If you’re self-employed, health insurance for the self-employed isn’t just another line item — it’s one of the most consequential financial decisions you’ll make every single year. Get it wrong and you’re either haemorrhaging money on premiums you didn’t need to pay, or you’re one emergency room visit away from a $40,000 bill that wipes out six months of client work.

I’ve spent years advising independent contractors, consultants, and small business owners on benefits strategy. And the same pattern repeats constantly: people either leave thousands of dollars in subsidies on the table, or they buy an expensive private plan because it “felt more professional.” Both are mistakes that compound over time.

This guide gives you a clear, income-based framework for choosing between Marketplace (ACA) plans and private insurance in 2026 — with actual numbers, real scenarios, and the hidden cost traps most comparison articles skip entirely.

What Self-Employed Health Insurance Actually Means

When you leave a traditional job — whether voluntarily or through a layoff — you lose three things that most people underestimate: employer-sponsored coverage, subsidized premiums, and the HR team that handled all the paperwork without you having to think about it. Now it’s all on you.

Here’s the structural reality: as a self-employed individual, you pay 100% of your monthly premium upfront. There’s no employer splitting it 70/30. A plan that might have cost you $180/month as an employee can suddenly cost $520/month as a freelancer for the exact same coverage level.

But — and this is crucial — self-employed people have access to two cost offsets that salaried employees don’t:

- Premium Tax Credits (ACA subsidies) — income-based discounts applied to Marketplace plans that can reduce your monthly cost to near-zero in some cases

- Self-employed health insurance deduction — you can deduct 100% of your premium from your taxable income, reducing your effective cost materially

Most self-employed people know about one of these. Very few optimise for both simultaneously. That’s where the real savings live — and we’ll get into the math shortly.

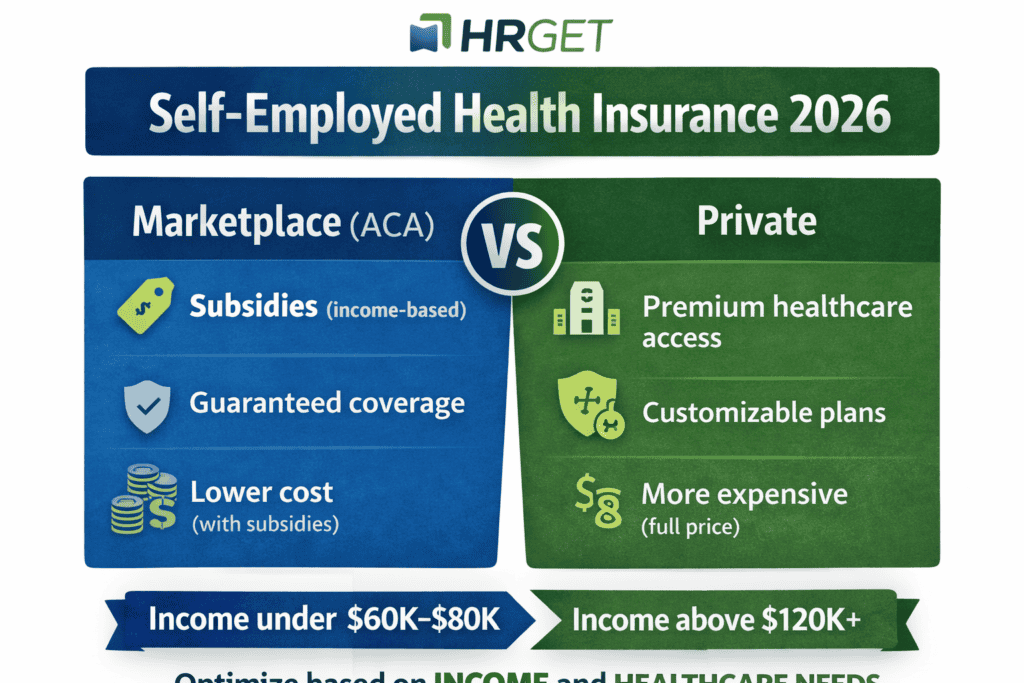

Marketplace vs Private: Side-by-Side Comparison

| Feature | Marketplace (ACA) | Private Insurance |

|---|---|---|

| Subsidies available | Yes — income-based premium tax credits | No |

| Coverage standards | Regulated — 10 essential health benefits required | Flexible — varies by insurer |

| Pre-existing conditions | Always covered, no exceptions | Improved post-ACA, but verify plan terms |

| Monthly premium (individual, no subsidy) | $350–$650 depending on plan tier and state | $400–$900+ depending on coverage level |

| Monthly premium (with subsidy) | $0–$250 for many income brackets | N/A |

| Provider network | Narrower — state-specific HMO/PPO networks | Often broader, including out-of-state specialists |

| Enrollment window | Open enrollment (Nov–Jan) or qualifying life event | Year-round |

| Customisability | Low — tiered plans (Bronze/Silver/Gold/Platinum) | High — deductible, add-on, network options |

| Tax deductibility | Yes (self-employed deduction applies) | Yes (same deduction applies) |

The “private is better quality” assumption is the most expensive myth in self-employed benefits. Many Marketplace Silver plans use the same hospital networks as comparable private plans in major metro areas — but cost $2,000–$4,000 less annually because of subsidy eligibility. Always run the subsidy calculation first before you even look at private quotes.

Marketplace (ACA) Plans: Pros, Cons, and Who Should Choose

Marketplace plans — offered through Healthcare.gov or your state’s exchange — operate under the Affordable Care Act. The architecture is straightforward: Bronze plans have lower premiums and higher deductibles; Platinum plans flip that. Most self-employed individuals land in Silver territory, and for good reason — Silver plans unlock additional cost-sharing reductions if your income is below 250% of the federal poverty level.

Where ACA Plans Win

Subsidies are genuinely transformative. A freelance designer earning $52,000/year in 2026 would pay roughly $180–$280/month for a solid Silver plan after premium tax credits — compared to $500+ for a comparable private plan. That’s $2,500–$4,000 in annual savings that’s effectively invisible if you never check your subsidy eligibility.

Guaranteed coverage regardless of health history. ACA plans can’t deny you, charge you more, or exclude a condition because of your medical background. For anyone managing a chronic condition — Type 2 diabetes, hypertension, autoimmune issues — this isn’t a minor benefit, it’s the whole ballgame.

Standardised minimum benefits. Every ACA plan covers preventive care (annual physicals, screenings, vaccinations) at $0 cost sharing. Mental health services, substance use treatment, emergency care, and prescription drugs are mandatory inclusions. You won’t get a plan that technically covers hospitalisation but quietly excludes medications.

Where ACA Plans Fall Short

Network restrictions are real. Many Marketplace HMO plans require referrals for specialist visits and won’t cover out-of-network care except in emergencies. If you travel frequently for work or want to see a specialist at a top academic medical centre without jumping through hoops, this matters.

Income estimation is a genuine risk. Your subsidy is calculated based on your projected annual income. Self-employment income fluctuates — and if you earn significantly more than estimated, you’ll repay part of your subsidy at tax time. I’ve seen freelancers get surprised by $1,800–$3,000 repayment bills in April. The fix is conservative income estimates and mid-year adjustments through your exchange account.

Who should choose Marketplace plans: Anyone with income below roughly $58,000 (single) or $78,000 (couple) in 2026, those with pre-existing conditions, and anyone who values predictable costs over network breadth.

Private Health Insurance: Pros, Cons, and Who Should Choose

Private plans — purchased directly from insurers like Cigna, Aetna, UnitedHealthcare, or regional providers — sit outside the exchange. You’re buying off-market, which means no subsidies, but also fewer constraints on plan design.

Where Private Plans Win

Network breadth is the headline advantage. Private PPO plans, particularly at mid-to-premium tiers, give you direct access to specialists at major medical centres — Mayo Clinic, Cleveland Clinic, MD Anderson — without referrals and often without prior authorisation requirements. For a business owner or consultant who travels across state lines, this matters more than the premium difference.

Plan customisation. Private insurers let you design coverage around your actual life: higher premium / lower deductible if you use healthcare frequently; a leaner plan with a Health Savings Account (HSA) if you’re generally healthy and want to build a tax-advantaged medical fund. The tiered, one-size-mostly-fits-all structure of ACA plans doesn’t offer this flexibility.

Year-round enrollment. No waiting for open enrollment or a qualifying life event. If you launched your business in March or went full-time freelance in August, you can get coverage within days — not months.

Where Private Plans Fall Short

Full-price premiums are brutal without subsidies. A 38-year-old in Chicago looking at a solid private PPO plan with a $3,000 individual deductible will typically pay $520–$750/month in 2026. That’s $6,200–$9,000/year before you’ve paid a single co-pay or filled a prescription. The math rarely works unless you genuinely can’t get subsidies.

Plan quality varies dramatically. Unlike ACA plans, private insurers aren’t required to cover all 10 essential health benefits. Some short-term or limited-benefit plans — which technically count as “private” — exclude maternity care, mental health, and prescription coverage. Always read the Summary of Benefits and Coverage document, not just the marketing sheet.

Who should choose private plans: Self-employed individuals earning above ~$80,000 (single) where subsidies phase out, those who need broad specialist access without referral requirements, and business owners who want an HSA-eligible high-deductible plan paired with aggressive savings contributions.

If you’re considering a private high-deductible health plan (HDHP), pair it with a Health Savings Account (HSA). In 2026, you can contribute up to $4,300 (individual) or $8,550 (family) pre-tax. That money rolls over indefinitely, grows tax-free, and covers qualified medical expenses — essentially a second retirement account that also handles healthcare costs.

Real Scenario: Income-Based Decision Breakdown

Scenario A — Freelance UX designer, $44,000/year, Chicago, age 34, no dependents

Subsidy eligibility: Strong. Premium tax credit brings a Silver plan down to roughly $95–$160/month. Full-price equivalent: ~$490/month. The annual gap is nearly $4,000. Marketplace is the obvious call — private insurance here is a $4,000 mistake.

Scenario B — Independent strategy consultant, $115,000/year, New York, age 41, spouse + one child

Subsidy phases out almost entirely at this income level. A Marketplace family Silver plan runs $1,100–$1,400/month at full price. A private PPO family plan: $1,050–$1,350/month with better network access. Now it’s genuinely a comparison decision — and the private plan’s network breadth may tip the scales, especially with a child who needs specialist access.

Scenario C — Founder/owner, $280,000/year, Dallas, age 45, family of four

No subsidy eligibility. At this income level, private plans with executive-tier coverage — $1,400–$2,000/month — are the category that fits. The self-employed health insurance deduction softens the blow: at a 35% effective tax rate, a $2,000/month premium costs $1,300 in after-tax dollars. Still expensive, but not as brutal as the sticker price suggests.

Hidden Costs Most People Ignore

Monthly premium is the number people focus on. It’s also the number that leads to the worst purchasing decisions. Here’s what actually determines your total annual cost:

Deductible: The Real Starting Point

A “cheap” Bronze plan at $180/month often carries a $7,000–$9,000 individual deductible. If you have any meaningful health event — a surgery, an ER visit, even a series of specialist appointments — you’ll pay every dollar of that deductible before insurance covers anything. A Silver plan at $320/month with a $2,500 deductible may cost less over the full year if you use healthcare regularly.

Out-of-Pocket Maximum

This is your worst-case scenario. In 2026, ACA plans cap individual out-of-pocket costs at $9,450. Some private plans have no cap — or a much higher one. Always compare out-of-pocket maximums alongside monthly premiums. For someone with a serious health event, the difference between a $9,450 cap and an uncapped plan can be financially catastrophic.

Network Costs: The Sneaky One

Out-of-network emergency care is one of the most common financial shocks I see self-employed professionals experience. You’re admitted to a hospital through the ER, the facility is in-network, but the attending physician is not — and you’re billed at out-of-network rates. The No Surprises Act (2022) provides some protection here, but it doesn’t eliminate all balance billing scenarios. Check whether your plan uses surprise billing protections and read the out-of-network cost-sharing terms carefully.

Prescription Drug Costs

Drug formularies — the list of medications your plan covers and at what cost — vary wildly. If you take a brand-name medication regularly, check the formulary before you buy. I’ve seen people save $800/year simply by choosing the plan that placed their specific medication in Tier 2 rather than Tier 3.

Don’t buy a short-term health plan as a primary coverage solution. These plans are technically “private insurance” but they’re not ACA-compliant — they can exclude pre-existing conditions, cap annual benefits, and leave you exposed to significant out-of-pocket costs. They work as a bridge during a coverage gap (30–90 days), not as a full-year strategy.

Smart Strategy: How to Choose in 2026

Here’s the decision framework I walk self-employed clients through. It’s not complicated — but most people skip step one entirely, which makes everything else wrong.

Step 1: Calculate your subsidy eligibility first. Go to Healthcare.gov or your state’s exchange and use the subsidy estimator. Enter your projected net self-employment income (after business deductions). This single number determines whether Marketplace is a slam dunk or a fair fight with private plans.

Step 2: Estimate your total annual healthcare cost — not just the premium. Add your annual premium to your expected out-of-pocket spending (based on your typical utilisation — doctor visits, prescriptions, any planned procedures). Compare this number across plans, not just the monthly premium.

Step 3: Verify your providers are in-network. Before you commit, check that your primary care physician and any specialists you see regularly are in-network for the plan you’re considering. This step takes 10 minutes and prevents the single most common source of unexpected medical bills.

Step 4: Apply the self-employed health insurance deduction. Calculate your effective post-deduction cost. If you’re in the 24% federal tax bracket, every $100 of premium costs you $76 in real money. This often closes the perceived gap between Marketplace and private plans at the higher end of the income spectrum.

Step 5: Decide on HSA compatibility. If you’re going with a high-deductible plan — either ACA or private — confirm it’s HSA-eligible and open an account immediately. Max your contribution every year. It’s one of the most tax-efficient financial moves available to self-employed individuals in 2026.

Common Mistakes to Avoid

I’ll be blunt — these are the errors I see repeatedly, and they cost people real money:

- Choosing by premium alone. A $180/month plan with a $9,000 deductible is not a cheap plan. It’s a plan that bills you later instead of now. Always compare total annual exposure.

- Ignoring subsidy eligibility because you “make good money.” The enhanced subsidies introduced through the Inflation Reduction Act (still applicable in 2026) extend eligibility further up the income scale than most people realise. Run the calculator regardless of what you think you earn.

- Underestimating income and triggering repayment. If you’re a growing freelancer and your income comes in 30% higher than projected, you’ll repay a portion of your subsidy at tax time. Build a buffer — estimate conservatively but revisit mid-year.

- Not verifying your doctors are in-network. Network adequacy is real. Before open enrollment ends, spend 10 minutes confirming your preferred providers accept the plan. Switching doctors because of an insurance choice is entirely avoidable.

- Skipping the HSA opportunity. Even if you’re healthy and rarely use healthcare, an HSA-eligible HDHP lets you build a substantial tax-advantaged reserve. Over 10 years, maxing HSA contributions creates a six-figure medical fund — and if you stay healthy, you can use it for retirement healthcare costs tax-free.

Final Verdict: Marketplace vs Private for the Self-Employed

Marketplace wins for roughly 70–75% of self-employed individuals — specifically everyone earning below ~$75,000 (single) or ~$100,000 (family) where subsidies make the math decisively favourable.

Private insurance makes sense for high-income earners above the subsidy threshold who need broad specialist access, year-round enrollment flexibility, or custom plan design that ACA tiers don’t offer.

The real insight: this is an income optimisation decision, not a quality-of-care decision. The right plan is the one that minimises your total annual healthcare cost after subsidies, deductions, and realistic utilisation — not the one with the best brand recognition or the lowest sticker-price premium.

For most freelancers and independent contractors starting out, the move is simple: check your subsidy eligibility on Healthcare.gov, pick a Silver plan that includes your providers, and pair it with an HSA if you go high-deductible. As your income grows toward and past the subsidy cliff, revisit the private market with fresh eyes and the deduction math in hand.

The best health insurance for self-employed professionals in 2026 isn’t a specific plan or insurer — it’s the one you chose after running the actual numbers, not the one a broker pushed because it pays higher commission.

Related reading on HRGet.com

How to Calculate Self-Employment Taxes in 2026 (With Deduction Strategies) — understanding your net income is the first step to getting your health insurance math right.

Frequently Asked Questions

By Emily Carter | Updated April 2026 | 11 min read

Emily Carter is a career coach and former McKinsey talent advisor with 15+ years of experience helping professionals navigate career transitions, promotions, and high-stakes job decisions. She has advised professionals across consulting, technology, finance, and corporate leadership roles on offer negotiations, career positioning, and long-term growth strategy.

Role: Career Coach & Ex-McKinsey Talent Advisor: Focuses on helping professionals make smarter career moves—switching jobs, negotiating offers, and long-term career growth. She blends structured thinking with real-world coaching insights.