Losing your job is stressful enough. Losing your health insurance at the exact same moment? That’s where most laid-off professionals panic — and expensive, avoidable mistakes get made. The COBRA vs ACA Marketplace decision is one of the most financially consequential choices you’ll face in the first 60 days after a layoff, and most people make it on autopilot.

I’ve spent 15 years in HR, watching employees reflexively elect COBRA without running a single number — then quietly hemorrhage $800, $1,000, even $1,400 a month on insurance they could have replaced for a fraction of the cost. This guide is the conversation I wish every laid-off professional could have before they check that COBRA election box.

By the end of this article, you’ll know exactly which option fits your situation, what the real cost difference looks like in dollar terms, and a hybrid strategy that most people never consider — one that gives you maximum flexibility without locking you into a bad decision on day one.

What Happens to Health Insurance After a Layoff?

Here’s what most HR departments don’t explain clearly on your last day: your employer-sponsored health insurance doesn’t just “continue” — it ends. Specifically, it ends either on your last day of employment or at the end of that calendar month, depending on your company’s plan rules. After that, you’re on your own — and you have a 60-day window to act before the door closes.

Under US law, a job loss is a “qualifying life event” that triggers two separate Special Enrollment opportunities: one for COBRA continuation coverage (governed by the Consolidated Omnibus Budget Reconciliation Act) and one for an ACA Marketplace plan (via healthcare.gov or your state exchange). A third option — joining a spouse or domestic partner’s employer plan — exists if applicable and is often the best of all worlds.

Most people get stuck between COBRA and ACA. And the choice, frankly, isn’t close for the majority of laid-off workers in 2026. But the exceptions matter enormously.

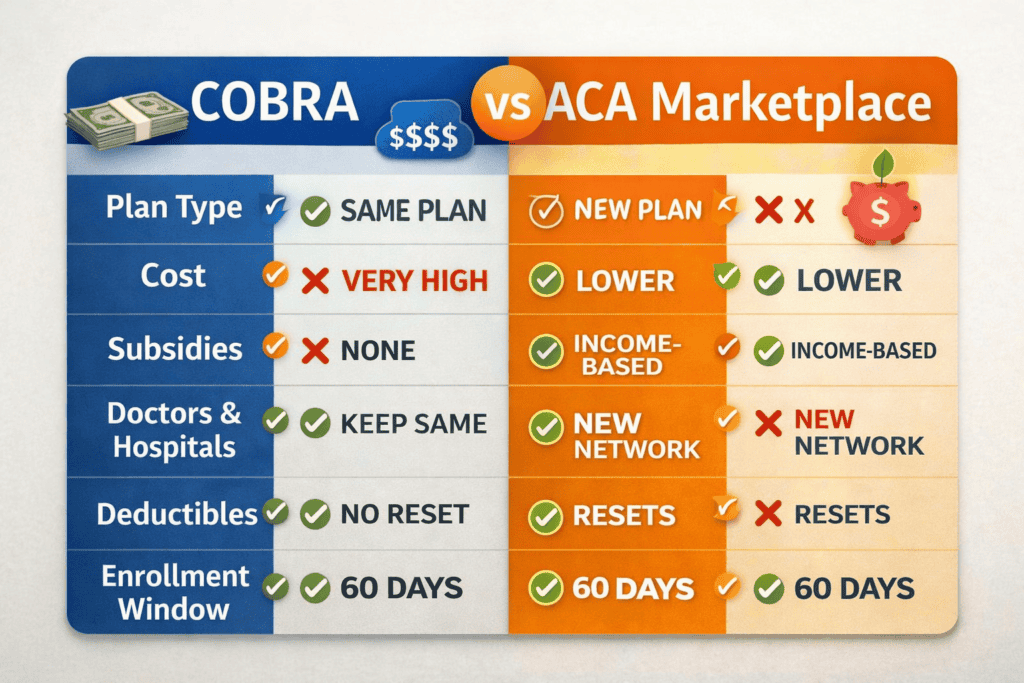

COBRA vs ACA Marketplace: Quick Comparison

| Feature | COBRA | ACA Marketplace |

|---|---|---|

| Keeps your exact same plan | ✅ Yes — zero disruption | ❌ New plan, new network |

| Monthly premium | ❌ Very high ($600–$1,400+) | ✅ Often much lower with subsidies |

| Income-based subsidies | ❌ None | ✅ Yes — layoff dramatically increases eligibility |

| Doctor/network continuity | ✅ Same providers | ❌ Need to verify new network |

| Deductible resets | ✅ No reset | ❌ Deductible resets on new plan |

| Enrollment window | 60 days from job loss | 60 days from losing job-based coverage |

| Max duration | 18 months (36 in some cases) | Year-round with qualifying event |

| Best for | Active treatment, near deductible limit | Healthy, cost-sensitive, expecting longer job search |

What Is COBRA? Costs, Pros, and Real Drawbacks

COBRA — the Consolidated Omnibus Budget Reconciliation Act — gives you the legal right to continue your employer-sponsored health coverage for up to 18 months after losing your job. The catch: you now pay the entire premium. Both your share and your employer’s share, plus a 2% administrative fee on top.

Here’s what that actually means in real money. Say your employer plan cost $900/month total. You paid $180 through paycheck deductions. Your employer quietly covered $720. Under COBRA, you’re suddenly responsible for the full $900 — often closer to $918 after the admin fee. That’s a 5x jump in your monthly out-of-pocket cost. For families, total COBRA premiums can easily hit $1,800–$2,400/month.

When COBRA is genuinely worth it

COBRA earns its premium in a narrow but important set of situations. If you’re in the middle of cancer treatment, a pregnancy, physical therapy following surgery, or managing a chronic condition with a specialist you’ve spent months finding — switching plans mid-year is a real clinical risk, not just an inconvenience. New ACA networks may not include your doctor, your hospital, or your current prescriptions at the same tier.

The second scenario where COBRA wins: you’re late in the plan year and you’ve already met a significant portion of your deductible. Switching resets that clock to zero. If it’s October and you’ve paid $3,500 toward a $4,000 deductible, absorbing a few months of COBRA premiums to protect that credit often makes mathematical sense — especially if you anticipate more medical spending before December 31.

What Is ACA Marketplace? How Subsidies Change Everything

The Affordable Care Act Marketplace — often called Obamacare — lets you buy an individual or family health insurance plan through the federal exchange at healthcare.gov or your state’s equivalent. What most people don’t grasp until they actually log in: a layoff can make you eligible for subsidies that slash your monthly premium to a fraction of what COBRA costs.

Here’s the mechanism. ACA Premium Tax Credits are based on your projected Modified Adjusted Gross Income (MAGI) for the calendar year — not your pre-layoff salary. If you earned $95,000 for the first six months of the year, then lost your job, your projected annual income for ACA purposes might be significantly lower depending on severance, unemployment benefits, and any freelance income. That drop in projected income can push you well into subsidy territory.

The subsidy math in plain English

For 2026, ACA subsidies are available to individuals earning up to 400% of the Federal Poverty Level — roughly $60,240 for a single adult. But enhanced subsidies from the Inflation Reduction Act extension (still in effect) cap your premium contribution at a percentage of your income even above that threshold for many plans. A single person projecting $35,000 in income for the year might pay as little as $80–$150/month for a Silver plan in most major metros.

The tradeoff: you’re on a new plan with a new network. Bronze plans carry lower premiums but higher deductibles — fine if you’re healthy and rarely use insurance. Silver plans hit the sweet spot for most people: moderate premiums, reasonable deductibles, and cost-sharing reductions if your income qualifies. Gold plans make sense if you anticipate significant healthcare usage and want predictable costs.

True Cost Breakdown: Where the Real Money Goes

Let’s get specific, because “COBRA is expensive” doesn’t mean much without numbers. Here’s a realistic side-by-side for a 35-year-old single professional in a major US metro, with a pre-layoff employer plan that cost $900/month total.

| Cost Item | COBRA | ACA Silver Plan |

|---|---|---|

| Monthly premium | $900–$918 | $80–$250 (after subsidy) |

| Annual deductible | Carries over from employer plan | Resets — typically $1,500–$3,500 |

| Employer subsidy | None | Premium Tax Credit (income-based) |

| Network continuity | Same doctors | Must verify in-network |

| Typical 6-month cost | $5,400–$5,508 | $480–$1,500 |

| Potential 6-month savings by choosing ACA: $3,900–$5,000 | ||

That’s not a small number. For someone navigating a job search that stretches 3–6 months — which is entirely normal for mid-to-senior professionals — the ACA route can conserve $5,000–$10,000 that you badly need in reserve.

The deductible reset concern is real but overblown for healthy adults. If you’re not anticipating significant medical spending, a new plan’s deductible is largely theoretical. You’re paying for peace of mind against catastrophic events — which even Bronze plans cover at 100% above your out-of-pocket maximum.

Real Scenarios: Which Plan Wins in Your Situation?

Situation: A 38-year-old software engineer in Austin loses her job in February. She’s been seeing a rheumatologist monthly for a chronic autoimmune condition and has already spent $2,200 toward her $3,500 deductible.

The decision: COBRA. Switching plans mid-treatment risks her rheumatologist being out-of-network and resets her deductible — meaning she’d have to re-spend thousands before coverage kicks in. The COBRA premium ($880/month) is painful, but the continuity is clinically necessary.

The smart add: She simultaneously checks ACA plan networks to see if her doctor is listed. If she finds a Silver plan with the same rheumatologist in-network, she might switch at the start of the next plan year — January 1 — after the deductible year resets anyway.

Situation: A 31-year-old marketing manager in Chicago is laid off in April. He’s healthy, hasn’t used his insurance much all year, and expects his job search to take 2–4 months. His projected income for the year, including severance, is around $52,000.

The decision: ACA Marketplace. His projected income makes him eligible for meaningful Premium Tax Credits. He enrolls in a Silver plan for $140/month. His COBRA alternative would’ve been $940/month. Over a 3-month job search, that’s $2,400 saved — money that stays in his emergency fund.

Situation: A senior product manager in Seattle is laid off but has two final-round interviews already in progress. She realistically expects to start a new role within 6–8 weeks.

The smart move: Don’t elect COBRA yet. Don’t enroll in ACA yet. Let the 60-day clock run. If she lands the job before the window closes, she never needed either. If a medical issue arises in the gap, she can activate COBRA retroactively — paying only for the months she actually needs. This strategy costs nothing unless something happens.

Smart Strategy: The Hybrid Play Most People Miss

Here’s what most COBRA vs ACA articles won’t tell you, because it requires understanding a slightly obscure federal rule.

When you receive your COBRA election notice, you don’t have to decide on day one. You have up to 60 days to elect COBRA — and if you do elect it, coverage is retroactive to the date it would have started. That creates a window of strategic flexibility most people never use.

Step 1: Receive your COBRA notice. Do nothing for now.

Step 2: Simultaneously compare ACA plans on healthcare.gov using your projected annual income.

Step 3: If ACA is significantly cheaper and you’re healthy, enroll in ACA within your 60-day SEP window.

Step 4: If a medical issue arises before you decide, elect COBRA retroactively — you’ll pay back-premiums for the gap period, but you’ll have coverage from day one.

Result: You pay nothing for insurance during the decision window unless you actually need it. Maximum flexibility, minimum financial exposure.

This approach requires a bit of financial discipline — you need to be prepared to pay retroactive premiums if you activate COBRA late. But for someone in good health with 60 days of runway, it’s the financially optimal play.

One important caveat: once you’ve enrolled in ACA and your coverage starts, you generally can’t activate COBRA retroactively for that same period. The strategies are sequential, not parallel. Plan accordingly.

Common Mistakes That Cost Laid-Off Workers Thousands

I’ve watched smart people make all of these. Don’t be one of them.

Mistake 1: Automatically electing COBRA without comparing costs

The COBRA packet arrives in the mail looking official and urgent. People sign and return it without ever logging into healthcare.gov. For a family of three, that reflex decision can cost $12,000–$18,000 extra over a 6-month job search. Take two hours to compare. It’s worth it.

Mistake 2: Assuming you earn too much for ACA subsidies

Your pre-layoff salary is irrelevant. What matters is your projected income for the rest of the calendar year. A $150,000/year earner who loses their job in July and receives modest severance might project only $85,000–$95,000 for the year — which, depending on family size, could put them squarely in subsidy territory. Run the numbers at healthcare.gov before assuming you don’t qualify.

Mistake 3: Missing the 60-day enrollment window

Both COBRA and ACA Special Enrollment have firm 60-day deadlines. Miss COBRA’s window and you can’t enroll. Miss ACA’s SEP and you’re uninsured until open enrollment in November (for January coverage). Set a calendar reminder the day your coverage ends. Do not let this deadline sneak up on you.

Mistake 4: Not verifying provider networks before enrolling in ACA

ACA plan networks vary dramatically — even within the same insurer. A Blue Cross Gold plan in one metro might include your hospital; a Blue Cross Silver plan might not. Always use the plan’s provider lookup tool before enrolling. Confirm your primary care doctor, any specialists you see, and your pharmacy. Skipping this step is how people end up with surprise out-of-network bills.

Mistake 5: Ignoring how severance affects ACA subsidy calculations

Lump-sum severance counts as ordinary income in the year you receive it. A generous severance package could push your annual MAGI high enough to reduce or eliminate your Premium Tax Credits — and if you underestimate your income at enrollment and receive excess subsidies, you’ll repay the difference at tax time. If your severance is substantial, consider speaking with a tax advisor before choosing your ACA plan tier.

Final Decision Framework

Here’s the honest summary. Most people agonize over this decision, but the right answer usually becomes clear once you map your situation against two variables: your health status and your income drop.

Choose COBRA If…

- You’re mid-treatment with a specialist

- You’ve hit a significant portion of your deductible

- You’re late in the plan year (Oct–Dec)

- Your ACA network doesn’t include your doctors

- You expect to return to work within 30 days

Choose ACA Marketplace If…

- You’re generally healthy with no active treatment

- Your income dropped significantly after layoff

- You expect a job search of 2+ months

- Cost savings are a priority right now

- You’re early in the deductible year (Jan–Apr)

The honest truth: in roughly 75–80% of layoff situations I’ve seen, ACA Marketplace is the financially superior choice. The exceptions — ongoing treatment, near-deductible, very short job searches — are real, but they’re exceptions. Start with ACA as your default and work backward from there.

What to Do in the First 30 Days After a Layoff — Your Complete Financial Checklist

Frequently Asked Questions

Is COBRA always more expensive than ACA Marketplace?

In the vast majority of cases, yes. COBRA requires you to pay both your share and your former employer’s share of the premium — often $800–$1,400/month for a single person. ACA plans, with income-based subsidies triggered by a layoff, can drop that figure to $50–$300/month depending on your projected annual income. The gap narrows if your ACA subsidy eligibility is limited by severance income.

Can I switch from COBRA to ACA Marketplace after I enroll?

Yes — but timing matters. Losing COBRA coverage (not just electing it) counts as a qualifying life event that opens a 60-day Special Enrollment Period on the ACA Marketplace. So if you enrolled in COBRA and later want to switch, you’ll generally need to wait until you actually lose COBRA eligibility or until open enrollment in November (for January 1 coverage).

How long do I have to enroll in COBRA after losing my job?

You have 60 days from either the date of the qualifying event (job loss) or the date your employer sends the COBRA election notice — whichever is later. Miss that window and you lose the option entirely. ACA Special Enrollment is also 60 days from the date you lose job-based coverage. Both clocks often run concurrently, but confirm your coverage end date with your HR department.

What if I get a new job within 30 days — should I still enroll in COBRA?

Probably not. If your new employer offers coverage with little or no waiting period, enrolling in COBRA adds a premium bill you won’t need. The smarter play: confirm your new plan’s start date, leave the 60-day COBRA window open as a safety net, and activate retroactively only if a health event occurs in the gap before new coverage kicks in.

Does severance pay count as income for ACA subsidies?

Yes. Severance is counted as ordinary income and affects your Modified Adjusted Gross Income (MAGI), which determines subsidy eligibility. A large lump-sum severance could push you above the threshold for meaningful Premium Tax Credits for the year. Always calculate your projected annual income carefully — and if your severance is substantial, consider a quick consultation with a tax advisor before enrolling.

Can I cancel COBRA at any time?

Yes. You can stop paying COBRA premiums at any time, which effectively cancels coverage. However, once cancelled, you generally can’t re-enroll. That said, losing COBRA voluntarily before the 18-month period ends does open a Special Enrollment Period on the ACA Marketplace — so you can transition without a coverage gap if you time it correctly.

Is there any scenario where COBRA is the financially smarter choice?

Yes — when you’ve already met a large portion of your annual deductible. If it’s October and you’ve hit $4,000 of a $5,000 deductible, switching to ACA resets that clock. Staying on COBRA through year-end, then switching January 1, protects the deductible credit you’ve already earned. That math alone can make COBRA worth the premium for 1–3 months, especially if you anticipate additional medical costs before December 31.

The Bottom Line

The COBRA vs ACA Marketplace decision comes down to one core question: are you optimizing for continuity or for cost? COBRA gives you the comfort of keeping everything the same — same doctors, same deductible progress, zero administrative hassle. That comfort has real value in specific medical situations. But for the majority of laid-off professionals who are reasonably healthy and facing an uncertain income period, it’s an expensive habit dressed up as security.

The ACA Marketplace, especially in 2026 with enhanced subsidies still available, offers a genuinely competitive alternative that most people underestimate because they’ve never actually logged in and run the numbers. Do that before you decide anything. Healthcare.gov’s plan comparison tool takes 20 minutes and could save you $5,000–$10,000 over a typical job search.

And if you’re genuinely unsure? Use the 60-day COBRA election window as breathing room. You don’t have to decide on day one. Compare your options, project your income realistically, verify your provider networks, and then choose deliberately — not out of panic.

That’s the kind of clear-eyed COBRA vs ACA Marketplace decision that protects both your health and your finances during one of the most stressful transitions of your career.

Michael Reeves | Former Senior Counsel, Littler Mendelson | Severance & Restructuring Specialist | 18+ Years in Employment Law

Author bio: Michael Reeves spent nearly two decades as Senior Counsel at Littler Mendelson — one of the world’s largest employment law firms — advising on mass layoffs, corporate restructurings, and severance negotiations for Fortune 500 companies across the US and Europe. He has worked both sides of the table: structuring cost-efficient separation packages for employers and, more recently, helping employees understand exactly where their leverage lies. Based between Chicago and London, Michael writes for HRGet.com to demystify the legal and financial dimensions of layoffs — so employees stop leaving money on the table.