?

A typical severance package might include any combination of the following:

- A lump-sum cash payment tied to a release of claims

- Weekly or biweekly salary continuation on the normal payroll cycle

- Payout of unused accrued PTO or vacation

- Continuation or COBRA subsidy for health insurance

- Commission settlements or bonus payments

- Outplacement services or career coaching

- Accelerated or modified stock vesting

- Garden leave — where you remain nominally employed but don’t work

Here’s where it gets important: a payment your employer calls “severance” in the offer letter may not be categorized the same way by your state’s unemployment agency. Agencies often distinguish between true severance (consideration for a legal release), dismissal pay, wages in lieu of notice, vacation pay, and salary continuation. Each label can carry a different outcome.

⚠ Watch the Language

Phrases like “this payment represents eight weeks of salary,” “paid through July 31,” or “in lieu of notice” in your agreement signal allocation — meaning a state may treat the payment as wages covering those specific weeks. That distinction can delay your unemployment claim by exactly those weeks.

The Big Rule: State Law Controls the Answer

Unemployment insurance in the United States is a state-administered system. There is no single federal rule governing how severance interacts with your claim. The Department of Labor sets broad parameters, but each state’s statute and agency guidance does the real work — and the differences are significant.

Three states illustrate the spectrum well:

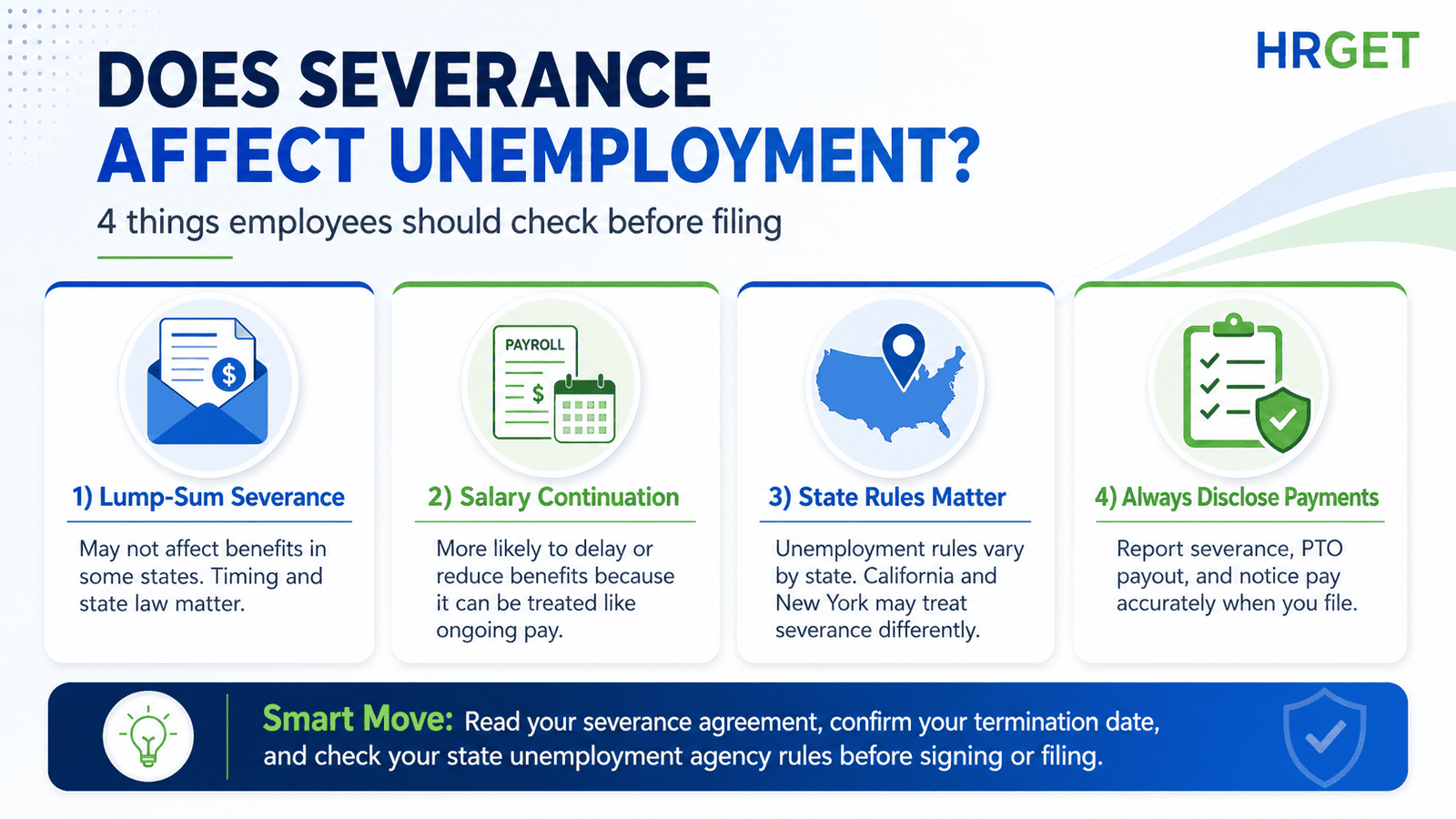

California: The California EDD’s guidance states that severance, dismissal, or separation pay is not wages for unemployment insurance purposes and does not affect eligibility. That means a California-based employee who receives a clean lump-sum severance after a genuine layoff can typically file for unemployment without waiting for the payment period to expire.

New York: The New York Department of Labor takes a different position. Dismissal or severance pay may affect your benefits depending on its amount and timing. New York says you may be eligible once dismissal or severance pay stops or falls below the maximum weekly unemployment benefit rate — which was $504 per week as of early 2026.

Michigan: The Michigan UIA is more explicit still: severance pay can reduce unemployment benefits for the weeks to which the payment is allocated. If the severance isn’t allocated to specific weeks, the reduction may apply in the week the payment is actually made.

Your friend who lives in California might tell you they got severance and unemployment at the same time. Your colleague in Michigan might have waited two months. Both experiences are accurate. The state rules are simply different — which is why taking advice from someone in another state is one of the more expensive mistakes I’ve seen laid-off employees make.

✦ Pro Tip

Before you sign a severance agreement and before you file a claim, go directly to your state’s unemployment agency website and search for these exact phrases: “severance pay unemployment,” “dismissal pay,” “salary continuation,” “pay in lieu of notice,” and “vacation pay unemployment.” The official guidance is usually free, specific, and more reliable than anything you’ll find on a general HR blog.

Lump-Sum Severance vs. Salary Continuation — Why the Difference Matters

This is the single biggest decision point most employees overlook during severance negotiation. The total dollar amount of your package gets all the attention. The structure — which often matters just as much — gets almost none.

Lump-Sum Severance

A lump-sum payment is typically made once, after you’ve signed and returned the severance agreement. You’re no longer employed. The payment arrives as a single deposit.

In states like California, this structure often has the least impact on unemployment because the payment isn’t tied to ongoing payroll or allocated to future weeks. In other states, the impact depends on whether the agreement language allocates that lump sum to a specific period.

Salary Continuation

Salary continuation means your employer keeps issuing regular paychecks — usually biweekly — for a defined period after your role is eliminated. Emotionally, you feel unemployed. Legally, you may still be on payroll.

This structure is far more likely to create a waiting period before unemployment kicks in. The state sees ongoing wage payments. Even if your employer confirms you’re “terminated,” the regular pay disbursements can look functionally identical to being employed — and agencies often treat them that way.

| Payment Structure | Typical Unemployment Impact | Best For |

|---|---|---|

| True lump-sum severance (post-termination) | Minimal in CA; varies by state; allocation language matters | Employees prioritising faster unemployment access |

| Salary continuation on payroll | Higher risk of delaying unemployment; treated as wages in most states | Employees who prioritise benefits continuation and payroll perks |

| Lump sum allocated to specific weeks | May reduce or delay benefits for those weeks | Negotiation target: remove allocation language where possible |

| PTO / vacation payout | State-specific; often treated as wages for covered weeks | Report separately; not interchangeable with severance |

| WARN Act pay / pay in lieu of notice | State-specific; some treat it as wages, delaying benefits | Ask HR for explicit label and check state rules immediately |

I’ve advised clients who received identical $25,000 packages — one as a lump sum, one as salary continuation — and had completely different unemployment timelines. Neither employer intended to create a disadvantage. The structure wasn’t negotiated. And one employee effectively lost two months of benefits as a result.

Real Scenarios: How Severance Changes Your Claim

📋 Scenario 1 — Lump Sum After Layoff

A product manager in San Jose is laid off in a tech restructuring. Last working day: April 30. Two weeks later, she receives a $22,000 lump-sum payment after signing a mutual release. She files for California unemployment immediately after April 30. Because California EDD treats true severance as non-wages, her claim proceeds. The $22,000 doesn’t delay her first benefit payment.

Smart move: She filed on her actual last day of work, not after receiving the payment — and disclosed the severance payment honestly on her claim.

📋 Scenario 2 — Salary Continuation for Eight Weeks

A finance manager in Detroit is told his role is eliminated. HR says: “We’ll keep you on payroll through June 30.” His official last day of active work is May 1. He files for Michigan unemployment in early May. The UIA sees ongoing wage payments through June 30 and delays his claim accordingly. He didn’t lose the severance — he just couldn’t access unemployment until those payments stopped.

Smart move: Before his next role, he’d negotiate for a lump sum rather than continuation — and ask HR to confirm his official termination date in writing upfront.

📋 Scenario 3 — Severance Plus PTO Payout

A marketing director in Chicago receives four weeks of severance plus a $4,200 payout for unused vacation. She assumes both are treated identically on her Illinois claim. They’re not. Her state treats PTO payout as wages tied to the period the vacation would have covered. Reporting both as “severance” causes an overpayment flag — avoidable if she’d separated them on the form.

Smart move: Always report each payment type using the exact label from your agreement.

How to File for Unemployment When You Have Severance

The most common error I see is employees either delaying filing unnecessarily (assuming severance blocks them) or filing without disclosing severance (and facing overpayment consequences later). Neither is necessary.

Confirm your official last day of work in writing

Read the severance agreement’s allocation language carefully

Check your state agency’s official severance guidance

File your claim and disclose all payments fully

Respond to agency follow-ups promptly and keep your records

5 Mistakes Employees Make After Getting Severance

Mistake 1: Assuming Severance Automatically Blocks Unemployment

This is false in multiple states. California’s EDD guidance is explicit that true severance is not wages for unemployment purposes. Employees who wait for their severance period to expire before filing — when they were already eligible — lose benefits they deserved. That delay can mean $500–$800 per week gone permanently, since benefits aren’t retroactive once you miss a filing week.

Mistake 2: Assuming Severance Never Matters

Also false. Michigan, New York, and many other states treat severance in ways that can delay or reduce benefits. Assuming you’ll be fine because a colleague in another state was fine is one of the most expensive assumptions a laid-off employee can make in 2026.

Mistake 3: Not Reading the Allocation Language in the Agreement

Most employees read the dollar amount and skim the rest. But the allocation language is often buried in standard boilerplate. Phrases like “this payment covers the period of May 1 through June 30” can add eight weeks to your benefits waiting period. Catching that before you sign — not after — gives you something to negotiate.

Mistake 4: Lumping PTO Payouts and Bonus Settlements In with Severance

Each payment type may be treated differently. PTO payout is commonly treated as wages for the weeks the vacation would have covered. A commission settlement may be treated as back wages. Reporting everything as “severance” on your application invites flags, overpayment notices, and delays that take months to resolve.

Mistake 5: Signing Without Checking the Structure First

Most severance agreements include a review period — typically 21 days for employees over 40 under the ADEA, or a shorter period for others. Use it. The structure of payment (lump sum vs. continuation, allocation language vs. clean consideration language) can have a multi-thousand-dollar impact on your total transition income, and changing it after signing is usually not possible.

🔍 The Insider View — What HR Actually Thinks About This

Here’s something most articles won’t say: HR departments often don’t design severance agreements with unemployment implications in mind. The salary continuation structure frequently exists because it’s administratively simple — you stay on payroll, benefits continue automatically, and HR doesn’t have to process a separate payment. It’s convenient for the employer, not optimised for you. When you ask HR to convert salary continuation to a lump sum, the answer is often yes — because it’s actually simpler for payroll to cut a single check than run you on cycle for two more months. The ask is less disruptive than you think.

Smart Strategy Before You Sign the Agreement

If you want to protect both your severance and your unemployment eligibility, review the agreement through three lenses before you pick up the pen.

1. Timing — When Does the Payment Land?

A lump sum paid after your official termination date typically creates cleaner separation between severance and unemployment. Salary continuation that runs through payroll blurs the line. If you have a choice, ask for payment after termination, not through continued payroll.

2. Label — What Does the Agreement Call the Money?

Severance, dismissal pay, transition pay, continuation pay, pay in lieu of notice, and wages each carry different implications at the state level. “Consideration for a release of claims” is often the cleanest framing for unemployment purposes because it ties the payment to a legal transaction, not to a wage period. Ask your employer’s HR team or your own employment attorney whether that language is achievable.

3. Allocation — Does the Agreement Tie Payment to Specific Weeks?

This is the most negotiable and most overlooked element. If the agreement currently says “this payment represents 12 weeks of compensation,” try negotiating to remove that language — or replace it with language that explicitly states the payment is not allocated to any specific weeks and represents consideration for your release of claims. In many states, this single change determines whether your unemployment starts this month or in three months.

Specific questions worth raising with HR or an employment attorney:

- “Can the payment be structured as a lump sum after my termination date rather than through payroll?”

- “Can the agreement clarify that my official employment ends on [separation date]?”

- “Can the payment be described as consideration for a release of claims, without week-by-week allocation?”

- “Is the PTO payout included in the main payment or treated separately?”

I’ll be honest — not every employer will agree to every change. But many will agree to structural adjustments that don’t change their bottom-line cost. The ask is worth making.

Severance, Taxes, and Unemployment: The Triple Hit

Even if your severance doesn’t delay your unemployment claim, there’s a second financial layer that catches most laid-off employees by surprise: taxes.

The IRS is clear that severance pay is taxable income, treated as wages, and subject to federal income tax, Social Security, and Medicare withholding. Unemployment compensation is also taxable at the federal level — something many employees don’t realise until their tax return arrives.

That creates three simultaneous financial pressures for most laid-off employees in 2026:

- Unemployment eligibility timing — your state may delay your first benefit payment depending on severance structure

- Cash flow management — severance and unemployment arrive at different times; your transition budget needs to account for the gap

- Tax liability — both severance and unemployment compensation are taxable; if insufficient tax was withheld, you’ll owe at filing time

The practical move: set aside 22–28% of your gross severance payment immediately if you’re in a mid-range federal bracket. Don’t assume the employer’s withholding covered everything — supplemental wage withholding rates and your actual effective rate often diverge. And if you’re collecting unemployment, check whether your state allows voluntary federal withholding on benefit payments. For many people, opting in saves a painful bill in April.

⚠ Real Risk

I’ve worked with employees who spent their full severance net payout, assumed unemployment would cover living expenses, and then received a $6,000–$9,000 federal tax bill in the spring. The combination of severance income, unemployment compensation, and no proactive withholding is a predictable trap. Plan for it upfront rather than discovering it after the fact.

✦ VERDICT

Does severance affect unemployment benefits? Yes — but only in specific circumstances that depend on your state, how the severance is structured, and what language is in your agreement. A lump-sum payment after termination may have no impact in California. Salary continuation on a biweekly payroll cycle may delay your Michigan claim for the full continuation period. The difference between these outcomes is often a single conversation with HR before you sign. Read the agreement carefully, check your state’s official guidance, disclose everything honestly when filing, and don’t treat the severance structure as fixed — it’s almost always negotiable.

Frequently Asked Questions

Can I collect unemployment if I get severance pay?

Yes, you may be able to collect unemployment after receiving severance, but state law controls the outcome. California generally treats true severance as non-wages and allows claims to proceed immediately. New York may delay eligibility until dismissal pay falls below the weekly benefit rate. Michigan can reduce benefits for the weeks to which severance is allocated. Always check your state agency’s current guidance before filing — and file on time even if you’re uncertain.

Does lump-sum severance affect unemployment benefits?

A lump-sum payment typically has less impact than salary continuation, but it isn’t automatically harmless. Some states may reduce or deny benefits in the week the payment is received, or may allocate it across the period it represents. If the agreement says the lump sum “represents 10 weeks of pay,” the state may treat it as covering those 10 weeks — potentially delaying your claim by exactly that period.

Does salary continuation affect unemployment benefits?

Salary continuation is the riskiest structure for unemployment purposes. Because your employer keeps you on payroll and issues regular paychecks, the state often treats those payments as ongoing wages — delaying your eligibility until the continuation period ends. Always confirm your official termination date in writing before the continuation period begins, and ask HR whether conversion to a lump sum is possible.

Should I wait until my severance ends before filing for unemployment?

Not necessarily. In states where severance doesn’t count as wages — like California — waiting unnecessarily can cost you weeks of benefits you were already entitled to, since those missed weeks typically aren’t retroactively paid. File on time, disclose the severance accurately, and let the state determine how it’s treated. Waiting without first checking state rules is a common and costly mistake.

Do I have to report severance when filing for unemployment?

Yes, always. If the application asks about severance, dismissal pay, separation pay, PTO payout, wages, or any other payments received around your termination, report them fully and accurately. Failing to disclose severance can result in overpayment demands, financial penalties, or a fraud determination — outcomes far worse than a short delay in benefits.

Can I negotiate severance to protect unemployment eligibility?

Yes. The structure of your severance matters almost as much as the amount. You can negotiate for a lump-sum payment after termination, cleaner language that avoids week-by-week allocation, and explicit confirmation of your separation date. If the severance amount is $15,000 or more, speaking with an employment attorney in your state before signing is worth the consultation cost — the structural change alone can be worth thousands.

Is PTO payout treated the same as severance for unemployment?

Not always. Some states treat PTO or accrued vacation payout as wages tied to specific weeks, which can affect eligibility differently from true severance. Always report each payment type separately on your unemployment application and use the exact wording from your severance agreement — don’t lump PTO in with severance or vice versa. A single misclassification can generate an overpayment flag that takes months to resolve.

Is severance pay taxable even if it delays unemployment?

Yes. The IRS classifies severance as taxable wages subject to income tax, Social Security, and Medicare withholding — regardless of how your state treats it for unemployment purposes. Unemployment compensation is also taxable federally. Budget for both. Many employees are surprised by a significant tax bill in the spring following a layoff year, particularly when severance and unemployment income are combined without adequate withholding.

Related Reading: If you’re heading into a severance negotiation, don’t leave money on the table. Read our guide on how to negotiate severance pay — including the specific asks that most employees never think to make.

This article provides general educational information and should not be treated as legal or financial advice. Unemployment rules vary by state and are subject to change. Verify current guidance with your state unemployment agency before filing. If your severance package is substantial, consult an employment attorney in your jurisdiction before signing.

Michael Reeves | Former Senior Counsel, Littler Mendelson | Severance & Restructuring Specialist | 18+ Years in Employment Law

Author bio: Michael Reeves spent nearly two decades as Senior Counsel at Littler Mendelson — one of the world’s largest employment law firms — advising on mass layoffs, corporate restructurings, and severance negotiations for Fortune 500 companies across the US and Europe. He has worked both sides of the table: structuring cost-efficient separation packages for employers and, more recently, helping employees understand exactly where their leverage lies. Based between Chicago and London, Michael writes for HRGet.com to demystify the legal and financial dimensions of layoffs — so employees stop leaving money on the table.