By HRGet Editorial Team | Updated April 2026 | 12 min read

Changing jobs is one of the best wealth-building moves you can make — but most people completely drop the ball on their 401(k) rollover when changing jobs. The account gets forgotten, the wrong option gets chosen in a rush, and what should be a simple transfer quietly costs thousands of dollars in taxes and lost compounding.

I’ve seen it happen dozens of times — a solid earner, smart person, leaves a job with $60,000 in their 401(k) and either cashes it out impulsively or just leaves it orphaned at an old employer for years. Neither is a good outcome.

This guide covers exactly what to do with your 401(k) when you switch jobs — your four options laid out plainly, the step-by-step rollover process, the one critical mistake most guides gloss over, and the tax rules you need to understand before you touch anything.

What Happens to Your 401(k) When You Leave a Job

Here’s the thing most people don’t realize: your 401(k) doesn’t follow you out the door automatically. It stays with your old employer’s plan — invested, tax-deferred, technically yours — but increasingly disconnected from your financial life.

If your balance is under $1,000, your old employer can actually force a cash distribution without your input. If it’s between $1,000 and $5,000, they can roll it into a default IRA on your behalf. Over $5,000? It sits there until you decide what to do. That “decision window” is where most people lose money — not through dramatic bad choices, but through simple inaction.

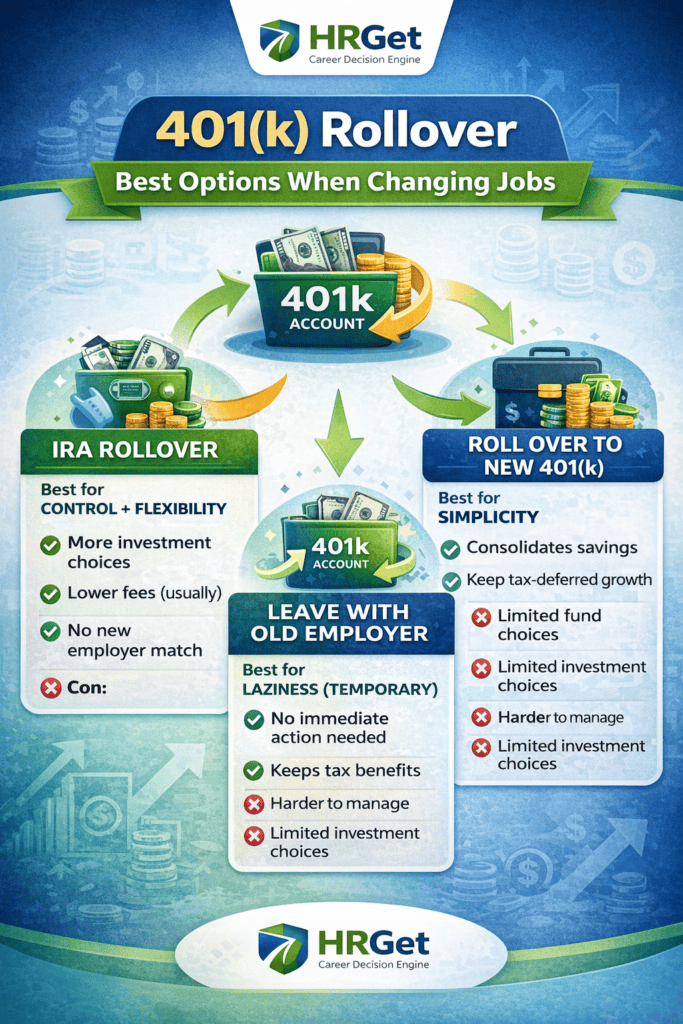

You have four paths forward. Each has real trade-offs that depend on your balance, your new employer’s plan quality, and how actively you want to manage your retirement savings.

💼 Insider View:

In my experience reviewing retirement plan decisions with employees during offboarding, the majority defaulted to “leaving it for now.” That’s fine for a month. It becomes a problem when “now” turns into three years and you’ve forgotten your old provider’s login credentials, changed your email address twice, and moved apartments. Lost retirement accounts are more common than you’d think — the National Registry of Unclaimed Retirement Benefits tracks billions in forgotten funds.

Your 4 Rollover Options — Pros, Cons, and the Real Trade-offs

Let’s be direct. There’s a clear hierarchy here, and I’ll tell you where I stand on each.

Option 1: Leave It With Your Old Employer

Your money stays invested and keeps growing tax-deferred. No action required. This sounds appealing when you’re in the middle of a job transition and have seventeen other things to deal with.

The downside: you can’t make new contributions, your investment options are locked to whatever that employer’s plan offers, and — realistically — out-of-sight often becomes out-of-mind. It’s a passable short-term move, not a long-term strategy.

Option 2: Roll Over to Your New Employer’s 401(k)

Consolidation is genuinely underrated. One account, one login, one set of statements. And if your new employer’s plan offers strong low-cost index funds, this can be a smart move.

The catch: not all 401(k) plans are equal. Some employer plans carry expense ratios of 0.8%–1.2% on funds that you could hold in an IRA for 0.03%–0.10%. Over 20 years on a $50,000 balance, that fee difference compounds into tens of thousands of dollars. Always compare the investment menu before consolidating.

Option 3: Roll Over to an IRA (Most Flexible Option)

This is the option most financially informed professionals choose — and for good reason. An IRA (Traditional or Roth, depending on your tax situation) gives you access to virtually unlimited investment options and typically lower costs than any employer-sponsored plan.

Platforms like Fidelity, Vanguard, and Schwab offer commission-free index funds with expense ratios under 0.05%. You’re in full control. The only downside is that it requires slightly more active decision-making — you’ll need to choose your investments once the funds land.

Option 4: Cash It Out (Almost Always a Mistake)

I’ll be honest — there are very few scenarios where this is the right call. If you’re under 59½, you owe a 10% early withdrawal penalty on top of ordinary income tax. On a $40,000 balance, that can mean handing over $15,000–$18,000 to the IRS immediately. The money you keep has lost all future compounding potential.

Emergency situations aside, cashing out a 401(k) is one of the most expensive financial decisions a working professional can make. Don’t do it unless you have truly exhausted every other option.

| Option | Best For | Tax Impact | Flexibility | Recommended? |

|---|---|---|---|---|

| Leave with old employer | Short-term / indecisive | None (deferred) | Low | Temporary only |

| Roll to new 401(k) | Simplicity seekers | None if direct | Medium | ✅ If fees are low |

| Roll to IRA | Control + cost-conscious | None if direct | High | ✅ Usually best |

| Cash out | True emergency only | Income tax + 10% penalty | N/A | ❌ Avoid |

Direct vs. Indirect Rollover: The Difference That Can Cost You Big

This is where a lot of people make a painful mistake, and most articles treat it as a footnote. It deserves its own section.

When you initiate a rollover, your old plan will ask how you want the funds distributed. There are two methods:

Direct Rollover (What You Always Want)

The funds transfer directly from your old 401(k) provider to the receiving account — either your new 401(k) or your IRA. You never touch the money. No taxes are withheld. No penalties apply. This is clean, efficient, and the right way to do it.

Technically, even with a “direct” rollover, some plans issue a check — but it’s made payable to your new institution (e.g., “Fidelity FBO [Your Name]”), not to you personally. That’s still a direct rollover for tax purposes.

Indirect Rollover (Handle With Extreme Care)

The funds are issued to you. Your old provider is required by the IRS to withhold 20% for taxes. You then have 60 days to deposit the full original amount — including the 20% that was withheld — into a qualifying retirement account.

Here’s the trap: if you only deposit what you received (i.e., 80% of the original balance), the withheld 20% is treated as a taxable distribution, subject to income tax and the 10% early withdrawal penalty. You’d need to come up with the withheld amount out of pocket to avoid the tax hit.

⚠️ Warning:

The 60-day rule for indirect rollovers is strict. Miss it by one day — for any reason, including a bank processing delay — and the IRS treats the entire amount as a taxable distribution. In 2026, the IRS continues to offer a “self-certification” waiver for certain missed deadlines under Revenue Procedure 2016-47, but it’s paperwork, stress, and risk you don’t need. Just use a direct rollover.

Step-by-Step 401(k) Rollover Process

Once you’ve decided where the money is going, the process is more straightforward than most people expect. Here’s exactly how to execute it.

Decide the Destination Account

New 401(k) or IRA? Lock this in before you do anything else. If rolling to an IRA and you don’t already have one, open it first. Fidelity and Schwab both allow you to open a Traditional IRA online in about 10 minutes with no minimum balance requirement.

Confirm the Receiving Account Details

If rolling to a new 401(k): confirm with your new HR team or plan administrator that they accept incoming rollovers — most do, but it’s worth a quick check. Get the exact account number and the plan’s mailing address for checks. If rolling to an IRA: locate your account number and the custodian’s rollover address (usually different from their regular deposit address).

Contact Your Old 401(k) Provider

Call or log in to your old plan’s portal and initiate a direct rollover — use exactly those words. Specify the receiving institution and account. They’ll either initiate an electronic transfer or mail a check made payable to the new institution.

Track the Transfer

Most transfers complete within 5–10 business days for electronic transfers, or 2–3 weeks if a physical check is mailed. Follow up if you haven’t seen the funds arrive within 3 weeks — checks do occasionally get lost or sent to outdated addresses on file.

Invest the Funds — Don’t Leave Them in Cash

This is the step people most often forget. When rollover funds arrive in an IRA or new 401(k), they’re typically placed in a money market or default cash position. They’re not automatically invested. Log in, allocate to your target funds, and confirm the purchase. Leaving $40,000 sitting in a 4.5% money market when you intended it to be in an index fund is a silent, ongoing cost.

💡 Pro Tip:

Always ask your old plan for a “trustee-to-trustee transfer” rather than just saying “rollover.” This phrasing signals to the administrator that you want a direct transfer, reduces the chance of them defaulting to sending you a check, and creates a clear paper trail for your records. Keep every confirmation email and letter — you may need them at tax time.

Real Scenario: Two Professionals, Two Very Different Outcomes

📊 Real Scenario:

Priya, 32, Software Engineer in Austin — left her job with $55,000 in a 401(k). She spent 20 minutes opening a Fidelity IRA, requested a direct rollover, invested the funds in a total market index fund (expense ratio: 0.015%), and forgot about it in the best possible way. At 55, assuming 7% average annual returns, that $55,000 is worth approximately $250,000. Zero taxes paid, zero penalties.

Marcus, 34, same starting balance — cashed out his $55,000 when switching jobs because he was stressed, had a credit card balance he wanted to clear, and figured he’d “start fresh” with his new employer’s plan. After the 10% penalty and a 22% federal tax rate, he walked away with roughly $37,400. The amount he lost to taxes and penalties alone? About $17,600. The compounding he forfeited? Over 20 years, that original $55,000 would have grown to ~$250,000. Marcus gave up ~$212,000 in future wealth to clear a credit card bill.

The gap between those two outcomes isn’t intelligence or income — it’s one decision, made in 20 minutes.

Smart Strategy: What Financially Savvy Job-Changers Actually Do

Look, here’s what the people I’ve seen handle this well actually do — and it’s not complicated.

Step 1: IRA first, everything else second. They open an IRA before they even give notice at their old job. By the time they leave, the receiving account is already ready. The rollover gets initiated on their last day or the week after, not six months later.

Step 2: Consolidation as a habit. Every time they change jobs, old 401(k)s get rolled into the same IRA. By their mid-40s, they have one consolidated retirement account they can actually manage, not four orphaned accounts at four old employers.

Step 3: Low-cost index funds, not fund menus. Most 401(k) plans offer a target-date fund or a handful of actively managed options. An IRA at Vanguard, Fidelity, or Schwab gives access to index funds with expense ratios so low they’re practically rounding errors — 0.03% vs the 0.8%–1.2% you might find in an older employer plan. On $100,000 over 20 years, that difference in fees is worth more than $30,000.

Step 4: Roth conversion consideration. If you’re rolling from a Traditional 401(k) and you’ve had a particularly low-income year — career break, new job with ramp-up period — it may be worth exploring a Roth conversion. You’d pay taxes now at a lower rate in exchange for tax-free growth forever. This one requires a conversation with a tax professional, but it’s a genuine opportunity that a job transition can create.

5 Common 401(k) Rollover Mistakes That Cost Real Money

These aren’t hypothetical — I’ve seen every one of them play out in real offboarding conversations.

1. Forgetting the account exists. This sounds absurd, but it happens constantly — especially with smaller balances from early-career jobs. The National Registry of Unclaimed Retirement Benefits estimates there are tens of billions in unclaimed 401(k) assets in the US. Check your old accounts. All of them.

2. Choosing an indirect rollover without understanding the 60-day rule. Old employer sends you a check, life gets busy, deadline passes. Suddenly a clean rollover becomes a taxable event. Always specify direct rollover.

3. Not comparing fees before rolling to a new 401(k). Your new employer’s plan might charge more than your IRA would. Always look at the plan’s Summary Plan Description (SPD) and compare expense ratios before consolidating.

4. Leaving rollover funds uninvested. Money arrives in the receiving account and sits in cash earning 4%–5% while you meant it to be in equities. This is a particularly costly mistake in a bull market. Always allocate immediately.

5. Rolling a Roth 401(k) into a Traditional IRA. These are different account types with different tax treatment. A Roth 401(k) should roll into a Roth IRA to preserve its tax-free status. Rolling it into a Traditional IRA by mistake means you’ve lost the tax-free growth benefit. Your old plan administrator should flag this, but confirm it yourself.

Tax Rules You Must Understand Before You Move Anything

You don’t need to be a tax expert, but you do need to understand a few key rules before initiating any rollover.

| Scenario | Tax Withheld? | Penalty? | IRS Form |

|---|---|---|---|

| Direct rollover to IRA or new 401(k) | No | No | 1099-R (Box 7: Code G) |

| Indirect rollover, completed within 60 days | 20% withheld upfront | No (if fully redeposited) | 1099-R + Form 5498 |

| Indirect rollover, missed 60-day deadline | 20% withheld + income tax on remainder | 10% if under 59½ | 1099-R (taxable distribution) |

| Cash distribution (any reason) | 20% withheld + full income tax | 10% if under 59½ | 1099-R (taxable distribution) |

| Roth 401(k) → Roth IRA direct rollover | No | No | 1099-R (Code H) |

One additional nuance: even a completed direct rollover generates a Form 1099-R from your old plan and a Form 5498 from your new IRA custodian. Some people panic when they receive a 1099-R and assume they owe taxes. You don’t — as long as the rollover was completed properly and reported correctly on your tax return. Your tax software or preparer handles this with a couple of checkboxes.

💼 Insider View:

The IRS’s one-rollover-per-year rule is a trap that catches sophisticated investors off guard. You’re limited to one indirect (60-day) rollover per IRA per 12-month period — not per calendar year. Direct rollovers are exempt from this limit entirely. Another reason to always go direct.

Bottom Line: What Should You Actually Do?

If you want simplicity and your new plan has low-cost funds → Roll to new 401(k)

If you want maximum flexibility and lower fees → Roll to IRA (the default best choice for most people)

If you want to make an expensive mistake → Cash out

The 401(k) rollover when changing jobs isn’t complicated — but it does require a deliberate decision within your first few weeks at your new role. Handle it intentionally and it becomes one of the best financial moves you’ll make this year.

FAQs: 401(k) Rollover When Changing Jobs

How long does a 401(k) rollover take when changing jobs?

Most direct rollovers complete within 1–3 weeks. Electronic transfers between major custodians (Fidelity, Vanguard, Schwab) typically settle in 5–10 business days. If your old plan sends a physical check, expect 2–3 weeks. Follow up after 15 business days if funds haven’t arrived — checks do occasionally get sent to old addresses on file.

Can I roll over my 401(k) to an IRA while still employed?

Generally, no — most 401(k) plans only permit rollovers after you’ve left the employer. The exception is “in-service distributions,” which some plans allow after age 59½. Check your plan’s Summary Plan Description if you’re exploring this option while still employed.

Do I pay taxes when rolling over a 401(k) to an IRA?

Not if you do it correctly. A direct rollover from a Traditional 401(k) to a Traditional IRA is a non-taxable event — you’ll receive a Form 1099-R, but with the correct distribution code it won’t trigger tax liability. You only pay taxes if you convert to a Roth IRA or take a cash distribution.

What happens if I miss the 60-day rollover deadline?

The IRS treats the distribution as taxable income for that year. If you’re under 59½, you’ll also owe a 10% early withdrawal penalty. The IRS offers a self-certification waiver for certain qualifying reasons (illness, postal errors, severe financial hardship) under Rev. Proc. 2016-47, but it’s not guaranteed and involves additional paperwork. The easiest solution is to avoid indirect rollovers entirely.

Should I roll my 401(k) into a Roth IRA when changing jobs?

Only if you’re prepared to pay income taxes on the converted amount now. Converting a Traditional 401(k) to a Roth IRA triggers a taxable event — the full balance is added to your income for that year. This can make sense if you’re in a low income year or expect to be in a higher tax bracket in retirement. It requires careful tax planning, not a snap decision during a job transition.

Can I have multiple 401(k) accounts from different jobs?

Yes, there’s no legal limit on how many 401(k) accounts you can hold. However, managing multiple accounts across multiple old employers is genuinely difficult — different login credentials, different investment menus, different fee structures. Most financial advisors recommend consolidating into a single IRA for simplicity, lower costs, and better long-term visibility.

Is a 401(k) rollover to an IRA better than keeping it in the old plan?

For most people, yes — primarily because of investment flexibility and fees. An IRA lets you invest in virtually any publicly traded security, with expense ratios often 10x–20x lower than the funds available in an older employer’s plan. The main exception: if you’re over 55 and might need penalty-free access before 59½, a 401(k) has slightly more favorable early withdrawal rules under the “Rule of 55.”

What if my old 401(k) balance is very small — under $5,000?

For balances under $1,000, your old employer can cash you out automatically. For $1,000–$5,000, they may roll it into a default IRA on your behalf. In both cases, you should act quickly to take control — contact the plan or the receiving IRA custodian and roll the funds into an account you actively manage.

Navigating a job change involves more than just the 401(k). If you were laid off or are negotiating exit terms, read our guide:

How to Negotiate Severance Pay: What You’re Actually Entitled To →

The Bottom Line on 401(k) Rollovers When Changing Jobs

Here’s what it comes down to: a 401(k) rollover when changing jobs is not administrative busywork. It’s a wealth decision that will compound — for better or worse — over the next 20–30 years. The mechanics are simple. The stakes are real.

Direct rollover to an IRA is the right move for the majority of job changers. It takes about 30 minutes to execute, costs nothing, and gives you the best long-term flexibility and cost structure. If your new employer’s plan is genuinely excellent — strong fund menu, low fees — consolidating there is also a solid choice.

What’s not a choice? Leaving it forgotten at your old employer forever, or worse, cashing it out and handing a meaningful chunk to the IRS. You worked for that money. Make sure it keeps working for you.

Emily Carter is a career coach and former McKinsey talent advisor with 15+ years of experience helping professionals navigate career transitions, promotions, and high-stakes job decisions. She has advised professionals across consulting, technology, finance, and corporate leadership roles on offer negotiations, career positioning, and long-term growth strategy.

Role: Career Coach & Ex-McKinsey Talent Advisor: Focuses on helping professionals make smarter career moves—switching jobs, negotiating offers, and long-term career growth. She blends structured thinking with real-world coaching insights.